Gold vs. Stocks

Gold is not used in most portfolios, which are typically a stock-bond mix.

Gold nonetheless has value because of its unique properties as a non-financial store of wealth that has a strong track record of offsetting equity and bond declines.

If we ignore other asset classes (most notably bonds), how would we optimize a gold and stocks portfolio?

Key Takeaways – Gold vs. Stocks

- Stocks are productive assets that generate earnings and thus are a staple for compounding wealth.

- Gold is inert and a type of monetary asset that preserves value rather than creating it.

- Gold tracks money growth over the long run and protects purchasing power when currencies weaken or when inflation rises (imperfectly).

- Bonds normally serve as the defensive anchor, but in certain environments (e.g., higher inflation, geopolitical conflict, poor currency performance, real rate declines), gold can diversify better, plus it carries no counterparty risk.

- Stocks deliver strong long-term returns but come with deep drawdowns, long recovery periods when they take large spills, and high sensitivity to economic cycles.

- Gold tends to rise during stress, geopolitical shocks, or periods of currency debasement. This is a different type of stabilizing counterweight to equities.

- Gold has real costs: storage, insurance, ETF fees/roll costs (futures), and the opportunity associated with no yield.

- It’s not about stocks or gold, but their partnership in a portfolio for better risk-adjusted returns.

- Combining stocks and gold smooths volatility and shortens “underwater” periods, turning crashes into manageable corrections.

- A 63% stocks / 37% gold mix historically achieved much better risk-adjusted returns with ~60% of the drawdown depth versus 100% equities, thanks to diversification and the “trim the expensive, buy the cheaper” benefit of systematic rebalancing. Rebalancing between two uncorrelated assets forces “buy low, sell high,” which creates a mathematical compounding advantage.

- A stock-gold portfolio strengthens the sustainability versus one or the other by reducing drawdowns and raising safe-withdrawal potential.

Top Brokers With Stocks and Gold

Our hands-on tests point to these providers being strong choices if you want to trade stocks and gold from the same platform:

Gold vs. Stocks: The Fundamental Difference

With stocks and gold you have a choice between productive equity and inert commodities.

Stocks represent ownership in companies and their profits/cash flow over time. When you hold a share of a company, you possess a claim on future earnings, innovation, and growth.

These are productive assets that generate cash flow through dividends and reinvestment. Stocks are the engine of wealth creation, relying on the success of the underlying business to compound value over time.

Gold, conversely, is a static asset. It produces no cash flow, yields no interest, and creates nothing. It’s a non-financial store of value that relies entirely on scarcity and demand to maintain its worth.

As an investment, gold isn’t a bet on economic growth, but a bet on the preservation of purchasing power.

It doesn’t “do” anything; it simply is. Its value is simply a reflection of the world around it.

Over the long run (but not the short run) gold’s value mirrors money growth relative to the global gold stock.

The Traditional View vs. The Reality

Conventionally, investors rarely choose between stocks and gold directly.

Instead, the standard portfolio pairs risky stocks with the more staid bonds.

Bonds have historically served as the “safety anchor” because they offer a contractual yield and usually have lower volatility than equities because of their fixed duration.

In a typical 60/40 portfolio, bonds are the counterweight intended to smooth out the ride when the stock market stumbles – though stocks still dominate 85-90% of the movement because of their longer duration.

But the reality of modern markets challenges this traditional view. In environments where interest rates are low or inflation is high, bonds may fail to provide real returns or adequate protection against equity falls.

This is where the argument for replacing or supplementing bonds with gold or something physical (i.e., commodities) gains traction.

While bonds rely on the solvency of a government or corporation, gold carries no counterparty risk. It’s a financial asset that’s not simultaneously someone else’s liability. Introducing gold into the “safety” portion of a portfolio, a trader can help not have their entire portfolio tied to the financial system.

Gold acts as a shock absorber, often rising during periods of fear or currency debasement when both stocks and bonds might fall together.

In this context, gold isn’t a competitor to stocks, but a partner that can also be a quality asset for helping offset equity risk.

The Case for Equities

Stocks generally serve as the primary engine for portfolio growth because they represent ownership in productive, profitable enterprises.

Historically, the asset class has had stronger-than-expected returns; the S&P 500 has delivered a CAGR of approximately 10.9% since 1972.

Prudent forward-looking estimates suggest future returns may be lower due to current valuations and practical future productivity growth rates. But stocks remain the most effective vehicle for capturing economic growth over the long haul.

Most of the value generated gets capitalized in the share prices of most stocks. But a key component of this total return comes from dividends. When these cash payouts are reinvested rather than spent, they purchase additional shares (typically called a DRIP plan), which in turn generate more dividends.

This compounding loop helps turn linear savings into exponential wealth accumulation over decades.

The Risk Profile

This high return potential, however, is the premium paid for accepting more risk in the form of larger nominal price changes.

Stocks are notoriously volatile in the short term due to transactive activity that largely reacts to changes in discounted growth, discounted inflation, interest rates, risk premiums, and stock-specific news.

(Related: The 4 Main Variables Impacting Asset Prices)

A portfolio of stocks has traditionally increased in nominal value in around 76% of the years, but can also lose substantial value within a single year.

Equities are inextricably linked to the business cycle.

They’re not easy for informed professionals to time and trade accurately because of the fact that prices don’t move based on “good” or “bad” but how things transpire relative to what’s discounted in.

They’re highly susceptible to economic downturns and earnings recessions. When corporate profits contract, stock prices generally follow suit.

To benefit from this engine, and the fact that most won’t be able to market time (which triggers tax bills and involves transaction costs), the fortitude to hold through these inevitable, and sometimes deep, periods of decline.

The Case for Gold

While stocks/equity serve as the engine of wealth creation, gold functions as a type of diversification asset that can act as a safety net.

It’s widely regarded as the ultimate insurance policy against the various forms of financial/securitized wealth.

Its primary role is to act as a long-term hedge against currency debasement and its value is simply relative to its reference currency.

As central banks expand money supplies and inflation erodes the purchasing power of fiat currency, gold, which can’t be printed, historically maintains its real value. It’s the immutable counterweight to paper money.

