The Discounted Future: Backing Out What Markets Think

Financial markets represent the discounted future.

One of the most common mistakes traders make is their perception that the present reality is a certain way and that biases their opinion on markets. Everything is already discounted into the price.

In a previous article we walked through the big three market equilibriums that every trader and investor needs to watch, and we described the “risk premium” sitting between the different asset classes.

That risk premium helps tell you what the discounted future looks like.

Think of the economy this way: every day it takes everything people believe about growth, inflation, policy, security-specific factors, and a multitude of variables, and stamps a price on it. Cash gets a yield. Bonds get a yield. Stocks get an implied yield.

The gaps between those yields are part of the market’s bet on what comes next.

The price already contains a forecast. When you buy the S&P 500 at some level, you are not buying “stocks.” You are buying a specific set of assumptions about earnings growth, government yields, about where the Fed pegs cash, about how much extra return you’ll demand for taking equity risk. Back those assumptions out and you can hold them up against what’s actually realistic. For example, do cross-asset assumptions make sense?

Most traders never run it. They glance at a price, decide it feels high or low, and stop there. Backing out the forecast inside the price is slower work, and it’s the difference between guessing and knowing what you’re actually betting against.

Key Takeaways

- Markets price the discounted future, not the present. The yields on cash, bonds, and stocks, and the spreads between them, tell you what’s already baked in. Your job is to work out whether those expectations are realistic. For stocks, P/E ratios and earnings yield give you forward expectations of earnings and growth. It’s not “is this good or bad?”; it’s “is this good or bad relative to what’s already discounted in the price?”

- Late in the cycle, the spreads get too thin. People extrapolate the good times. Forward yields on stocks drop, credit spreads compress, and you end up taking the same risk for less reward. Are you being compensated well enough?

- Watch what the central bank is doing before you act on valuation. Expensive assets can stay expensive, or get even more expensive, when the central bank is easing/accommodative. Cheap assets can get cheaper when it’s tightening and less accommodating (usually to fight inflation). Policy beats price in the short run. Price is accordingly less of a trading signal.

- In the end, money printing is always expected. Heavily indebted countries with debt in their own currency don’t default the way a household does. They lower rates, refinance (extend the durations), and/or buy the debt (“monetizing the debt”), and the cost shows up in the currency instead, all else equal. Over time that’s good for things like gold. It doesn’t necessarily mean it’s bad for the national currency relative to another one (especially a country with analogous problems).

- Currency depreciation is zero-sum. When one currency falls it helps that country at the expense of another. It doesn’t produce the global easing that a coordinated drop in interest rates does. Distributional effects of a depreciation generally favor exporters over consumers.

- Sentiment works best as a contrarian read. Markets top and bottom when there are no buyers or sellers left at the margin.

- You can back out the discounted price for every asset class. Stocks through the forward earnings yield and a discounted cash flow. Bonds through the real yield and the forward curve. Commodities through the futures curve. Currencies through the interest rate differential(s).

- Great past returns don’t mean great forward returns. If profit margins and price-to-earnings multiples revert toward their long-run averages, the next decade can look nothing like the last one.

The big three yields you have to watch

Start with the three numbers that anchor everything else.

What’s the yield on cash?

Where does the central bank have its policy rate pegged?

Cash usually means the overnight rate the central bank controls, the three-month rate, or really anything with a duration under one year with little to no nominal price risk.

This is the risk-free floor. Every other return in the system gets measured against it.

What are the yields on bonds?

What are rates further out along the yield curve, at two years, five years, ten years? And what do bonds of different credit qualities pay?

The gap between a Treasury and a corporate bond of the same maturity is the market’s price on default risk and growth.

What’s the “yield” on stocks?

Stocks don’t pay an explicit yield, so you infer it. Stock yields are a residual – what do owners receive after everything else has been paid?

Project out earnings, divide by the value of the index, and you get an implied forward yield. The price-earnings ratio is one version of this. See a forward P/E of 16 and the reciprocal, 1 divided by 16, is your implied forward yield. That’s 6.25%.

Looking at the yields across cash, bonds, and stocks matters because together they show you the discounted future. One number alone tells you almost nothing. The relationships between them tell you a lot.

