Barbell Investing Strategy – How to Use A Barbell Portfolio Strategy

What is a barbell investing strategy? In this article, we look at some related posts and explain asset allocation when using a barbell strategy (as coined by Nassim Taleb in the book Antifragile).

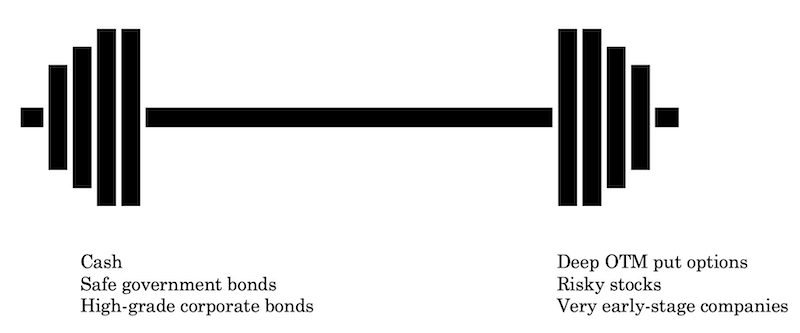

A barbell investment strategy aims to minimise risk with the largest part of the portfolio, but embrace exposure to black swan events with small, low-cost but high risk positions in the remainder.

Top Brokers For Barbell Portfolio Strategies

-

1

Interactive Brokers

Interactive Brokers -

2

NinjaTrader

NinjaTrader -

3

eToro USAeToro USA LLC and eToro USA Securities Inc.; Investing involves risk, including loss of principal; Not a recommendation

eToro USAeToro USA LLC and eToro USA Securities Inc.; Investing involves risk, including loss of principal; Not a recommendation -

4

Plus500USTrading in futures and options involves the risk of loss and is not suitable for everyone.

Plus500USTrading in futures and options involves the risk of loss and is not suitable for everyone.

Key Takeaways – Barbell Investing Strategy

- Diversification and Balance

- Barbell investing strategy emphasizes balancing the portfolio between high-risk and low-risk assets.

- Instead of trying to predict market directions or bothering with medium-risk assets that have only moderate returns with risks that are difficult to estimate.

- Risk Management

- By combining assets with contrasting risk profiles, such as high-risk equities and low-risk bonds, the strategy manages overall portfolio risk.

- This configuration allows for capital appreciation during market upswings and risk mitigation during downturns, to help with the risk-return trade-off.

- Adaptability and Long-Term Focus

- This approach tries to protect against market volatility and economic fluctuations, with the safe part of the portfolio staying stable and the risky part may or may not paying off (e.g., deep OTM put options vs. high-risk startups).

- Backtesting the Barbell Approach

- We backtest the barbell and compare it to the S&P 500 and a traditional balanced portfolio.

Real-World Barbell Strategy

In a previous article, we covered Universa Investment’s performance through its tail risk hedging strategy. It pursues what’s commonly known as a barbell portfolio.

Universa’s capital risk in the “high risk” part of its portfolio is only 2 to 3 percent of its overall capital – i.e., the part it dedicates to put options to benefit off the occasional market routs.

It earned at least $3 billion from the market decline with about only $100 million in total derivatives exposure.

The other part of its portfolio is in a mix of safe assets like cash, government bonds, and high-grade corporate bonds that pay out safely.

The payoff from the safe assets essentially fund the derivatives exposure.

Universa makes it straightforward to its clients that it doesn’t expect to generate anything in sub-average to great market environments for equities. But it expects to make a lot when the market crashes because of its highly convex exposure to big market drops.

Given most investment funds have equity beta (i.e., are long a lot of equities) and have other types of equity risk in addition (e.g., real estate, private equity, early-stage companies), adding a portion of their portfolio to a tail-risk hedging strategy could be a judicious use of capital.

It’s something unique and can provide an offset when the bulk of its portfolio doesn’t do well.

Barbell Portfolios

Barbell portfolios – and portfolios that use barbell strategy concepts – are out there in one form or another.

But they’re not popular because their risk allocation is so low.

For institutional funds in particular, without a consistent low-double digit percentage return each year – or at least something that beats passive index tracking within acceptable risk parameters – it’s hard for them to scale.

Structure Of A Barbell Portfolio

Traders who take the barbell portfolio approach structure the portfolio in a way where there’s a dichotomy between “high risk” and “low risk” and little, if anything, in between:

You see some combination of:

- i) a small allocation toward nonlinear, high convexity bets on one end that don’t lose much if they don’t pan out but can make a lot if they do, and

- ii) a larger allocation toward assets that have less volatility and lower yields that provide low, stable returns

Safe Barbell Assets

- Treasury bills

- Government bonds

- Cash or cash equivalents

- High-grade corporate bonds

- Fixed deposits

Risky, Convex Barbell Assets

- Out-of-the-money (OTM) put options

- Venture capital investments

- High-risk personal projects (starting a new business with no previous experience)

- High-risk stocks

- Tactical day trading

- Commodities with speculative potential

- Cryptocurrencies

Because the types of bets are so different from each other from a risk and potential return perspective – virtually on opposite ends of a spectrum – this gives rise to the name barbell portfolio.

You have allocations on each side of the risk/return spectrum, giving it a dichotomous weighting.

As an example of what could be considered on each end of the barbell:

While Universa uses put options as part of its “high risk” basket, it doesn’t have to be puts.

It can be virtually anything that gives high return potential but a high likelihood of either not panning out or simply having a lot of risk or price volatility.