Furthermore, gold’s value proposition is magnified during geopolitical crises when trust falls between countries and “black swan” events. It’s a type of asset of last resort.

During periods of volatility, such as the 1970s stagflation or the onset of the 2020 pandemic (it fell approximately 11%), gold can better hold its ground or even increase when traditional assets fall.

This non-correlated performance provides critical stability when fear dominates the market.

The Cost of Carry

Gold, as a physical non-productive asset, has costs associated with it.

First, opportunity cost.

Gold lacks a yield/cash flow. It’s a sterile asset – an ounce of gold remains unchanged. So, in bull markets when equities are rising and interest rates are high enough to make bonds attractive, the opportunity cost of gold puts it out of favor.

Beyond the opportunity cost, there are direct expenses to consider.

For those holding physical bullion, the logistical burden involves fees for secure vaulting and insurance against theft or losses.

Even for modern traders using ETFs or futures to avoid physical hassles, there’s a price to pay in the form of expense ratios with the former and roll costs with an upward-sloping price curve with the latter.

These management fees and roll costs, while often small, are a drag on the value over time.

Therefore, gold should not be viewed as a profit generator, but rather as a cost-incurring form of portfolio insurance that one hopes will appreciate enough over the long run to make it worthwhile – or at the very least serve as a risk-dampening diversifier.

Optimizing a “Stocks + Gold” Portfolio

Bonds are a perfectly viable piece of a portfolio in all their form – government, corporate, foreign-currency, local-currency, nominal yields, inflation-linked yields…

But all asset classes have their strengths and weaknesses and bonds struggle in periods of rising interest rates, when inflation is high (and can lock in a real loss of purchasing power),

A 100% stock portfolio avoids this trap, it exposes the holder to volatility and potentially decade-long recovery periods.

Mixing stocks and gold, we aim to smooth this ride without sacrificing the long-term growth potential of equities.

So basically we have a classic “Efficient Frontier” scenario (the optimal balance of risk and return).

We can first try an 80/20. The idea with 80% stocks and 20% gold is that you can capture the majority of equity upside while reducing the maximum drawdown during market falls. The gold acts as a drag during raging bull markets but can help be somewhat of a parachute during panics.

(With appropriate leveraging, we can keep the 100% stocks and have gold as an overlay, but for purposes of this exercise we’re simply splitting up the pie.)

For those prioritizing preservation over aggressive growth, Harry Browne’s Permanent Portfolio concept shows the viability of even higher gold allocations (i.e., equal to other assets). This idea is that gold exposure can stabilize a portfolio through every economic season (inflation, deflation, and recession).

With two assets, this would simply be 50/50. (The traditional Permanent Portfolio is 25% each to stocks, bonds, cash, and gold.)

But to spare the details, when testing and optimizing for the standard risk-adjusted ratios (Sharpe, Sortino) and drawdowns, we settled on 63% stocks and 37% gold when including just those two assets in the portfolio.

One positive thing with combining assets is the rebalancing. Stocks and gold rarely move in sync. A systematic/rules-defined approach requires selling the asset that has surged (the winner) to buy the asset that has lagged (the loser).

When stocks fall, gold generally acts differently. The disciplined investor sells high-priced gold to buy lower stocks at a discount. Conversely, during a stock boom, they trim expensive equities to replenish their gold allocation.

This mechanical “buy low, sell high” loop creates a mathematical advantage. Rebalancing between two volatile, uncorrelated assets can yield a combined geometric return superior to holding either asset in isolation.

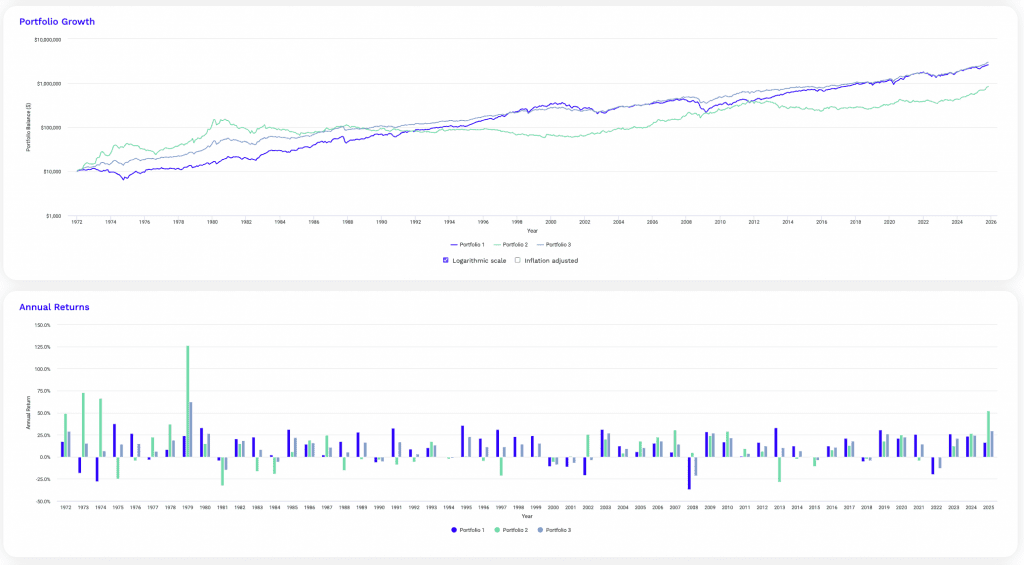

Portfolio Analysis Results

So, we’re going to look at three portfolios:

- stocks

- gold

- stocks-gold mix

Portfolio 1

| Asset Class | Allocation |

|---|---|

| US Stock Market | 100.00% |

Portfolio 2

| Asset Class | Allocation |

|---|---|

| Gold | 100.00% |

Portfolio 3

| Asset Class | Allocation |

|---|---|

| US Stock Market | 63.00% |

| Gold | 37.00% |

Performance Summary

| Metric | Stocks | Gold | Stocks-Gold |

|---|---|---|---|

| Start Balance | $10,000 | $10,000 | $10,000 |

| End Balance | $2,607,436 | $840,654 | $2,976,706 |

| Annualized Return (CAGR) | 10.89% | 8.58% | 11.16% |

| Standard Deviation | 15.64% | 19.59% | 12.46% |

| Best Year | 37.82% | 126.55% | 62.10% |

| Worst Year | -37.04% | -32.60% | -21.51% |

| Maximum Drawdown | -50.89% | -61.78% | -29.09% |

| Sharpe Ratio | 0.46 | 0.29 | 0.56 |

| Sortino Ratio | 0.67 | 0.48 | 0.86 |

So, in this backtest, we compared a 100% US stocks portfolio against both 100% gold and a mix of 63% Stocks and 37% Gold.