That 6.25% yield looks good when yields are 0% (risk premium of 625bps) and looks less attractive when risk-free yields are 5% (risk premium of just 125bps).

Later in the cycle, the spreads between cash and bonds, cash and stocks, and bonds and stocks tend to get too low. Why? Because people get overly optimistic about the future. They extrapolate the recent past and assume current conditions will just keep going. When that happens, assets become fully priced or overpriced, and you’ve got a decision to make.

Do you want to own a lot of stocks when their forward yields are lower than they were and the risks haven’t changed? If you’re a short-term trader, do you want to keep biasing your decisions long? Your reward relative to your risk just got worse.

Do you want to own a pile of longer-duration bonds when the yield is tiny but the volatility is just as large as ever?

Trading is fundamentally about the risk you’re taking relative to the reward you’re getting. If you’re holding assets mainly for their yield, these are the questions you can’t skip. A few other data points help fill in the picture of what to expect going forward.

How do you read the discounted future?

Five questions. Work through them and you’ll have a decent read on where you are and what’s already in the price.

1. What are the unemployment rates?

Low unemployment regularly goes hand in hand with low credit spreads and high risk-asset prices. Said differently, riskier credits start yielding closer to the risk-free sovereign rate, and the forward yields on stocks start looking unattractive relative to their risks. It means businesses are broadly doing well and there’s plenty of liquidity in the system.

But central banks tend to start pulling that liquidity back toward the later stages of the cycle, because they see inflation ticking up or expect it to. That’s exactly where they were in Q4 2018, raising interest rates. They overtightened. Then they reversed and went back to easing, which was necessary to keep the expansion alive and to support financial asset prices, which are very much part of the health of the real economy (as they affect wealth, collateral values, credit creation, and other factors).

When unemployment is low, it tells you the capacity to squeeze more out of the current cycle is limited. Fewer workers are left to join the workforce and push growth higher. At this phase growth risks are skewed to the downside. Growth can’t get much better, because the economy is already running at or near, maybe even a touch above, its operating capacity. But hit it with a credit or liquidity crunch and growth can get a lot worse, fast.

When relatively late in the cycle, high forward returns for stocks, bonds, and risk assets aren’t very likely. Some investors and traders pull back their allocation to risk during this phase. That’s a reasonable response to a thin reward.

2. What is the central bank doing?

Even when asset prices are high, that alone doesn’t make it a good time to sell.

Are the central banks easing? The ones that matter most sit in the jurisdictions of the top three or four reserve currencies: the US Federal Reserve, the European Central Bank, the Bank of Japan, and the Bank of England. Are they cutting rates? Are they buying assets?

If a central bank provides enough liquidity, that liquidity finds its way into assets. This is the part people get wrong when they sell purely because something looks expensive.

Even in heavily indebted societies, as long as the debt is denominated in the domestic currency, the central bank can lower rates and buy the debt. At that point, instead of the cost of all that borrowing showing up in the sovereign credit through higher yields (more debt means more risk), it gets diverted into the currency channel. The currency depreciates instead.

Take Japan. It’s a deeply indebted country, with sovereign debt around 250 percent of annual GDP. And yet the debt is overwhelmingly denominated in yen, with interest rates only slightly positive across most of the curve. So the debt-service burden is low and not particularly risky. The bill doesn’t disappear. It just gets paid in a different currency than you’d expect.

Now, once rates are maxed out on the downside, and relative interest rates can’t move much because they’re already at zero or somewhat negative, currency volatility has to pick up to avoid economic volatility. To keep growth from taking the hit, countries lower their exchange rates instead.

This is what leads to “currency wars,” to fixed exchange rate breakups, and to larger currency risk for traders generally. It also tends to boost the value of alternative money like gold.

But the catch with currency depreciation is that it’s zero-sum. When one currency falls, it helps that one country at the expense of another. It doesn’t bring about a global easing the way a coordinated drop in interest rates does, that’s the primary form of monetary policy, or the way asset buying does, the secondary form. One country exports its problem. The world as a whole gets no relief.

3. How is debt tracking relative to earnings and output?

Even if debt is rising faster than incomes and earnings, that doesn’t mean trouble is imminent. It depends entirely on the servicing.