This can mean things like:

- Highly speculative stocks, businesses, and commercial projects

- Very early-stage ventures, perhaps even pre-revenue companies

- Cryptocurrencies

- Any type of derivative structure with a low likelihood of winning

If traders risk a few percent of their portfolios per year on the highly convex, asymmetric payout bets and return that 2 to 4 percent on the “safe bets” then in an otherwise normal year the portfolio will remain steady.

The returns on the safe bets effectively pay for the losses on the long-shot bets.

It’s not going to be the most exciting portfolio most of the time and you won’t see much growth.

But every now and then, maybe every 10 years, this type of portfolio can see great returns of three-digit or even four-digit percentage gains in one year – if put into highly convex, speculative investments.

Many institutional investors that look for something different from what they have can benefit if they deem that it helps them manage risk or enhance returns more effectively.

Nassim Taleb’s Barbell Philosophy

Nassim Taleb’s advocacy for the barbell approach to risk management is a reflection of his broader philosophy on uncertainty, risk, and decision-making under conditions of opacity.

Here are the key elements of this approach:

Concept of the Barbell Strategy

- Avoiding the Middle – Taleb’s barbell strategy advocates for avoiding medium-risk investments. He posits that risk is inherently difficult to calculate accurately. Instead, it promotes a binary investment strategy.

- Combination of Extremes – The strategy involves a linear combination of extremes – being hyper-conservative on one end and hyper-aggressive on the other.

- Robustness to Estimation Errors – By focusing on the extremes and avoiding the middle, the barbell strategy is seen as more robust to errors in risk estimation.

Application in Investment

- Asset Allocation – Typically, a large portion of the portfolio (80-90%) is allocated to extremely safe investments, such as treasury bills, to preserve capital.

- Speculative Component – The remaining portion is invested in high-risk, diversified speculative bets aiming for high returns.

- Limited Downside Speculation – An alternative form of the barbell strategy involves engaging in speculative investments where the potential downside is limited, allowing for aggressive risk-taking with controlled loss potential.

Philosophical Underpinnings

- Skepticism of Risk Measurement – Taleb’s approach stems from a skepticism towards the accuracy and reliability of risk measurement tools and models. He emphasizes the unpredictable nature of the real world.

- Preference for Extremes – His endorsement of the barbell strategy reflects a belief that in environments of uncertainty. He argues that concentrating investments in the extremes can lead to a more predictable and controlled range of outcomes.

Impact on Decision-Making

- Influences on Financial and Personal Decisions – The barbell strategy is not only a financial investment approach but also a life philosophy. Taleb suggests applying this principle across various domains, including politics, economics, and personal life choices like exercising (e.g., resting/walking moderating vs. short bursts of intense exercise).

Overall

Nassim Taleb’s barbell strategy is a manifestation of his broader philosophical stance on uncertainty.

He advocates for a risk management approach that eschews moderate risks in favor of a mix of extreme conservatism and aggressive speculation.

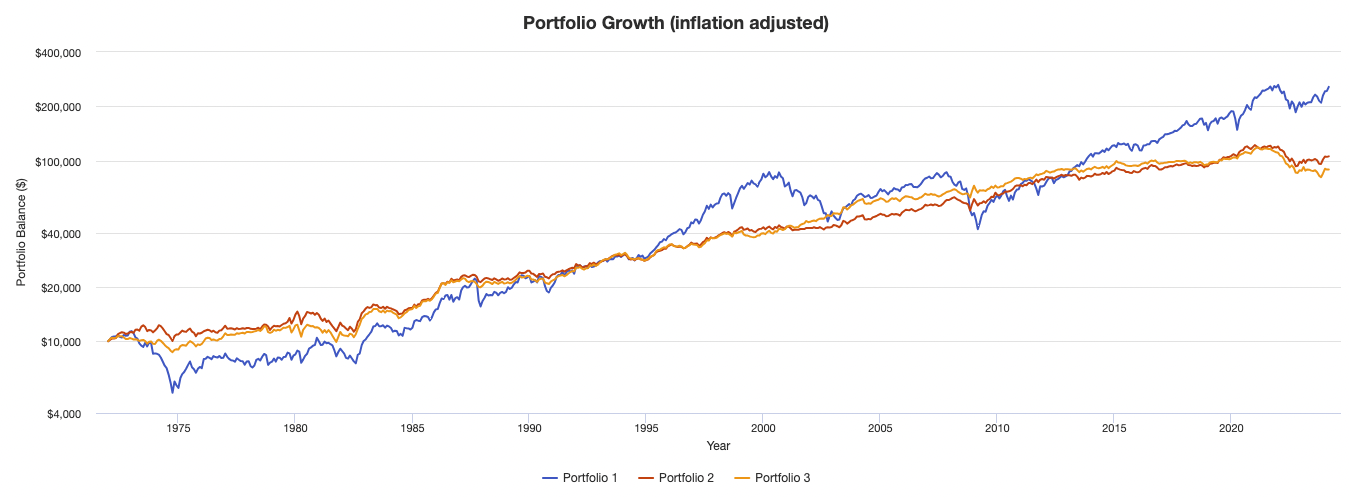

Barbell Backtesting

How does the barbell perform in a backtest?

We tested the following portfolios:

Portfolio 1 – All Stocks

| Asset Class | Allocation |

|---|---|

| US Stock Market | 100.00% |

Portfolio 2 – More Traditional Balanced Portfolio

| Asset Class | Allocation |

|---|---|

| US Stock Market | 30.00% |

| 10-year Treasury | 50.00% |

| Gold | 20.00% |

Portfolio 3 – Barbell

| Asset Class | Allocation |

|---|---|

| 10-year Treasury | 70.00% |

| Gold | 10.00% |

| US Micro Cap | 20.00% |

Here, we follow the traditional barbell approach, with 80% in safer assets (70% US Treasuries and 10% in gold), and the other 20% of the portfolio going into higher-risk micro caps.