The Results: The mixed portfolio did what most do when the assets are return-additive and have real diversification value.

The most critical part was the lower drawdown. The 100% stock investor had to endure a 50.89% crash during the 2008 GFC. The mixed portfolio investor only saw a 29.09% drop.

How is this possible?

This is the value of diversifying (many adverse moves are partially or fully canceled out) “rebalancing bonus” in action.

Because stocks and gold often move in directions that aren’t sensitive to each other, the investor in the mixed portfolio would sell the asset that had just skyrocketed to buy the one that had crashed.

This automatic “buy low, sell high” mechanism captured volatility and turned it into compound growth.

The data proves that by ignoring bonds and finding the right ratio of gold, you can potentially get similar returns with less risk.

Risk and Return Metrics

| Metric | Stocks | Gold | Stocks-Gold |

|---|---|---|---|

| Arithmetic Mean (monthly) | 0.97% | 0.84% | 0.95% |

| Arithmetic Mean (annualized) | 12.25% | 10.60% | 12.02% |

| Geometric Mean (monthly) | 0.86% | 0.69% | 0.89% |

| Geometric Mean (annualized) | 10.89% | 8.58% | 11.16% |

| Standard Deviation (monthly) | 4.52% | 5.66% | 3.60% |

| Standard Deviation (annualized) | 15.64% | 19.59% | 12.46% |

| Downside Deviation (monthly) | 2.92% | 3.17% | 2.14% |

| Maximum Drawdown | -50.89% | -61.78% | -29.09% |

| Benchmark Correlation | 1.00 | 0.02 | 0.79 |

| Beta(*) | 1.00 | 0.03 | 0.63 |

| Alpha (annualized) | 0.00% | 9.76% | 4.10% |

| R2 | 100.00% | 0.06% | 62.41% |

| Sharpe Ratio | 0.46 | 0.29 | 0.56 |

| Sortino Ratio | 0.67 | 0.48 | 0.86 |

| Treynor Ratio (%) | 7.15 | 180.98 | 11.03 |

| Calmar Ratio | 2.37 | 4.75 | 4.17 |

| Modigliani–Modigliani Measure | 11.61% | 8.98% | 13.17% |

| Active Return | 0.00% | -2.31% | 0.27% |

| Tracking Error | 0.00% | 24.76% | 9.59% |

| Information Ratio | N/A | -0.09 | 0.03 |

| Skewness | -0.52 | 0.84 | -0.24 |

| Excess Kurtosis | 1.89 | 4.17 | 2.66 |

| Historical Value-at-Risk (5%) | 7.05% | 6.42% | 4.41% |

| Analytical Value-at-Risk (5%) | 6.46% | 8.46% | 4.96% |

| Conditional Value-at-Risk (5%) | 9.93% | 10.12% | 7.02% |

| Upside Capture Ratio (%) | 100.00 | 20.56 | 70.32 |

| Downside Capture Ratio (%) | 100.00 | -14.81 | 56.19 |

| Safe Withdrawal Rate | 4.29% | 5.59% | 7.19% |

| Perpetual Withdrawal Rate | 6.38% | 4.36% | 6.62% |

| Positive Periods | 405 out of 646 (62.69%) | 336 out of 646 (52.01%) | 408 out of 646 (63.16%) |

| Gain/Loss Ratio | 1.03 | 1.40 | 1.18 |

| * US Stock Market is used as the benchmark for calculations. Value-at-risk metrics are monthly values. | |||

This data table here goes beyond simple growth charts and shows the structural quality of the mixed portfolio.

The most critical takeaway here is efficiency, which can be measured, for example, by the Sharpe Ratio and Sortino Ratio.

The stocks-gold mix achieves a Sharpe Ratio of 0.56, decisively beating the 100% stocks portfolio’s 0.46.

In basic terms, for every “unit” of risk you endured, the mixed portfolio paid you more money. This is confirmed by the volatility, which dropped from 15.64% in stocks to a calmer 12.46% in the mix.

We can also look at the Safe Withdrawal Rate (SWR) estimate. This metric estimates how much money you can pull out annually in retirement without going broke.

- 100% Stocks – Offers a standard 4.29% SWR.

- Stocks-Gold Mix – Jumps to 7.19%.

Because the mixed portfolio avoids deep crashes (as seen in the Max Drawdown of -29% vs -50%), it better preserves capital.

This allows a retiree to potentially spend more than the annual income compared to the all-stock investor, with less risk of ruin.

Also, we can look at the Capture Ratios. The mix captures 70% of the stock market’s upside but only 56% of its downside. The better than 1:1 ratio is common with better diversified portfolios.

This asymmetric return profile, participating in the rallies while partially sitting out the crashes, is key to long-term wealth preservation.

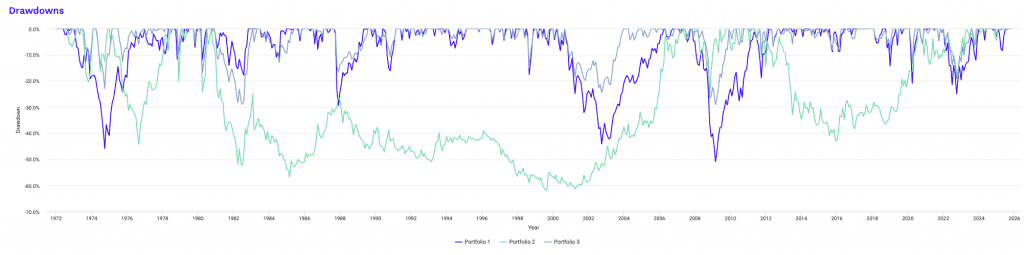

Below we can see the drawdowns of each portfolio.