If you owe a billion dollars but it’s not due for another year, you’re fine in the near term, even if the longer term looks scary because you haven’t figured out a solution yet. And there are only so many solutions. You can:

- extend the maturity to buy yourself more time

- lower the rate to make the payments easier

- put the debt on someone else’s balance sheet (e.g., Maiden Lane LLC during the financial crisis)

- write-down the debt, which is basically defaulting and paying only part or nothing

- run austerity measures, spending less so you have more cash flow and can prioritize the debt

- and if you’re a sovereign government, you can print money to relieve the burden

That list isn’t random. It maps almost one-for-one onto the four levers for getting through a debt problem: austerity, debt defaults and restructurings, debt monetization (printing money), and wealth transfers from the haves to the have-nots.

Each lever lands differently on the economy and on creditworthiness. The whole job is getting debt and income growth back in line with each other.

In the US and other countries, we were nowhere near in line in 2006 and 2007. Right now we’re broadly there. Debt and output are growing at about the same pace in aggregate, with no runaway debt growth in any single sector. That’s a healthier setup than the one that preceded the last crisis.

Still, debt growing faster than income is not a sustainable set of conditions. Eventually balance sheets top out and lenders get more cautious. It doesn’t break all at once. Lending just gets tighter until someone notices.

4. What’s the level of sentiment?

Sentiment is really a question of how other investors are positioned.

A few ways to gauge it.

First, what’s the speculative positioning across markets? You can pull this for free from the CFTC, which publishes long and short positioning across commodities, equities, fixed income, currencies, and rates. Second, the various investment banks put out both soft data, surveys of what people expect, and hard data, what’s actually happening right now. The survey measures take the pulse of what their brokerage clients are doing. Other useful metrics include equity allocation as a percentage, cash allocation, the beta of clients’ top equity holdings, and the banks’ own bull and bear indicators.

Markets classically top or bottom when there are no new buyers or sellers left at the margin. When a market is stretched long or short, the risk of going along with the consensus grows the bigger that consensus gets.

We saw it in July 2018, bullish bets at a record high with WTI crude up in the $70s. We saw it again in gold and Treasuries, with large short positions in Q4 2018. In each case the crowd had already placed its bet, so there was almost no one left to push the price further in that direction.

That’s why these readings work best as contrarian indicators. When everyone is on the same side of the boat, it doesn’t take much for the boat to flip.

5. How much growth is already baked into prices?

Lower credit spreads mean higher bond prices, which means higher expected growth is baked in. Same logic for equities. Using a discounted cash flow, you can back the expectation out and hold it up against what’s realistic.

There’s no single fair value handed down from above. There’s only the price that corresponds to your assumptions, which is why backing those assumptions out, asset class by asset class, is worth doing carefully.

Backing out the discounted price, asset class by asset class

Every market gives you a way to reverse-engineer what it already expects. The instrument differs, but the idea is identical.

Find the price, find the cash flows or the carry, and solve for the forecast that’s sitting inside the number.

Stocks

Stocks don’t have a stated yield, so you build one from the forward earnings multiple. If stocks trade at a forward earnings multiple of 20 times, the inverse is the yield: 1 divided by 20, or 5 percent. That 5 percent is what the market is implicitly paying you, before any growth.

From there, you add growth and subtract the return you demand over cash. Take the current index price as a given and solve for the current earnings and growth rate that would justify it. If the implied growth is well above anything the real economy has produced in decades or could conceivably produce, the market is discounting a future that probably won’t show up.