Results

| Portfolio | Initial Balance | Final Balance | CAGR | Stdev | Best Year | Worst Year | Max. Drawdown | Sharpe Ratio | Sortino Ratio | Market Correlation |

|---|---|---|---|---|---|---|---|---|---|---|

| Stocks | $10,000 | $1,925,614 | 10.61% | 15.75% | 37.82% | -37.04% | -50.89% | 0.44 | 0.64 | 1.00 |

| Balanced | $10,000 | $793,062 | 8.74% | 7.91% | 33.50% | -13.63% | -17.23% | 0.54 | 0.85 | 0.64 |

| Barbell | $10,000 | $670,207 | 8.39% | 7.33% | 34.78% | -15.39% | -21.61% | 0.53 | 0.84 | 0.53 |

The barbell approach, overall, did quite well on a risk-adjusted basis.

Its Sharpe and Sortino ratios were on par with the more traditionally balanced portfolio (S&P 500 or equivalent, moderate bonds, moderate gold).

It had a little bit of a higher drawdown.

The approach (barbell) may also not work as well when real interest rates are negative due to the heavy safe-asset exposure.

While the 100% stocks approach “wins” at face value, it’s important to realize that the balanced and barbell approaches are getting these types of returns with half the volatility or less as the all-stocks approach.

A good financial engineer could run this portfolio at the same volatility as the S&P 500 and get returns that are roughly 7% better per year.

The barbell has a lower correlation to the broader stock market than the more traditional balanced portfolio and has a slightly better skew (though higher kurtosis, which is displayed in its higher maximum drawdown).

We have some more advanced metrics describing these portfolios in the Appendix at the end of this article.

Barbell Concepts For Non-Barbell Traders

Hedging tail risk prudently is important for every trader.

Ideally hedging should be done in a way where the benefits outweigh the costs.

Because of the volatility risk premium where options are structurally expensive (similar to standard insurance policies issued by private insurance businesses so they have a profit and a sustainable business), perpetual hedging is a long-run drag on performance.

When hedging tail risk with a focus on value, preparing for an economic and market bruising makes sense when justified. Namely, when volatility is cheap such that it makes sense when making the bet.

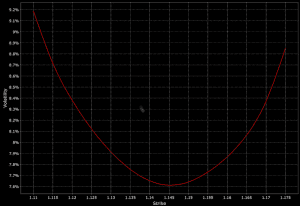

How do we know when volatility is cheap?

An easy way is to look at the historic realized volatility of whatever you’re trading and compare that to the implied volatility going forward.

Almost all brokers have an implied volatility calculator within an options chain, often shown as ‘IV’ followed by an annual percentage.

For example, the historical volatility of the S&P 500 is about 15 to 16 percent annualized. In the example below, implied volatility is about 22 percent, making it more expensive than normal.

(Source: Interactive Brokers)

Some top trading brokers even show implied volatility across all strike prices of a certain maturity.

Implied volatility is not static across all strikes.

With respect to stocks, traders have more demand for downside protection to protect against losses, making puts generally more expensive than calls. This reflects in a volatility skew, where put option IVs tend to be higher than call option IVs.

(Source: Interactive Brokers ‘Implied Volatility Viewer’)

At the same time, while historic volatility can be a good guide of how an asset is likely to act, the future is not always like the past.

For example, government bond volatility is lower than in past history given central banks anchor them down at zero to keep today’s highly indebted economies going.

Because of this lower volatility in interest rates of both the short- and long-term variety, this also cuts down on currency volatility as well.

Price Dynamics For Barbell Investing

Barbell portfolios are designed to help get ahead during downturns and mostly tread water during good periods.

Many traders and institutions believe that a portfolio should be fully invested all the time. Universa’s approach is that only a slight part of the portfolio is invested in the convex bets with the remainder in the safer lower-yield assets.

For most investors that type of approach doesn’t work as they’re likely to face years or a decade or more of no capital appreciation.

But barbell portfolios fulfill a niche in the market. Every investment manager looking to take on outside clients has to differentiate in some way.

Being fully invested is generally good for investment firms in order to generate fees, but it isn’t necessarily the best for clients.

With the barbell portfolio, the main consideration isn’t necessarily between earning very little to nothing in cash or cash-like securities and earning something a bit better in standard bond and stock investments.

This is the standard trade-off made in conventional portfolios.

Instead of “opposing extremes” asset allocation is viewed on a continuum in terms of how much to allocate to cash, bonds, and stocks, examining the reward and risk of each in both absolute terms and relative to each other.

Instead, for a barbell portfolio strategy, it’s about the optionality of the cash.

In other words, how much it can earn you if assets become cheap enough versus the potential cost of holding them at more expensive levels.

But having a lot of cash and cash-like assets is not popular among investment managers because it’s not good for business.

People don’t want to pay management fees just to have their cash lay around not being used.

People are naturally impatient. While most sophisticated clients – e.g., pension funds, sovereign wealth funds, endowments – have healthy expectations, they still want to see results to stay onboard.

It’s not an easy argument to make that they should sit out present gains for the prospect of future gains that may not transpire. It’s the standard conundrum of the value investor who prefers to mostly sit out expensive markets only to see them zoom higher most of the time.