Note gold’s long underwater period between 1981 to the 2000s. This shows to not overemphasize an asset just because it’s hot.

Historical Market Stress Periods

| Stress Period | Start | End | Stocks | Gold | Mix |

|---|---|---|---|---|---|

| Oil Crisis | Oct 1973 | Mar 1974 | -12.61% | -2.00% | -5.60% |

| Black Monday Period | Sep 1987 | Nov 1987 | -29.34% | 0.00% | -16.58% |

| Asian Crisis | Jul 1997 | Jan 1998 | -3.72% | -13.26% | -4.22% |

| Russian Debt Default | Jul 1998 | Oct 1998 | -17.57% | -7.73% | -14.21% |

| Dotcom Crash | Mar 2000 | Oct 2002 | -44.11% | -12.24% | -24.52% |

| Subprime Crisis | Nov 2007 | Mar 2009 | -50.89% | -25.83% | -29.09% |

| COVID-19 Start | Jan 2020 | Mar 2020 | -20.89% | -0.86% | -13.23% |

The true test of any portfolio isn’t how much it makes during a bull market, but how it does during market falls.

This table highlights the “Stress Periods” over the testing period, notably 2008, 2020, and 2000, but many others outside of that, too.

The data confirms that the stocks-gold mix acts as a quality shock absorber.

Look specifically at the two major “wealth destroyers” of the last 30 years: the Dotcom Crash and the Subprime Crisis of 2008.

During the Dotcom bust (2000-2002), a pure stock investor saw nearly half their wealth vanish in a standard S&P 500 fund (-44.11%), and of course would have lost around 80% if they were in the NASDAQ.

The mixed portfolio investor, however, was shielded, suffering a far more manageable -24.52% drop.

The story repeats in 2008: while the stock market was cut in half (-50.89%), the mix limited the damage to -29.09%.

It is important to notice that gold didn’t always skyrocket during these crises. In the Subprime Crisis, gold actually fell by 25%.

However, because it fell less than stocks and often moved on a different timeline, the combined effect was preservation. Even during the sudden shock of the COVID-19 onset, the mix outperformed stocks by over 7%.

The mix transforms a large hole into a survivable correction.

Let’s look at various drawdowns:

Drawdowns for Portfolio 1

| Rank | Start | End | Length | Recovery By | Recovery Time | Underwater Period | Drawdown |

|---|---|---|---|---|---|---|---|

| 1 | Nov 2007 | Feb 2009 | 1 year 4 months | Mar 2012 | 3 years 1 month | 4 years 5 months | -50.89% |

| 2 | Jan 1973 | Sep 1974 | 1 year 9 months | Dec 1976 | 2 years 3 months | 4 years | -45.86% |

| 3 | Sep 2000 | Sep 2002 | 2 years 1 month | Apr 2006 | 3 years 7 months | 5 years 8 months | -44.11% |

| 4 | Sep 1987 | Nov 1987 | 3 months | May 1989 | 1 year 6 months | 1 year 9 months | -29.34% |

| 5 | Jan 2022 | Sep 2022 | 9 months | Dec 2023 | 1 year 3 months | 2 years | -24.94% |

| 6 | Jan 2020 | Mar 2020 | 3 months | Jul 2020 | 4 months | 7 months | -20.89% |

| 7 | Dec 1980 | Jul 1982 | 1 year 8 months | Oct 1982 | 3 months | 1 year 11 months | -17.85% |

| 8 | Jul 1998 | Aug 1998 | 2 months | Nov 1998 | 3 months | 5 months | -17.57% |

| 9 | Jun 1990 | Oct 1990 | 5 months | Feb 1991 | 4 months | 9 months | -16.20% |

| 10 | Oct 2018 | Dec 2018 | 3 months | Apr 2019 | 4 months | 7 months | -14.28% |

| Worst 10 drawdowns included above | |||||||

Drawdowns for Portfolio 2

| Rank | Start | End | Length | Recovery By | Recovery Time | Underwater Period | Drawdown |

|---|---|---|---|---|---|---|---|

| 1 | Oct 1980 | Aug 1999 | 18 years 11 months | Apr 2007 | 7 years 8 months | 26 years 7 months | -61.78% |

| 2 | Jan 1975 | Aug 1976 | 1 year 8 months | Jul 1978 | 1 year 11 months | 3 years 7 months | -44.24% |

| 3 | Sep 2011 | Dec 2015 | 4 years 4 months | Jul 2020 | 4 years 7 months | 8 years 11 months | -42.91% |

| 4 | Mar 2008 | Oct 2008 | 8 months | May 2009 | 7 months | 1 year 3 months | -25.83% |

| 5 | Feb 1980 | Mar 1980 | 2 months | Jun 1980 | 3 months | 5 months | -24.27% |

| 6 | Jul 1973 | Oct 1973 | 4 months | Jan 1974 | 3 months | 7 months | -20.49% |

| 7 | Nov 1978 | Nov 1978 | 1 month | Feb 1979 | 3 months | 4 months | -20.28% |

| 8 | Aug 2020 | Oct 2022 | 2 years 3 months | Nov 2023 | 1 year 1 month | 3 years 4 months | -18.08% |

| 9 | Apr 1974 | Jun 1974 | 3 months | Nov 1974 | 5 months | 8 months | -16.62% |

| 10 | Dec 2009 | Jan 2010 | 2 months | May 2010 | 4 months | 6 months | -8.37% |

| Worst 10 drawdowns included above | |||||||

Drawdowns for Portfolio 3

| Rank | Start | End | Length | Recovery By | Recovery Time | Underwater Period | Drawdown |

|---|---|---|---|---|---|---|---|

| 1 | Nov 2007 | Feb 2009 | 1 year 4 months | Mar 2010 | 1 year 1 month | 2 years 5 months | -29.09% |

