Trading US Short-Term Interest Rates

Like any financial instrument, short-term interest rates are tradable. While the federal funds rate is under the purview of the Federal Reserve, traders can anticipate the future direction of interest rates several years into the future.

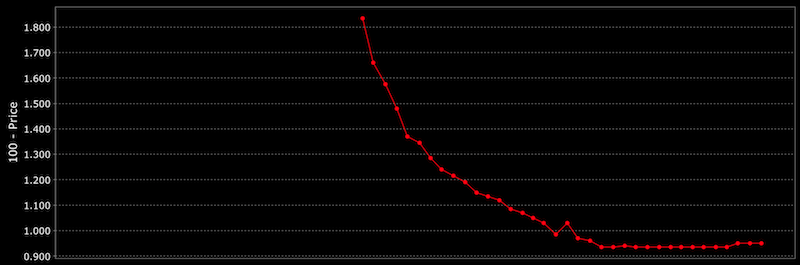

Traders price the fed funds rate to move down to just below 100bps (1 percent) in perpetuity. (This chart goes out three years.)

During the next recession, if that comes within the next three years, we would expect that rate to be back to close to zero. (During the last recession, the Federal Reserve set it within a range of 0-25bps, where it averaged around 16bps for approximately seven years.)

If you believe the US will fall into recession within the next 2-3 years, a potential trade opportunity would be going long either fed funds futures (ZQ, traded on the Chicago Mercantile Exchange) or eurodollars (GE on CME). Going long interest rates means expecting a decline. Just like when you’d trade a bond long, you expect its price to increase and its yield (the effective rate of interest paid on it) to decrease.

Eurodollars represent offshore USD time deposits and is one of the deepest and most liquid institutional markets in the world. It follows the fed funds futures market.

(You do not necessarily need prime brokerage arrangements for access to interest rate products. For example, many, including fed funds and eurodollar futures, are accessible through a broker-dealer such as Interactive Brokers.)

The prices between fed funds and eurodollars are typically separated by a small spread. This reflects the extra credit risk associated with offshore USD time deposits given they are not regulated directly by the Federal Reserve. So, eurodollars are slightly riskier.

Fed funds futures (ZQ) and eurodollar futures (GE) are priced as 100 minus their expected discounted rate over one month. For example, if the fed funds rate is expected to be 1.5 percent by December, then ZQ for the December contract would be priced as 98.5 (100 minus 1.5).

Currently, call options on GE 99 calls – i.e., expecting the fed funds rate to be less than 1 percent (in addition to the eurodollar related spread) by a certain period – on the Dec 2021 expiry are trading at about 0.30.

To put this into concrete dollar pricing, this is 0.30 multiplied by the cost of one eurodollar contract (which is $2,500 per percentage point, so 0.3*2,500 = $750).

This means if the Fed cuts rates to exactly zero and keeps them at zero by Dec 2021, then your approximate return will be 100bps minus the cost you paid for it, or 1.00*2,500 minus 0.30*2,500, or $1,750.

The reward to risk of this trade would be $1,750 divided by $750 or 2.33x. As an option, your downside is limited to $750 per contract.

You can trade short-term US interest rate through fed funds futures directly, ZQ. Fed funds futures, however, is a less liquid market and also doesn’t have expiries that extend out as far as GE.

Fed funds extends out three years; eurodollars extend out ten years.

Options on fed funds, ZQ, extend out two years; on eurodollars, GE, they extend out four years.

Moreover, if you are a trader that has a bias to be long equities, then being long eurodollars (or fed funds) acts as a form of a direct hedge. Lower interest rates are good for equities, holding all else equal, because lower rates increase their present values.

However, central banks typically cut rates in response to slower growth, which is bad for equities because it typically means lower corporate profits. They may also cut rates in response to less clarity on the forward growth and inflation outlook, and when there’s a credit or liquidity crunch (also bad for stocks). In some way, being long eurodollars can act as a form of insurance on portfolios that are long risk assets.

Trading is heavily about reward relative to risk. Even though rates 2-3 years out have rallied significantly in 2019, I believe that being long short-term rates 2-3 years out is still a reasonable opportunity. If a recession doesn’t come in 2-3 years with the Fed skillfully managing the situation, short-term rates are still likely to be around the 1 percent range. If there’s a recession, then rates are virtually guaranteed to be back at zero to go along with quantitative easing.

The Fed’s path moving forward

The nice thing about trading interest rates, specifically short-term interest rates, is that the only thing that’ll make you right or wrong is what the central bank does. Unlike equities, which are the most prone of any asset class to narrative related distortion, the central bank will either move rates in your direction or to your expected point, or they won’t. They will fluctuate in the near-term, but in the end, trading short-term interest rates is a pretty black and white game.

I expect US short-term interest rates to be back at zero in the future, likely within the next 2-3 years, so that’s personally what I’m betting on (by being long eurodollars). The central bank’s ability to get the balance right is more difficult to do as time goes on.