Most investment managers can’t have a barbell portfolio strategy – in the sense of a heavy concentration in very safe assets – and expect their business to thrive.

Universa is unique, but it also doesn’t have a lot of money allocated to it – at least pre-2020 – for a reason. Few clients are willing to see no gains year after year.

One’s fiduciary duty is to nonetheless do what’s best for clients, even if that does lead to a smaller client base.

Those that are willing to allocate to a tail risk hedging fund will likely only do so in a small quantity to help balance out their equity risk.

Other Types Of Barbell Strategy

Barbell strategies often refer to fixed income portfolios.

Part of the portfolio might be in longer duration securities (e.g., longer than 10 years) that give higher yields while the other part might be in shorter duration securities (e.g., less than five years) that are more stable in price.

But the barbell can mean many different approaches.

It could be as basic as a stocks and bonds dichotomy, such as a 60/40 or 50/50 portfolio.

The weightings can also move around as necessary to help accomplish certain objectives.

The barbell portfolio attempts to provide diversification in such a way to get access to both safe yields and riskier assets (that can provide higher yields) at the same time.

Many portfolios do this, but don’t have a distinct dichotomy between the two.

In a fixed income context, the short-term yields can take advantage of current interest rates while also holding longer duration securities that pay higher yields.

If interest rates were to rise, the shorter duration bonds won’t have as much price risk and can be rolled into new bonds that offer the higher yields.

The barbell strategy is a more active form of trading, whether it be due to the shorter duration nature of some securities and the rolling over process, monitoring the riskier part of a portfolio, or otherwise.

As in Universa’s case, the barbell strategy enables a portfolio to earn returns safely to help effectively fund a riskier part of the portfolio.

It uses cash and bonds to fund the put option part of the portfolio. The liquidity associated with cash and bonds also provide flexibility if one wants to more actively manage a portfolio.

A barbell manager might have the goal to at least return the rate of inflation to avoid losing purchasing power over time.

To do this, the portfolio might invest in inflation-protected bonds and a mix of other securities to get to the inflation rate plus any additional return required to fund the higher risk portion of a portfolio (e.g., OTM options).

Barbell Strategies That Anyone Can Do

Many people who hear about the barbell portfolio love the idea. It’s simple – most of your capital into safe assets and the rest on riskier and/or higher convexity bets that have the potential to pay off massively if the world breaks the way you think it might. And avoid the middle, where risk is often hardest to measure and returns are modest.

But knowing the logic and implementing it are two different things.

What I want to walk through in this section are the practical mechanics.

How do you structure 80 to 90 percent of your savings on the safe end?

What do you put on the risky end?

How do you fund the risky bets from the yield on the safe side? How do you rebalance? And how does any of this change depending on what’s going on in the world?

The Core Logic

The barbell only works if you understand what it is trying to do.

It’s not trying to beat the market in normal years. It’s trying to survive normal years while being positioned to make a lot of money in the years or periods when something favors you.

In virtually all past cases, the economy-markets linkage works like this:

- credit creation drives asset prices higher…

- debt burdens build up…

- the system becomes more fragile, and…

- eventually a trigger (a central bank tightening, a geopolitical shock, a solvency problem somewhere important) causes the whole thing to wobble.

The barbell is built to be boring during the first part of that sequence and explosive during the second.

So the question is less “how do I maximize returns?” and more “how do I stay in the game through the full cycle while keeping a cheap claim on the upside?”

It changes how you build the portfolio.

Step One: Build the Safe Side First

The safe side is the foundation. You build it first, and you build it conservatively, because this is the part that has to survive everything.

For an individual with normal savings, the safe 80 to 90 percent typically looks something like this:

A large allocation to short-duration government bills or notes

These are the closest thing to cash that still pays a yield. In the US, this means Treasury bills with maturities from four weeks to two years.

They have almost no credit risk and very little price risk if held to maturity. You can buy them directly through TreasuryDirect or through any broker.

For most individuals, a ladder of T-bills rolling every few weeks or months is the simplest approach.

An allocation to longer-duration government bonds

These provide yield and, more importantly, they tend to rally when the economy weakens and the central bank cuts rates.

That is, they give you some additional convexity on the safe side of the portfolio. How much you hold depends on where real interest rates are.

When real yields are high, you want more. When real yields are negative, you want less, because you are locking in a guaranteed loss of purchasing power.

An allocation to inflation-protected bonds (TIPS in the US)

These are the inflation-indexed bond market that are somewhat underappreciated and underused relative to their potential. They pay a real yield plus whatever inflation runs at.

If you are worried about the central bank eventually printing money to deal with debt burdens, and you should be, some TIPS exposure makes sense.

At the same time, there’s a bit of an “honor system” factor to these because the government decides what the official inflation rate is and hence what they pay on the inflation part of the bond.

A small allocation to gold

5-15% of the safe side is reasonable. Gold isn’t a yielding asset, but it’s the one asset that performs when central banks are engaging in debt monetization and when confidence in fiat currency weakens.

Gold is a diversifier that tends to work when correlations between stocks and bonds break down.

High-grade corporate bonds and municipal bonds

These can also have a part, but they add credit risk for sometimes modest additional yield (depends on credit spreads). For most individuals running a barbell, you keep the safe side mostly in sovereigns and high-quality investment-grade.

That’s the skeleton. 80%+ percent of your portfolio in a mix of T-bills, Treasury notes, TIPS, and a little gold and potentially investment-grade or muni bonds. The specific weights depend on the rate environment.