| 2 | Dec 1980 | Jun 1982 | 1 year 7 months | Jan 1983 | 7 months | 2 years 2 months | -29.00% |

| 3 | Sep 2000 | Sep 2002 | 2 years 1 month | Dec 2003 | 1 year 3 months | 3 years 4 months | -24.52% |

| 4 | Apr 1974 | Sep 1974 | 6 months | Feb 1975 | 5 months | 11 months | -22.99% |

| 5 | Jan 2022 | Sep 2022 | 9 months | Jul 2023 | 10 months | 1 year 7 months | -19.24% |

| 6 | Feb 1980 | Mar 1980 | 2 months | Jun 1980 | 3 months | 5 months | -16.96% |

| 7 | Sep 1987 | Nov 1987 | 3 months | Jul 1989 | 1 year 8 months | 1 year 11 months | -16.58% |

| 8 | May 1998 | Aug 1998 | 4 months | Dec 1998 | 4 months | 8 months | -15.21% |

| 9 | Feb 2020 | Mar 2020 | 2 months | May 2020 | 2 months | 4 months | -13.23% |

| 10 | Jul 1983 | Jul 1984 | 1 year 1 month | May 1985 | 10 months | 1 year 11 months | -13.00% |

| Worst 10 drawdowns included above | |||||||

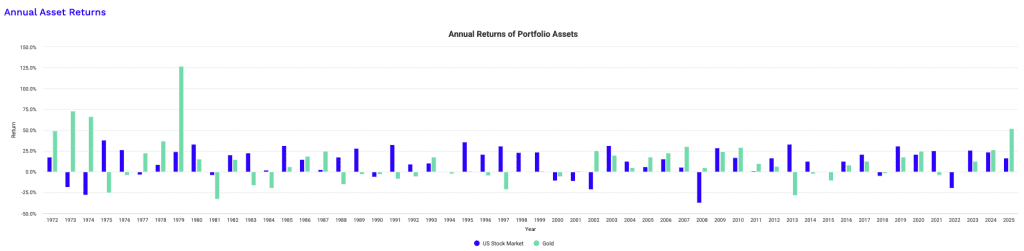

This chart shows that stocks and gold dance to different rhythms. The most striking example of this inverse relationship occurred during the stagflation of 1973 and 1974.

The stock market (blue) suffered consecutive years of deep losses, but gold (green) skyrocketed, delivering massive gains that completely offset the equity drop.

A similar protective pattern emerged during the 2008 financial crisis; when stocks fell, gold finished the year positive, acting as a quality shock absorber.

There are years like 2013 where the relationship flipped: stocks rallied hard while gold suffered a sharp decline (bonds did poorly that year, too).

However, “uncorrelated” doesn’t always mean “inverse” or separate. It’s just an average expectation.

There are rare, painful years where both assets lose value simultaneously, such as in 1981 and 2022. This is typically when monetary policy is overly tight and cash outperforms everything.

This shows that gold isn’t a magic shield that works every single year.

Nonetheless, its long-term tendency to zig when stocks zag is precisely what reduces overall portfolio volatility over time.

Having other assets to improve things further has a lot of value.

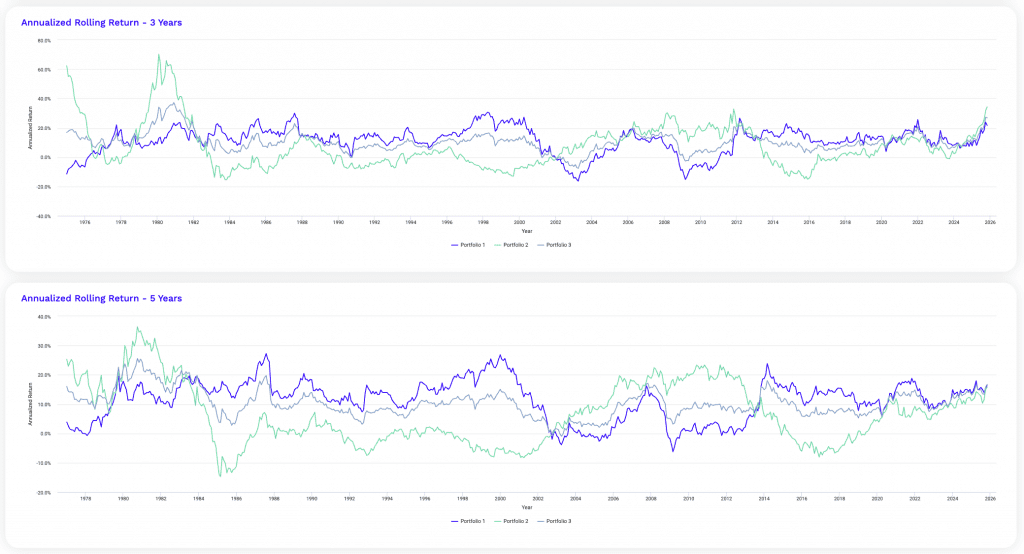

Rolling Returns

| Roll Period | Stocks | Gold | Stocks-Gold | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Average | High | Low | Average | High | Low | Average | High | Low | |

| 1 year | 12.08% | 66.73% | -43.18% | 10.39% | 179.42% | -37.71% | 11.55% | 77.56% | -28.65% |

| 3 years | 11.30% | 30.70% | -16.27% | 7.34% | 70.26% | -15.32% | 10.49% | 37.25% | -7.63% |

| 5 years | 11.41% | 27.25% | -6.23% | 6.56% | 36.39% | -14.69% | 10.34% | 25.56% | -0.94% |

| 7 years | 11.36% | 21.23% | -3.02% | 6.23% | 38.74% | -6.75% | 10.20% | 22.16% | 3.22% |

| 10 years | 11.30% | 18.89% | -2.57% | 5.29% | 24.75% | -5.99% | 9.82% | 17.10% | 3.55% |

| 15 years | 11.06% | 18.21% | 4.25% | 5.07% | 15.89% | -3.63% | 9.61% | 15.41% | 5.17% |

While annual returns show us what happened in a specific calendar year, Rolling Returns can help answer questions like: “What if I buy at the absolute worst time?”