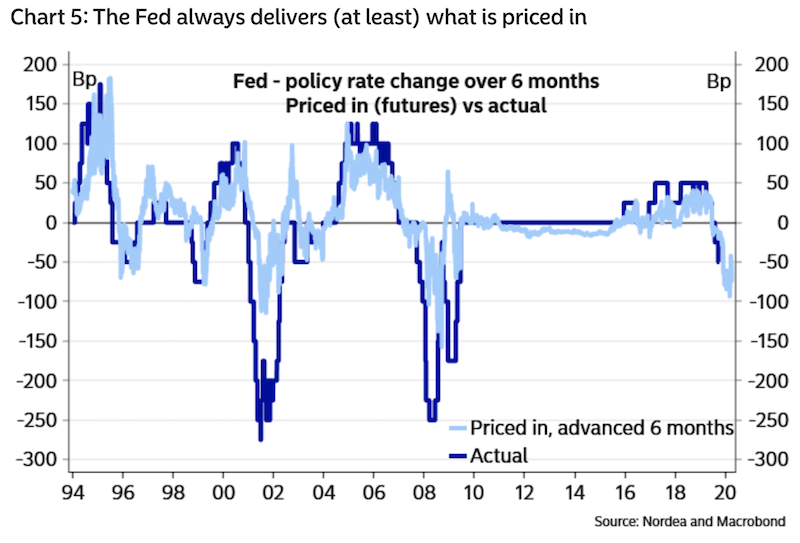

While historical information is not always helpful (the future can be different from the past), the Fed tends to deliver more cuts than what the market prices in.

The Federal Reserve’s central mandate – maximum employment within the context of price stability – pays attention to the operating rate of the economy relative to its capacity. But it pays little attention to whether the debt that’s being produced can be serviced despite how important keeping tabs on that is.

If a central bank is only looking at growth and inflation, and debt is being created for the purchases of assets that won’t generate the cash flow to justify the amount of debt being created, the central bank is directly responsible for that.

Debt growth and debt serviceability must be in relative alignment. If credit growth is too low, then the economy won’t grow to its potential. If credit growth is too high, then eventually that will create a problem if not controlled.

And it’s especially a problem when that debt is denominated in a foreign currency. This is common in emerging markets because they want to lock in lower rates and make it easier to sell to foreigners if it’s in a reserve currency (typically the US dollar and, to a lesser extent, the euro). When debt is denominated in a foreign currency, it can’t be controlled in all the usual ways, such as changing the interest rates. These countries are at the whim of what a foreign central bank does with its monetary policy. Moreover, when domestic incomes are denominated in local currency and debts are denominated in another currency, when the local currency depreciates, this is effectively an increase in interest rates. This makes the debt harder to service. This type of problem was part of the issue in the recent crises in Argentina and Turkey.

The US economy is running at a pretty normal pace – about 2 percent year-on-year growth (at capacity) and about 2 percent year-on-year inflation (approximately at the Fed’s target). But we’re still in a situation in all developed markets where their economies are highly indebted. Raising interest rates even slightly has no trouble slowing developed market economies down given that extra interest tacks on a large amount of extra debt servicing.

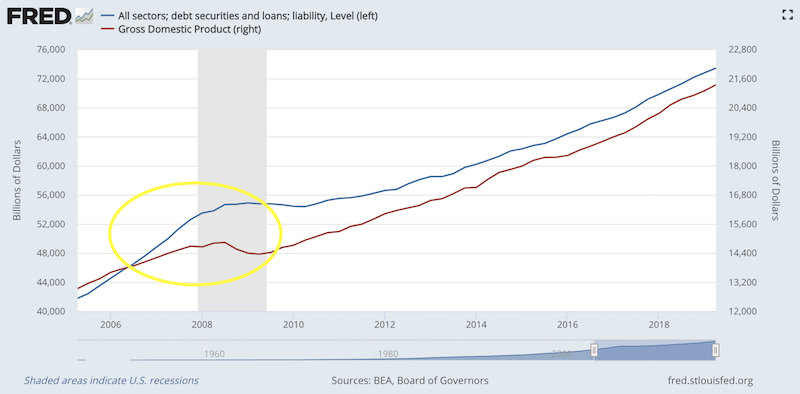

For example, in the US, there is about $75 trillion worth of debt among all sectors of the economy, inclusive of households, corporate entities, and local and sovereign governments.

A 25-bp increase (+0.25 percent) in interest expense on that pile of debt would require an extra $187.5 billion in debt servicing costs per year. That’s close to 1 percent of GDP. An extra $187.5 billion diverted into debt servicing means less is available for consumption and investment. That amounts to roughly $570 per US citizen.