Step Two: Decide What Your Convex Bet Is

The risky end is where it gets interesting, and where most people make mistakes.

The idea of the convex bet is asymmetry. You want something where you can only lose a small, known amount, and where the upside if you are right is many multiples of what you put in.

Universa Investment famously earned at least $3 billion on roughly $100 million of derivatives exposure during a major market rout. That’s a 30x return on the slice. It’s what a convex bet looks like when it works.

Here are the practical categories of convex bets available to an individual:

Deep out-of-the-money put options on broad indexes

This is the Universa approach, simplified. You buy puts on the S&P 500 (via SPY or SPX) that are twenty percent or more below the current market, with maturities anywhere from three months to two years.

Most of them expire worthless. You’re paying for insurance against a market rout.

When volatility is cheap, meaning implied volatility is low relative to historical realized volatility, these are attractive. When volatility is expensive, you wait.

Long-dated call options on assets you think could explode upward

This is the mirror image. If you think a particular asset or sector has a small probability of an enormous move higher, long-dated out-of-the-money calls give you that exposure without requiring you to put up much capital.

Venture capital, seed-stage equity, and private startup exposure

These are highly illiquid, highly risky, but also highly convex. You put in a small amount, you accept you will likely lose most or all of it, and you hope one or two bets pay off in a big way.

Sequoia Capital, one of the most well-known VCs in the world, once stated that 60% of their investments involve no return of capital (a way of saying that 60% are zeroed).

For accredited investors, platforms like AngelList, equity crowdfunding platforms, and syndicate investing have made this more accessible than it used to be.

Cryptocurrencies and crypto-adjacent bets

Some people treat crypto as a convex bet on monetary debasement, geopolitical fragmentation, and technology adoption all at once.

The downside is known (you can only lose what you put in), and the upside has been extraordinary in past cycles. But you want to keep these small.

Speculative stocks with asymmetric payoffs

Micro-caps, biotech with binary outcomes, distressed equities in sectors that could recover.

These are riskier than the market but they are not really convex in the same way options are. The downside is not capped the way it is with an option premium.

Your own business or a side venture

This is often “barbell” in itself because it’s people’s favorite or the one most people ignore. And it’s often the best convex bet available.

Starting something you own, where your time and a small amount of capital can produce an outsized return if it works, is a form of the barbell most sophisticated capital allocators eventually embrace. And it can fund your standard portfolio.

Step Three: Size the Convex Bet Carefully

The key insight about the risky end is that you’re not trying to make it big. You are trying to make it cheap and convex.

Universa’s capital risk in the high-risk part of its portfolio is only two to three percent of overall capital. Not ten percent. Not twenty. Just two to three. The reason is that options decay. Venture bets go to zero. Most convex bets are losing propositions most of the time, and you have to be able to keep funding them year after year without running out of money.

So the practical rule is this: your annual budget for the convex side should be roughly equal to the after-tax yield you earn on the safe side.

If your safe side is yielding 5 percent, and that represents 80 percent of your portfolio, you are earning roughly 4 percent of total portfolio value each year in yield. That’s your budget. That’s how much you can spend per year on options premiums, venture bets, crypto, and other convex exposures without eating into principal.

For traders that work in real terms (i.e., inflation-adjusted terms) and not nominal terms, then it’s even lower.

An upshot of this is that it kind of helps you avoid down years. You clip coupons on the safe side and occasionally make nice years when the risky, convex bets pay off.

That’s the elegance of the structure. The safe side funds the risky side. In normal years, the yield pays for the bets. The bets mostly don’t pan out. You end the year roughly flat or so. But every now and then, maybe every ten years, the bets pay off enormously and the portfolio has a great year.

Therein lies the logic to this approach.

Step Four: Get the Timing of the Convex Bets Right

A key point that many explanations of the barbell tend to miss: you don’t usually just set and forget the risky side.

When volatility is cheap, you buy more insurance. When volatility is expensive, you buy less, or you wait.

How do you know when volatility is cheap?

An easy way is to compare the historic realized volatility of whatever you are trading to the implied volatility going forward. This is often shown in your broker. It shows implied volatility on an options chain.

Note that what you see quoted is at-the-money.

Implied volatility exists on a curve:

The historical volatility of the S&P 500 runs around fifteen to sixteen percent annualized typically. If implied volatility is 15 and the market has been calm, insurance is priced modestly.

If implied volatility is thirty, you’re paying through the nose for insurance, and you should probably wait or reduce your exposure.

The same logic applies to venture and private investments. When everyone is pouring money into startups and valuations are stretched, your convex bets there will pay off much less, if at all. When the funding environment is frozen and valuations are depressed, that’s when convex bets in private markets have historically paid off best.

Said differently: the convex side should be counter-cyclical. Buy insurance when the machine looks stable and nobody wants it. Buy risky growth bets when everyone has given up and valuations reflect despair.

This is hard to do. It requires being less involved during periods where everything looks good and everyone is making money. You have to go opposite popular instincts. Most can’t stomach it. That’s why the barbell approach is not popular, even though conceptually it’s quite good.

Step Five: Rebalance With Rules, Not Feelings

One of the hardest practical parts of running a barbell is rebalancing when the risky side pays off.

Imagine you have 85 percent in Treasuries and 15 percent in deep out-of-the-money puts. The market crashes. Your puts go from 15 percent of the portfolio to 60 percent of the portfolio overnight. What do you do?

You rebalance. You take profits on the puts, you move the cash back into the safe side, and you re-establish the barbell. Most won’t do this. They see the puts going up, they get greedy, they hold on for the next leg down, and they give back the profits.