This can strip away the luck of the draw. It looks at every possible holding period (every 1-year window, every 5-year window, etc.) to reveal the relative consistency of the strategy.

I also think the asset management industry can be overly focused on annual horizons simply because that’s how a lot of things are organized for convenience and frame of reference.

In reality, in many long-term and short-term strategies the annual can be relatively noisy.

Here, the data shows that diversification is a great cure for “underwater periods,” the agonizing times when your account balance sits below your initial investment or your high-water mark.

Escaping the “Lost Decade”

The most unfortunate data point for the 100% stocks investor is in the 10-Year row. The “Low” column shows -2.57%. This means there was a ten-year period where a pure stocks investor waited a full decade only to end up with less money than they started with. That’s not great.

(And if you were a Japanese investor and you went through the 1989-90 bubble, it was even worse.)

Now, look at the Stocks-Gold Mix for the same 7-year and 10-year periods. The “Low” is positive.

- 7 Years: Stocks could be down -3.02%. The Mix is up +3.22%.

- 10 Years: Stocks could be down -2.57%. The Mix is up +3.55%.

The addition of gold effectively eliminates these low points at these horizons over the sample.

By the 7-year mark, the mixed portfolio has historically shown a profit, whereas the stock investor is still waiting on a recovery.

Smoothing the Ride

In the shorter term (1 to 5 years), the protection is equally vital.

In the worst 1-year period, stocks crashed -43.18%. The mix cushioned that fall to -28.65%. By year 5, the mixed portfolio has almost zero downside risk (-0.94% low), while stocks can still be down significantly (-6.23%).

While the “Average” returns for the mix are slightly lower than pure stocks (e.g., 9.82% vs 11.30% over 10 years), the trade-off is clear.

The mix creates a rising floor for your wealth, ensuring that even if you have the worst timing in history, you avoid the terrible long-term underwater periods that hurts retirement plans.

Is Warren Buffett Wrong About Gold?

Warren Buffett famously does not like gold.

He once quipped that gold “gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.”

Is he right?

Let’s look at the claim.

1. The “No Utility” Claim Is Narrowly Framed

The quote from Warren Buffett treats “utility” as productive cash flow. That definition is too restrictive.

Gold’s utility is monetary and balance-sheet based:

- It is a non-liability asset. In other words, it lacks counterparty risk.

- It functions as collateral in global funding markets.

- It is held by central banks as a reserve diversification asset.

- It acts as a hedge against currency debasement and sovereign risk.

Calling it useless because it doesn’t produce income ignores its role as monetary insurance.

Cash in a vault also produces no income. Yet liquidity has value.

2. The 100-Year Comparison Is a Straw Construction

Buffett made a comparison in his 2011 shareholder letter.

He wrote that all the gold in the world at the time, about 170,000 metric tons, could form a 68-foot-per-side cube then worth $9.6 trillion.

For that much money, one could have bought all US cropland and 16 Exxon Mobils with $1 trillion in change. “No sense feeling strapped after this buying binge.”

He then pointed out how unlikely it was that all those assets, plus their income, would be worth less than the gold 100 years in the future.

But this comparison (gold cube vs. farmland + Exxon) has multiple structural issues:

It Assumes Stable Political and Monetary Regimes

The farmland + Exxon Mobil comparison assumes:

- Stable property rights

- Functional capital markets

- No confiscation

- No severe currency collapse

Gold’s value proposition is heavily about tail risk. Comparing it only under stable long-run conditions biases the conclusion.

It Assumes Continuous Compounding Is Guaranteed

Productive assets compound if:

- Earnings remain durable

- Valuations don’t compress

- Taxes and regulation remain manageable

History shows:

- Empires fall

- Capital gets destroyed

- Entire stock markets disappear

Gold’s long-run stagnation periods are real. But so are long periods where equity markets permanently impaired capital.

3. Cherry-Picked Time Frames

The piece notes gold’s 45-year inflation-adjusted drawdown (1980–2025).

That starting point is key.

1980 was:

- A peak in inflation panic

- A peak in gold speculation following the inflationary 1970s and low real yields

- Right before a period of double-digit real rates with the Volcker hike

Starting at a mania peak makes practically any asset look bad.

Likewise, starting equity returns at 1980 benefits from:

- Disinflation

- Falling interest rates

- Massive valuation expansion

- Globalization tailwinds

Both gold bulls and gold bears cherry-pick periods.

The article critiques gold for timing sensitivity while implicitly benefiting from stock timing.

4. Gold Is Framed as Competing With Stocks

This is a category error.

Gold isn’t primarily a growth asset.

We’ve mentioned elsewhere that over the long-run gold itself isn’t much better than cash and you can expect 1-2% real (inflation-adjusted) returns over time.

It’s:

- A volatility dampener

- A currency hedge

- A real rate hedge

- A geopolitical hedge

Evaluating it purely against US equities ignores its diversification function.

The relevant question isn’t:

“Does gold beat stocks?”

It’s:

“Does gold improve portfolio risk-adjusted returns under certain conditions and over a long enonugh timeframe?”

Empirical evidence shows that in:

- High inflation periods

- Negative real rate periods

- Dollar weakness cycles…

…Gold often outperforms.

5. Sequence of Return Risk Argument Is Misapplied

Some argue gold increases sequence risk.

That depends entirely on allocation size.

- A 100% gold portfolio is reckless.

- A 5-15% allocation behaves differently.

Gold’s long flat periods are precisely why it can zig when equities zag.

Its low correlation in stress regimes is a central feature.

Sequence risk is a function of:

- Withdrawal rate

- Asset mix

- Correlation structure

Not just whether an asset compounds.

6. Ignores the Monetary Regime Shift Question

Buffett’s critique assumes:

- Fiat currency dominance remains intact

- US fiscal sustainability holds – if we’re talking USD traders (gold’s performance is relative to the reference currency)

- Dollar hegemony persists

Those may be correct assumptions.