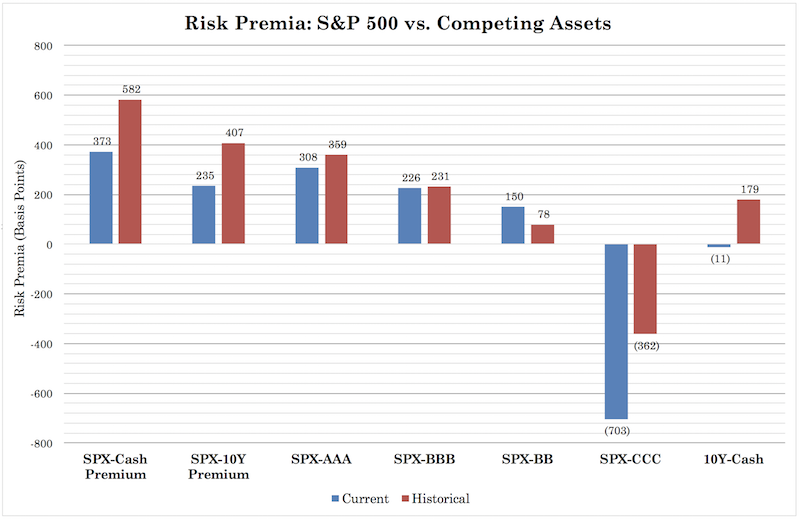

The equity risk premium is the number to keep your eye on here, the extra yield stocks offer over cash and over bonds. When that premium is fat, you’re being paid to take equity risk. When it’s thin, like it tends to get late in the cycle, you’re taking the same risk for less.

Equity risk premiums also can take a long time to climb back to their pre-downturn lows after a big decline (unless there’s a big stimulus), so don’t expect a quick reset once they’ve compressed.

Example

Let’s say a stock index is 10,000 and earnings are 500 (i.e., 5% one-year yield). What growth would be necessary to make this index fair value if you expect a 5% return over cash and the cash yield is 3.5%?

Required return:

- cash return 3.5 percent

- plus equity risk premium 5 percent

- equals required index return of 8.5 percent

Current earnings yield:

- Earnings of 500 divided by index level 10000 equals 5 percent

So required growth is:

- 8.5 percent required return

- minus 5 percent earnings yield

- equals 3.5 percent growth

So the index would be fair value if long term earnings grew about 3.5 percent per year, assuming the 5 percent earnings yield is a reasonable proxy for shareholder yield and valuation multiples don’t change.

Bonds

Bonds are the easy case, because the discounted future is printed right on them. The yield is the forecast.

A bond yield consists of two parts: the expected inflation rate and the expected real yield. Both matter for the value of money and debt as a store of wealth and as a cost of funds.

The real bond yield, what you can earn free of inflation, is the most important number to watch in the entire financial world. It’s the most foundational rate in all of capital markets, the one everything else gets priced off.

The yield curve does the rest of the work. The relationship between short rates and long rates tells you what’s expected. When short-term rates sit high relative to long-term rates, money is tight, and holding and lending cash becomes more attractive than borrowing and investing elsewhere. A flat or inverted curve is the market discounting cuts ahead. From the curve you can pull out the forward rates, which back out exactly what the market expects the central bank to do and when.

Credit spreads finish the picture. A wide spread between a corporate bond and a Treasury of the same maturity discounts more defaults and weaker growth. A thin spread discounts the opposite, that the good times continue and nobody misses a payment. When spreads get very thin, the bond market is telling you it sees no trouble coming, which, late in the cycle, is precisely when you should be most skeptical.

Commodities

Commodities have no earnings and no coupon, so the discounted future lives in the futures curve.

When the futures price sits above the spot price, the market is in contango, and it’s discounting some combination of storage costs, financing costs, and comfortable supply. When the futures price sits below spot, that’s backwardation, and it’s usually telling you supply is tight right now and buyers are paying up for immediate delivery. The shape of that curve is the forecast. Read it the way you’d read a bond curve. And watch the roll, what you earn or lose each time a futures contract expires and you move into the next one. That carry can quietly dominate your return over a year, whatever spot does.

Growth-sensitive commodities like oil and copper trade on the expected strength of the economy, so their curves and the level of inventories back out what the market expects demand to do.

Gold works differently. It pays nothing, so it competes directly with cash and bonds that pay a real yield. When real interest rates fall, especially when they go negative, the opportunity cost of holding gold falls and gold tends to rise. That’s why gold does well in exactly the environment we described earlier, when central banks have rates low relative to cash and bond investments, the currency is being debased, and there’s nowhere safe left to earn a quality real return.

Currency weakness, especially against gold, is the tell.

FX (exchange rates)

When the EUR/USD exchange rate is 1.15, what does that actually mean?

Fundamentally, it’s the market price of euros in dollar terms. It tells you how many dollars investors, banks, companies, and traders are willing to pay for one euro right now. In economic terms, 1.15 reflects relative money demand, interest rate expectations, inflation expectations, trade flows, capital flows, risk sentiment, and central bank credibility between the euro area and the US.