The practical rule is to set a rebalancing threshold in advance. If the risky side exceeds some percentage of the portfolio (say, 30 to 40 percent), you trim it back to the target weight. If the safe side grows beyond its target (which can happen in a prolonged bond rally), you redeploy some of it into the convex side.

Rules beat feelings. Write them down before you need them.

Adjusting the Barbell

Here is where the barbell gets interesting for someone thinking about today’s environment.

Early in the cycle, when debt burdens are low and the central bank has plenty of gas in the tank, the risk to the safe side is mostly inflation and the risk to the risky side is a typical recession.

In this phase, your safe side can lean heavier into longer-duration bonds because the central bank can always cut rates, and your risky side can lean toward puts on equities.

Late in the cycle, when the government debt situation is nearing the point of no return and the central bank is running out of room to cut rates, the risks are different. Long-duration bonds become dangerous because their real yields can go negative when the central bank monetizes debt.

This is when your safe side should rotate toward shorter-duration bonds, TIPS, and more gold. The risky side should include some exposure that performs in an inflationary deleveraging, not just a deflationary one. That might mean calls on gold, commodities, or hard-asset miners, alongside the equity puts.

For those who don’t want to play the tactical game, they can agree to a strategic allocation to hold through the cycle.

A Common Mistake: Confusing the Barbell With a Balanced Portfolio

A barbell is quite different than a 60/40 stocks and bonds portfolio or a standard balanced beta portfolio.

A balanced approach allocates to the middle of the risk spectrum. Stocks are moderately risky. Investment-grade bonds are moderately safe. The portfolio sits in the middle, and historically it has done fine in most environments.

But the 60/40 has most of its risk concentrated in equities, because stocks are 2-4x times more volatile than bonds. So a 60/40 in risk terms is really more like 85/15 or 90/10. Same with 80/20 stocks and bonds. Almost all the risk is in the stocks.

A true barbell puts capital in places where the risk characteristics are genuinely different, not in places that happen to have different asset class labels.

Eighty-five percent in T-bills and fifteen percent in more convex, riskier strategies is a barbell. Eighty-five percent in investment-grade corporate bonds and fifteen percent in large-cap stocks is just a conservative portfolio.

The difference is whether the risky slice is actually convex or just slightly riskier than the safe slice.

A Word on the Opportunity Cost

Let’s talk about what the barbell costs you.

In a normal market, the barbell will often underperform. And it will often underperform by a lot. If you had been running an 85/15 Treasury/puts barbell through the post-2009 recovery, you would have watched everyone else get rich in equities while you earned roughly nothing. That’s the trade. You give up the middle to get the ends.

Of course, you can diversify the convex part of the barbell so it’s venture, deep OTM puts, personal business, etc., to make it more robust.

But if people see their neighbors getting rich in stocks, or in real estate, or in tech, and they can’t stand sitting out. So they abandon the barbell right before the convex bet would have paid off.

So, the barbell is as much a psychological strategy as a financial one. It requires the ability to be patient during years of no returns and the willingness to look stupid for long stretches in exchange for looking brilliant for short ones.

Putting It All Together

Here’s what practical barbell implementation looks like for someone with, say, $500,000 in savings who wants to run this seriously:

Roughly $425,000 (85 percent) in the safe side: a ladder of T-bills rolling every few months, a modest allocation to longer-duration Treasury notes for convexity on the deflation scenario, an allocation to TIPS for the inflation scenario, and maybe $25,000 to $40,000 in physical gold or gold ETFs.

Roughly $75,000 (15 percent) available for convex bets, but not all at once. Budget perhaps $15,000 to $20,000 per year for options premiums on deep OTM puts, funded out of the yield on the safe side. Reserve some of the convex budget for venture investments, crypto exposure, or other asymmetric bets, depending on the market environment and even their own knowledge. Don’t feel obligated to use the full budget if volatility is expensive or opportunities are thin and you can even go into standard investment like stock indices.

Rebalance when the risky side grows beyond 25 percent of the total portfolio. Review the composition of both sides annually.

It’s not complicated. It’s just hard to stick to.

The people who have run this strategy successfully over long periods have a few things in common.

- They are aware of their opportunity set on the risky/convex side.

- They’re patient.

- They rebalance with discipline.

- They treat their convex bets as insurance, not as lottery tickets.

- And they accept that the reward for running this structure is not steady outperformance. The reward is survival and occasional spectacular gains to pay for the lean/breakeven years – and potentially some beyond that.

Risks To Consider

Interest rate risk

The traditional barbell portfolio of long duration bonds and short duration bonds has interest rate risk.

When interest rates rise, bond prices fall, and more so for long duration bonds. A trader may end up getting stuck with 10+ year duration securities that yield less than safer shorter term instruments had they been purchased when yields were lower.

Either the trader might sell the bond and realize a loss or bank on the bonds performing better going forward.

Inflation risk

Portfolios with a lot of nominal rate bonds face risks of inflation.

Most bonds are fixed-rate in nature. If a bond yields one percent and inflation is three percent, the trader has a real yield of minus-two percent.

Missing out on ‘stuff in the middle’

A barbell portfolio will invest in a mix of low-risk and high-risk assets with little to no allocation toward middle-of-the-road assets like safe stocks, moderate-quality bonds, and so on.

There is a time when these types of assets will outperform in absolute and relative terms. Diversifying broadly and not just on each end of the spectrum can help improve risk-adjusted returns.