But gold is a hedge against those assumptions being wrong.

Since 2008:

- Global debt-to-GDP has ballooned upward

- Central banks have monetized aggressively

- Real yields have periodically turned negative

Gold’s strong performance reflects monetary stress more than speculation.

7. “It Doesn’t Compound” Is True but Incomplete

Gold doesn’t compound. But it can reprice.

There’s a difference between:

- Growth via earnings

- Revaluation due to monetary debasement

If fiat supply grows faster than real output, gold’s nominal price adjusts upward without producing income.

Over the long run, gold’s value tends to track the amount of money in circulation relative to the global gold stock.

More preservation and defense than growth.

8. The Comparison Is US-Centric

US stocks crushed gold over long horizons.

But consider:

- Weimar Germany

- Argentina

- Turkey

- Russia

- Other instances of collapse as we list out here

In many currency collapses, gold preserved purchasing power when domestic equities and bonds were destroyed.

The argument assumes a stable Western financial system.

Gold’s role is most visible where systems fail.

9. Opportunity Cost Depends on Real Rates

Gold struggles when:

- Real interest rates are high

- Dollar/reference currency is strong

- Risk appetite is high

Gold thrives when:

- Real rates are negative

- Monetary policy is repressive

- Fiscal sustainability is questioned or a real threat

- There’s geopolitical friction and trust between countries is naturally lower

The 1980-2000 period was uniquely hostile to gold.

The 2000-2011 period was uniquely supportive.

Bottom Line

The anti-gold argument is correct in one narrow sense:

Over very long periods in stable capitalist systems, productive assets outperform inert ones.

But it’s flawed in broader asset allocation terms because it:

- Frames gold as a growth asset competitor

- Assumes regime stability

- Ignores tail risk hedging

- Dismisses monetary insurance value

- Ignores trade structuring – as an overlay such that it doesn’t take aware from core assets in a portfolio, which is our personal preference

Gold is a balance-sheet hedge against extreme outcomes.

If you believe:

- US fiscal dominance continues

- Real rates remain structurally positive

- Capitalism compounds uninterrupted

Then Buffett is likely right.

If you assign non-trivial probability to monetary instability, sovereign stress, or regime change, gold serves a different purpose entirely.

The real debate isn’t “gold vs. stocks.”

That’s like asking whether a seatbelt is worse than an engine because the engine moves the car faster.

They serve different purposes, and structuring gold as an overlay means you can still get its benefit without taking away from other assets.

Conclusion

The comparison between stocks and gold isn’t about picking a winner, but about engineering a relationship by blending them well to achieve return goals in a safer way.

Stocks provide the productive engine of growth, driven by corporate profits and productivity growth over time.

Gold serves as the anchor, a non-financial store of value that preserves purchasing power over long time horizons.

The data from our 63% Stocks / 37% Gold backtest shows a superior risk-adjusted return – Sharpe Ratio (0.56 vs. 0.46) compared to a pure stock portfolio.

This mix also helps with underwater periods. During the “lost decade” of the 2000s, where stock investors waited years to break even because of two bad drawdowns, the mixed portfolio remained positive.

It transformed the catastrophic 50% drawdown of 2008 into a survivable 29% correction.

Because these assets rarely move in sync and keeping an allocation within specific bands, the disciplined trader is mathematically forced to “buy low and sell high.”

Ultimately, the evidence suggests that a portfolio of stocks and gold offers a quality path to wealth preservation without sacrificing long-term growth.

It doesn’t have to be one or the other, but both.

Appendix

Annual Returns

| Year | Inflation | Stocks | Gold | Stocks-Gold Mix | US Stock Market | Gold | |||

|---|---|---|---|---|---|---|---|---|---|

| Return | Balance | Return | Balance | Return | Balance | ||||

| 2025 | 2.91% | 16.73% | $2,607,436 | 52.03% | $840,654 | 29.79% | $2,976,706 | 16.73% | 52.03% |

| 2024 | 2.89% | 23.61% | $2,233,767 | 26.66% | $552,938 | 24.74% | $2,293,454 | 23.61% | 26.66% |

| 2023 | 3.35% | 25.87% | $1,807,151 | 12.69% | $436,564 | 21.00% | $1,838,654 | 25.87% | 12.69% |

| 2022 | 6.45% | -19.60% | $1,435,676 | -0.77% | $387,397 | -12.64% | $1,519,588 | -19.60% | -0.77% |

| 2021 | 7.04% | 25.59% | $1,785,724 | -4.15% | $390,411 | 14.59% | $1,739,361 | 25.59% | -4.15% |

| 2020 | 1.36% | 20.87% | $1,421,889 | 24.81% | $407,310 | 22.33% | $1,517,960 | 20.87% | 24.81% |

| 2019 | 2.29% | 30.65% | $1,176,380 | 17.86% | $326,332 | 25.92% | $1,240,879 | 30.65% | 17.86% |

| 2018 | 1.91% | -5.26% | $900,414 | -1.94% | $276,892 | -4.03% | $985,487 | -5.26% | -1.94% |

| 2017 | 2.11% | 21.05% | $950,367 | 12.81% | $282,372 | 18.00% | $1,026,865 | 21.05% | 12.81% |

| 2016 | 2.07% | 12.53% | $785,093 | 8.03% | $250,310 | 10.87% | $870,211 | 12.53% | 8.03% |

| 2015 | 0.73% | 0.29% | $697,654 | -10.67% | $231,698 | -3.76% | $784,907 | 0.29% | -10.67% |

| 2014 | 0.76% | 12.43% | $695,625 | -2.19% | $259,376 | 7.02% | $815,611 | 12.43% | -2.19% |

| 2013 | 1.50% | 33.35% | $618,722 | -28.33% | $265,176 | 10.53% | $762,102 | 33.35% | -28.33% |

| 2012 | 1.74% | 16.25% | $463,985 | 6.60% | $369,995 | 12.68% | $689,509 | 16.25% | 6.60% |

| 2011 | 2.96% | 0.96% | $399,116 | 9.57% | $347,089 | 4.15% | $611,911 | 0.96% | 9.57% |