While the current operating rate of the economy relative to operating capacity is important to track, losing sight of how fast debts are rising in comparison to income is also important. The rises in debt and income have roughly been in line this cycle unlike in the 2006-07 period.

But this can become especially hard to manage when there’s already a high amount of debt and the capacity to adjust interest rates going forward is limited. This means secondary monetary policy, such as quantitative easing, is likely to become a perpetual norm throughout all developed market economies.

The role of quantitative easing moving forward

It’s important for traders to understand what central banks are doing policy wise at all times and what the effects of these policies are likely to be. Quantitative easing (“QE”) means putting money (also known as “liquidity”) into the financial system.

The Federal Reserve – and other reserve currency central banks (ECB, BOJ, BOE, SNB, RBA) – will buy securities from the private sector. Normally, these are government fixed-income securities but the ECB, BOJ, and SNB have ventured into corporate debt markets as well (BOJ even into equities).

The central bank puts these securities on its balance sheet. The private sector market participants – commercial banks, institutional investors, and others – will receive cash in return.

The seller of these assets (the private sector) will be motivated to buy something similar to what they had previously owned, such as a security of similar risk and return properties. The idea is that provided enough asset buying activity from the central bank, this will eventually push investors into riskier assets, driving up their price, and creating a wealth effect.

This can take an enormous amount of spending from central banks. Where do they get this money? They create it, sometimes metaphorically referred to as “printing money”. The influence of “printing money” on supply often has an impact on the exchange rate. A higher supply of currency means a depreciation of said currency, holding all else equal.

During the QE period since the 2008 financial crisis, central banks purchased about $15 trillion worth of financial assets. And there’s a long chain of events before the wealth effect from higher asset prices flows into spending in the real economy. There hasn’t been much goods and services inflation, though since the beginning of 2009 we have seen plenty of financial asset inflation over this past cycle.

QE also increases future inflation expectations. More credit creation means more spending and thus is bound to influence prices. So, its mechanical impact on closing the spreads between cash and longer-duration bonds isn’t as clear-cut. While getting rates down further out along the curve is the intention to boost credit creation, it will help in getting real (inflation adjusted) rates down, but not necessarily nominal rates.

QE will continue to be a part of the easing policies in the US, EU, and Japan, but it won’t be as effective as last time. The spreads between short-term and long-term interest rates is no longer as high. Moreover, the forward expected returns of these assets are no longer as high despite comparable risks.

So, the big question is what the effectiveness of QE will be when the next downturn comes along.

What will be most interesting is what traders will do will when asset prices get so high that they’ll be buying assets with very little forward returns but with high risks.

We can already see this with respect to many forms of bonds. Their forward return to risk ratios don’t make much sense as investments. Sovereign bonds in various parts of the EU yield negatively even when their durations are very long.

For example, the Switzerland 50-year bond yields nothing to slightly negative; yet because of its duration, all it would take is a 100-bp increase in interest rates for that bond to lose 50 percent of its value.

Bonds in other countries are comparable. US long-duration bonds yield 1.50 to 2.00 percent. A very small fluctuation in interest rates can wipe out your expected return for the year. German bunds, the EU’s top reserve asset, yield negatively out 30 years.

That’s an extreme level of risk for something that gives you no return or negative return – not only no nominal return, but even worse return (more negative) in inflation adjusted terms.

Conclusion

Interest rates are the bedrock of finance and the foundation of the financial asset markets. They represent the price of credit and determine the valuation of asset prices through the net present value effect.

We are in a situation in developed markets where interest rates are zero, negative, or likely to become zero within the next few years. With respect to US short-term interest rates, you can bet on them directly through the fed funds (ZQ) and eurodollar (GE) market.

When short-term rates are at zero, this means central banks will move to secondary monetary policy, relying on asset purchases to lower longer-term rates, known as quantitative easing or QE.

QE means putting money (“liquidity”) into the financial system. When we think about a debt security, a loan or a bond, it’s a promise to deliver currency in the future. It’s really a “short money” position. In other words, it eventually has to be covered by paying the debt back.

To help this process along – i.e., to help debtors relative to creditors – the central bank will put money into the financial system to help make it easier to service the debt (by effectively lowering interest rates). It does so by buying financial assets, mostly government debt securities, which helps increase their prices and decrease their yields.

The central government, from a fiscal point of view, can buy goods, services, and distribute money to people. The central bank, or equivalent monetary authority, is allowed to purchase financial assets.

When financial asset prices go up, people are wealthier on a mark-to-market basis. More valuable assets means more valuable collateral. People can borrow more and they can spend more. They become in better shape financially and this helps the process of better creditworthiness throughout the economy. However, this process of aiding the credit cycle along to a good place doesn’t do much to help spur along the thing that matters most in the long-run, which is productivity.

While knowing where we are in the cycle is important for a trader, insipid productivity trends hold back long-run output expectations. This matters for living standards and long-run asset price returns.