A portfolio that invests heavily or exclusively in mid-duration or moderate risk assets is called a bullet portfolio.

Reinvestment risk

Reinvestment risk occurs when bonds are maturing and the yields of new debt are lower than the ones that just returned their principal.

In a low interest rate world, this is a reality for many investors. Before the financial crisis, they may have gotten 5 percent yields in safe government debt. Now they look across the yield curve and see yields of one percent or even negative nominal yields.

That leaves a lack of viable replacement securities to choose from. That means traders must look into riskier securities that have more credit risk or longer duration, or pursue riskier strategies to generate they yield they’d like.

The Barbell In A Lower Interest Rate World

The Black-Scholes model predicts that put options are less expensive when interest rates are high.

This makes sense given any drop in earnings that can cause stocks to fall can normally be “caught” by cutting interest rates.

In a low interest rate world, that process no longer normally works as designed. Put options become more expensive with less ability to offset drops in earnings with lower interest rates. That puts a premium on put protection.

Moreover, when interest rates are high, this enables barbell strategies to function well for those who rely on investing in cash and bonds to bankroll the riskier part of the portfolio.

When interest rates fall, this squeezes the barbell portfolio strategy’s potential margins on both sides.

The safe part of the portfolio returns less and the risky part of the portfolio either becomes more expensive (e.g., put options) and/or riskier.

Speculative stocks are even more expensive than normal because they’re discounted at lower interest rates and more people pile into them without much yield in other securities.

Accordingly, one might expect the barbell strategy practitioners to adapt during these periods.

The safe part of the portfolio might have to become riskier. Or else accept mild losses most years.

It may have to include bonds and other securities of lower creditworthiness or longer duration. These have more price risk and volatility. The investment manager might also have a lower allocation to the riskier side of the portfolio.

Barbell Portfolio Convexity

The barbell portfolio strategy is considered convex as it’s a trading or investing technique that seeks to exploit the benefits of both high-risk, high-return investments and low-risk, low-return investments.

The strategy involves constructing a portfolio that is heavily weighted towards either end of the risk-return spectrum.

For example, a typical barbell portfolio might be composed of 20 percent high-risk, high-return assets and 80 percent low-risk, low-return assets.

How this percentage varies will depend on what part of the cycle we’re in.

During periods where stocks and risk assets are more expensive, traders following a barbell strategy will typically put more of the portfolio into cash or short-term bonds.

How does a trader determine if stocks are expensive?

Determining whether stocks and other risk assets are expensive will typically entail the following:

- Are forward earnings multiples (i.e., P/E ratios) high relative to average?

- Are lots of new buyers in the market (e.g., retail participation in the market up, higher options activity)?

- Is inflation high relative to the central bank’s target?

- Is unemployment low? Are there very tight labor markets?

- Is the central bank tightening policy?

Advantages

The main advantage of the barbell portfolio strategy is that it allows investors to capture the upside potential of high-risk, high-return investments while still providing some downside protection from low-risk, low-return investments.

This type of portfolio construction can be especially beneficial in volatile market conditions when the direction of the market is in flux.

Another advantage of the barbell portfolio strategy is that it can help investors to diversify their portfolios and reduce overall portfolio risk.

By including both high-risk and low-risk assets in the portfolio, investors can offset the risk of any one investment with the stability of another.

This can lead to a more efficient portfolio that is better able to weather market volatility.

Disadvantages

For many traders, the barbell strategy might mean taking on too much risk for comfort.

Additionally, the barbell portfolio strategy can be difficult to rebalance on a regular basis, which can lead to sub-optimal results over time.

Despite these disadvantages, the barbell portfolio strategy can be a useful tool for traders who are looking to capture the upside potential of high-risk, high-return investments while still providing some downside protection.

When used correctly, the barbell portfolio strategy can lead to superior risk-adjusted returns and a more efficient overall portfolio.

Pension Funds & Bonds

Pension funds follow a similar concept to the barbell portfolio strategy.

When risk assets go up, they often look to sell in order to buy assets of less risk.

Conversely, when risk assets fall, they often look to buy them by selling off safer assets.

As a result, the strategy of pensions is quite analogous to the central idea behind the barbell portfolio strategy.

Barbell Investing Strategy FAQ

Why is a barbell structure best with a flattening yield curve?

When a yield curve is flat, it incentivizes traders and investors to put more of their capital into shorter-duration bonds that have equivalent yields as longer-duration bonds with the benefit of lower price risk.

A flat yield curve also signals economic slowdown may be likely, which makes risk assets less attractive to own.

Having more of a barbell structure, in that case, can make more sense.

How can the barbell portfolio strategy help investors diversify their portfolios and reduce overall risk?

By including both high-risk and low-risk assets in the portfolio, traders can offset the risk of any one investment with the stability and capital preservation of another.

This can lead to a more efficient portfolio that is better able to tolerate the large ups and downs associated with risk assets.

What are some of the main disadvantages of the barbell portfolio strategy?

The main disadvantage of the barbell portfolio strategy is that the trader must purchase enough high-risk, high-return assets to achieve the desired weighting in the portfolio.

For many traders, this might mean taking on too much risk for comfort.

Additionally, the barbell portfolio strategy can be difficult to rebalance on a regular basis, which can lead to sub-optimal results over time.

For example, if a trader is 90 percent stocks and 10 percent bonds because they perceive that risk assets are weak, and stocks fall in price some more, they might not be able to pick up bargains because they’re already “fully invested”, or essentially maxed out on their allocation.

Moreover, a barbell portfolio is not the same thing as a balanced portfolio.