| 2010 | 1.50% | 17.09% | $395,313 | 29.27% | $316,785 | 21.60% | $587,554 | 17.09% | 29.27% |

| 2009 | 2.72% | 28.70% | $337,604 | 24.03% | $245,056 | 26.97% | $483,189 | 28.70% | 24.03% |

| 2008 | 0.09% | -37.04% | $262,323 | 4.92% | $197,580 | -21.51% | $380,552 | -37.04% | 4.92% |

| 2007 | 4.08% | 5.49% | $416,635 | 30.45% | $188,308 | 14.73% | $484,854 | 5.49% | 30.45% |

| 2006 | 2.54% | 15.51% | $394,954 | 22.55% | $144,348 | 18.11% | $422,618 | 15.51% | 22.55% |

| 2005 | 3.42% | 5.98% | $341,918 | 17.76% | $117,789 | 10.34% | $357,803 | 5.98% | 17.76% |

| 2004 | 3.26% | 12.52% | $322,624 | 4.65% | $100,023 | 9.60% | $324,274 | 12.52% | 4.65% |

| 2003 | 1.88% | 31.35% | $286,736 | 19.89% | $95,580 | 27.11% | $295,857 | 31.35% | 19.89% |

| 2002 | 2.38% | -20.96% | $218,293 | 25.57% | $79,724 | -3.74% | $232,754 | -20.96% | 25.57% |

| 2001 | 1.55% | -10.97% | $276,183 | 0.75% | $63,490 | -6.63% | $241,809 | -10.97% | 0.75% |

| 2000 | 3.39% | -10.57% | $310,199 | -5.44% | $63,020 | -8.68% | $258,985 | -10.57% | -5.44% |

| 1999 | 2.68% | 23.81% | $346,880 | 0.85% | $66,648 | 15.32% | $283,589 | 23.81% | 0.85% |

| 1998 | 1.61% | 23.26% | $280,165 | -0.83% | $66,085 | 14.35% | $245,921 | 23.26% | -0.83% |

| 1997 | 1.70% | 30.99% | $227,288 | -21.41% | $66,636 | 11.61% | $215,059 | 30.99% | -21.41% |

| 1996 | 3.32% | 20.96% | $173,510 | -4.59% | $84,788 | 11.51% | $192,696 | 20.96% | -4.59% |

| 1995 | 2.54% | 35.79% | $143,441 | 0.98% | $88,863 | 22.91% | $172,807 | 35.79% | 0.98% |

| 1994 | 2.67% | -0.17% | $105,638 | -2.17% | $88,002 | -0.91% | $140,600 | -0.17% | -2.17% |

| 1993 | 2.75% | 10.62% | $105,817 | 17.68% | $89,954 | 13.23% | $141,890 | 10.62% | 17.68% |

| 1992 | 2.90% | 9.11% | $95,654 | -5.73% | $76,441 | 3.62% | $125,307 | 9.11% | -5.73% |

| 1991 | 3.06% | 32.39% | $87,670 | -8.56% | $81,091 | 17.24% | $120,934 | 32.39% | -8.56% |

| 1990 | 6.11% | -6.08% | $66,220 | -3.11% | $88,680 | -4.98% | $103,150 | -6.08% | -3.11% |

| 1989 | 4.65% | 28.12% | $70,505 | -2.84% | $91,527 | 16.66% | $108,557 | 28.12% | -2.84% |

| 1988 | 4.42% | 17.32% | $55,031 | -15.26% | $94,202 | 5.27% | $93,050 | 17.32% | -15.26% |

| 1987 | 4.43% | 2.61% | $46,908 | 24.53% | $111,160 | 10.72% | $88,396 | 2.61% | 24.53% |

| 1986 | 1.10% | 14.57% | $45,713 | 18.96% | $89,265 | 16.20% | $79,836 | 14.57% | 18.96% |

| 1985 | 3.80% | 31.27% | $39,898 | 6.00% | $75,040 | 21.92% | $68,708 | 31.27% | 6.00% |

| 1984 | 3.95% | 2.19% | $30,394 | -19.38% | $70,792 | -5.79% | $56,354 | 2.19% | -19.38% |

| 1983 | 3.79% | 22.66% | $29,743 | -16.31% | $87,807 | 8.24% | $59,820 | 22.66% | -16.31% |

| 1982 | 3.83% | 20.50% | $24,249 | 14.94% | $104,914 | 18.44% | $55,264 | 20.50% | 14.94% |

| 1981 | 8.92% | -4.15% | $20,124 | -32.60% | $91,274 | -14.68% | $46,660 | -4.15% | -32.60% |

| 1980 | 12.52% | 33.15% | $20,995 | 15.19% | $135,419 | 26.51% | $54,685 | 33.15% | 15.19% |

| 1979 | 13.29% | 24.25% | $15,768 | 126.55% | $117,566 | 62.10% | $43,228 | 24.25% | 126.55% |

| 1978 | 9.02% | 8.45% | $12,691 | 37.01% | $51,894 | 19.02% | $26,667 | 8.45% | 37.01% |

| 1977 | 6.70% | -3.36% | $11,701 | 22.64% | $37,876 | 6.26% | $22,406 | -3.36% | 22.64% |

| 1976 | 4.86% | 26.47% | $12,108 | -4.10% | $30,884 | 15.16% | $21,086 | 26.47% | -4.10% |

| 1975 | 6.94% | 37.82% | $9,574 | -24.80% | $32,204 | 14.65% | $18,310 | 37.82% | -24.80% |

| 1974 | 12.34% | -27.81% | $6,947 | 66.15% | $42,824 | 6.95% | $15,970 | -27.81% | 66.15% |

| 1973 | 8.71% | -18.18% | $9,623 | 72.96% | $25,775 | 15.54% | $14,932 | -18.18% | 72.96% |

| 1972 | 3.41% | 17.62% | $11,762 | 49.02% | $14,902 | 29.24% | $12,924 | 17.62% | 49.02% |

| Annual return for 2025 is from 01/01/2025 to 10/31/2025 | |||||||||