Currencies look like the hardest market to read, but the discounted future is right there in the interest rate differential.

The forward exchange rate isn’t a prediction in the way people assume. It’s set mechanically by the gap between two countries’ interest rates.

A currency with higher interest rates trades at a forward discount to one with lower rates, by roughly the size of the rate gap. So the forward rate already “discounts” the difference in monetary policy between the two economies. That’s your baseline. The market expects the high-yielder to depreciate by about the amount of its yield advantage. You see this discounted into the futures markets between the two currencies (if they exist and are liquid).

The opportunity shows up when you think a currency will move more than that baseline.

Here’s the rule worth memorizing: if a currency falls against another currency at a rate greater than its interest rate, the holder of debt in the weakening currency loses money.

So when a country is monetizing its debt, running large capital outflows, or carrying a lot of debt denominated in a foreign currency, you’d expect the currency to fall by more than the rate differential. Being long that currency, even at a juicy yield, ends up costing you.

This is the channel we talked about with Japan. Once rates are stuck at zero and can’t be cut further, the adjustment has to come through the exchange rate. The real exchange rate against trading partners is what to track, not the headline number. And remember it’s zero-sum. A weaker currency helps one country and hurts another, so currency depreciation never produces the broad global easing that lower interest rates do.

Measuring things out

Put it all together and you can measure cash against bonds and stocks, and bonds against stocks.

Stocks have no explicit yield, so use the forward earnings multiple again. A forward earnings yield of 20 times gives you a yield of 5 percent. Now you can line all three up on the same scale and read the spreads.

Take a quick example. If cash is yielding about the same as long-duration bonds, that’s the market telling you to expect monetary policy to be eased at some point. The front-end rates should come down to push the cash-to-bonds spread back toward a more normal risk premium. The flat spread isn’t “market irrationality” but a forecast of cuts.

Run the stock side the same way. Say cash yields 2 percent, the ten-year bond yields 3 percent, and stocks carry that 5 percent forward earnings yield. The stock-to-cash spread is 3 percent and the stock-to-bond spread is 2 percent. Those gaps are your equity risk premium, the reward for owning equities over the safer alternatives. When the spreads are wide, stocks are paying you to show up. When they compress toward zero, you’re being asked to hold equities for almost no extra return over a government bond, and that’s usually a late-cycle warning rather than a reason to buy.

Take this example (not meant to be representative of today).

Discounting and extrapolations

Most of what’s discounted into markets comes from extrapolating the past, because the past is the only frame of reference people have. That’s human, and most of the time it’s roughly fine. The trouble, and the opportunity, comes when something is going on that makes those extrapolations unlikely to play out.

For instance, US investors surveyed at the end of 2021 said they expected annual returns of 17.5 percent going forward. Think about that. Returns like that would 5x your money every decade.

It made sense why they expected it, though, sitting where they sat. The decade from the end of 2011 to the end of 2021 had delivered 16.6 percent a year. So they just drew the line forward.

But where did those returns actually come from? Mostly from enormous monetary stimulus after the 2008 recovery. And the very thing that made those returns look so good looking backward is what makes returns less going forward.

Stimulus can only be stretched so far. Interest rates can’t go far below zero. Bond rates can’t go far below zero either. Fiscal stimulus combined with supportive monetary policy can only run so long, given the trade-offs of inflation, asset bubbles, and currency devaluation. Once inflation becomes a problem and financial stability starts to crack, through bubbles or currency strain, the supportive policy has to be toned down.

The trade-offs force policymakers’ hand.

And there’s a second trap hiding in low rates. When interest rates are very low, the duration of financial assets lengthens, which makes them more sensitive to any rise in rates. So the same low rates that pumped the asset prices up are what leave those prices fragile when rates eventually turn.

The lesson is simple, and worth repeating. Great past returns don’t mean great forward returns. If profit margins and price-to-earnings multiples revert to the mean, stock returns going forward could be nothing spectacular at all.

Conclusion

The future and the dollar-weighted expectation of the future is already in the price.

That’s why trading is so difficult. It’s not “is this good or bad?” but “is this good or bad relative to what’s discounted in the price?”