A balanced portfolio will try to avoid environmental biases.

A barbell portfolio is still heavily skewed toward risk. Even if a portfolio is 60/40 stocks/bonds, stocks are more volatile than bonds, so the risk weighting is more like 90/10.

An 80/20 stocks/bonds portfolio has almost all of its risk in the stocks portion.

Holding cash against risky assets can help lower a portfolio’s overall risk, but not balance it very well.

Despite these disadvantages, the barbell portfolio strategy can be a useful tool for traders who are looking to capture the upside potential of high-risk, high-return investments while still providing some downside protection.

When used correctly, the barbell portfolio strategy can lead to superior risk-adjusted returns and a more efficient overall portfolio.

Do institutional traders use the barbell portfolio strategy?

Yes, institutional traders often use the barbell portfolio strategy or strategies analogous to it to achieve their desired risk and return profile.

However, because they have access to a wider range of assets, more capital, and a wider range of products (e.g., swaps), they are often able to take on more risk than individual traders.

This can lead to higher returns, but it also means that their losses can be amplified during periods of market volatility.

How can traders implement the barbell portfolio strategy?

There are a few different ways that investors can implement the barbell portfolio strategy.

One way is to invest in two separate portfolios, one that consists of high-risk, high-return investments and another that consists of low-risk, low-return investments.

The investor would then allocate a portion of their total capital to each portfolio based on their desired risk/return profile.

Another way to implement the barbell portfolio strategy is to invest in a single portfolio that consists of both high-risk, high-return investments and low-risk, low-return investments.

The investor would then allocate a portion of their total capital to each investment based on their desired risk/return profile.

Does the barbell portfolio strategy have any rules associated with it?

A trader may be “fully invested” when 90 percent of assets are in stocks or other risk assets and 10 percent is in cash or short-term bonds.

In other words, a trader might have a rule of always having 10 percent of assets in cash as a prudent buffer zone.

This cash can help to lower the overall risk of the portfolio and make it easier to rebalance during periods of market volatility.

Conclusion

The barbell portfolio strategy is a popular investment strategy that allows investors to capture the upside potential of high-risk, high-return investments while still providing some downside protection from low-risk, low-return investments.

There are a few different ways that investors can implement the barbell portfolio strategy.

One way is to invest in two separate portfolios, one that consists of high-risk, high-return investments and another that consists of low-risk, low-return investments.

Another way to implement the barbell portfolio strategy is to invest in a single portfolio that consists of both high-risk, high-return investments and low-risk, low-return investments. The investor would then allocate a portion of their total capital to each investment based on their desired risk/return profile.

The barbell portfolio strategy is not straightforward as to how to rebalance on a regular basis, which can lead to sub-optimal results over time.

This type of portfolio construction can be especially beneficial in volatile market conditions when the direction of the market is uncertain. While there are some risks associated with this strategy, it can be a useful tool for investors who are looking to achieve better risk-adjusted returns.

Appendix

Risk and Return Metrics

| Metric | S&P 500 | Balanced | Barbell |

|---|---|---|---|

| Arithmetic Mean (monthly) | 0.95% | 0.73% | 0.70% |

| Arithmetic Mean (annualized) | 11.99% | 9.08% | 8.68% |

| Geometric Mean (monthly) | 0.84% | 0.70% | 0.67% |

| Geometric Mean (annualized) | 10.61% | 8.74% | 8.39% |

| Standard Deviation (monthly) | 4.55% | 2.28% | 2.12% |

| Standard Deviation (annualized) | 15.75% | 7.91% | 7.33% |

| Downside Deviation (monthly) | 2.95% | 1.23% | 1.13% |

| Maximum Drawdown | -50.89% | -17.23% | -21.61% |

| Stock Market Correlation | 1.00 | 0.64 | 0.53 |

| Beta(*) | 1.00 | 0.32 | 0.25 |

| Alpha (annualized) | 0.00% | 5.08% | 5.55% |

| R2 | 100.00% | 40.65% | 28.10% |

| Sharpe Ratio | 0.44 | 0.54 | 0.53 |

| Sortino Ratio | 0.64 | 0.85 | 0.84 |

| Treynor Ratio (%) | 6.93 | 13.35 | 15.83 |

| Calmar Ratio | 0.39 | 0.10 | -0.18 |

| Active Return | 0.00% | -1.87% | -2.22% |

| Tracking Error | 0.00% | 12.32% | 13.40% |

| Information Ratio | N/A | -0.15 | -0.17 |

| Skewness | -0.51 | 0.09 | 0.13 |

| Excess Kurtosis | 1.88 | 1.37 | 1.59 |

| Historical Value-at-Risk (5%) | 7.12% | 2.87% | 2.51% |

| Analytical Value-at-Risk (5%) | 6.53% | 3.03% | 2.78% |

| Conditional Value-at-Risk (5%) | 10.01% | 4.08% | 3.85% |

| Upside Capture Ratio (%) | 100.00 | 41.17 | 35.06 |

| Downside Capture Ratio (%) | 100.00 | 21.95 | 13.34 |

| Safe Withdrawal Rate | 4.30% | 5.20% | 4.92% |

| Perpetual Withdrawal Rate | 6.05% | 4.43% | 4.12% |

| Positive Periods | 391 out of 626 (62.46%) | 397 out of 626 (63.42%) | 399 out of 626 (63.74%) |

| Gain/Loss Ratio | 1.03 | 1.32 | 1.37 |

| * US stock market is used as the benchmark for calculations. Value-at-risk metrics are monthly values. | |||