Anti-Growth Assets (List of Stores of Value)

There are several assets that can be considered stores of value that hold their value over time and are less dependent on infusions of liquidity and good economic conditions.

Including some level of “anti-growth” assets in a portfolio can help to reduce risk and provide a store of value for a more balanced portfolio or during times when growth and/or inflation or overall economic conditions are unfavorable.

These assets, also known as defensive assets, tend to perform well when growth assets, such as stocks, are performing poorly.

Key Takeaways – Stores of Value & Anti-Growth Assets

- Anti-growth assets provide stability and diversification, and can serve as a store of value during economic downturns or periods of high inflation.

- Examples of anti-growth assets include predictable cash flow equities, private assets, gold and other precious metals, inflation-linked bonds, long-duration government bonds, real estate, infrastructure, farmland and timberland, art, rare collectibles, potentially some cryptocurrencies, commodity currencies, reserve currencies, and less growth-sensitive commodities.

- The specific allocation of anti-growth assets will depend on an investor’s risk tolerance, investment goals, and market conditions, as well as where we are in the long-term debt cycle.

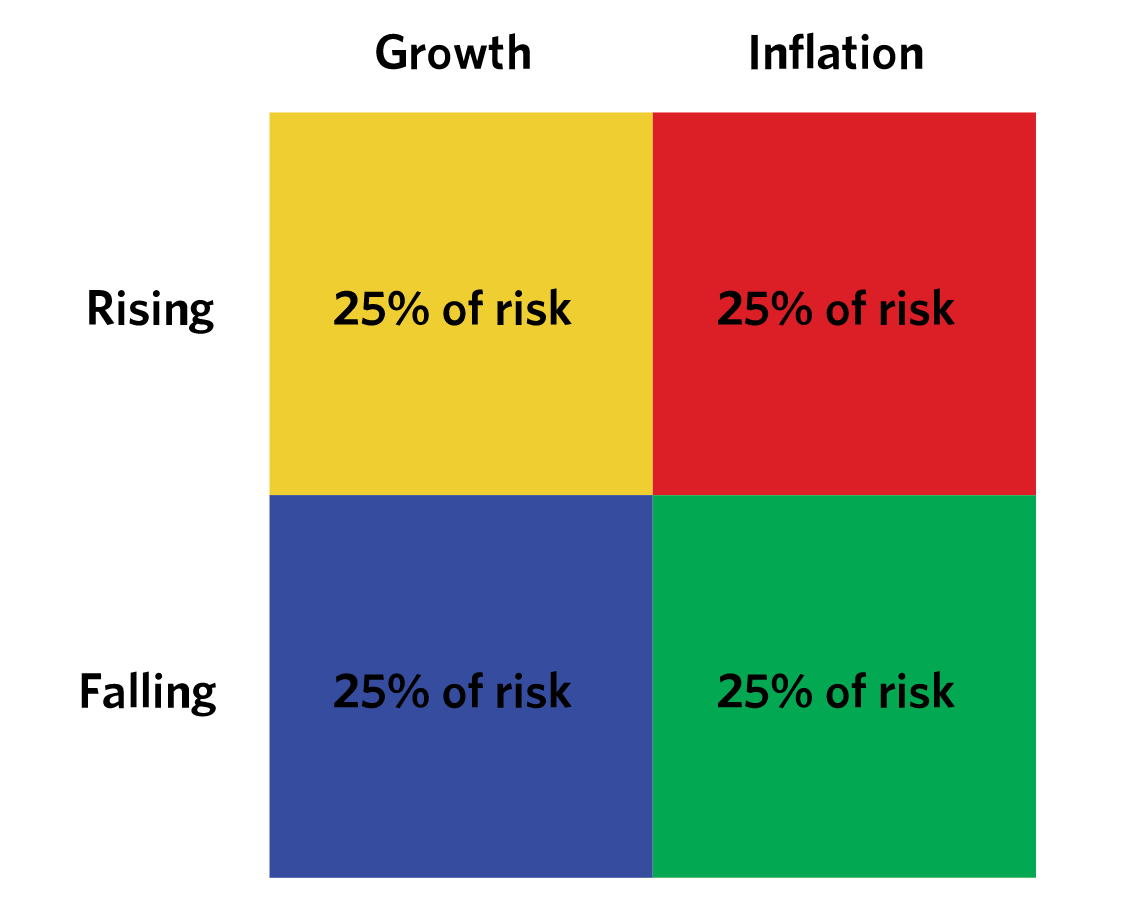

The Four Economic Environments – Why Diversification Across Stores of Value Matters

Asset prices are driven, in the simplest possible terms, by two big forces: growth and inflation.

Each can come in faster or slower than what’s discounted into prices. That gives you four economic environments: growth rising, growth falling, inflation rising, inflation falling.

Most portfolios are concentrated in assets that do well only in the first environment. Stocks make up the bulk of household wealth, and stocks are essentially long growth rising.

When growth disappoints or inflation surprises to the upside, the typical portfolio gets hit hard at exactly the moment the investor can least afford it.

The whole point of holding anti-growth assets is to have something that performs well when the dominant assets in the book are getting hurt. As a trader looking for better balance, it’s a good idea to think about owning assets that do well when growth is rising and assets that do well when growth is falling.

That is the foundation of what is sometimes called “balanced beta” thinking, or risk parity in its more institutional form. Balance environmental exposures. Don’t predict which environment will arrive next.

Stores of value aren’t a market call. They are a structural acknowledgment that the future is uncertain.

Benefits of Anti-Growth Assets & Stores of Value

Anti-growth assets help to provide stability and diversification.

Allocating to assets that have a low correlation with the broader stock market (and risk assets, generally) means traders/investors can reduce the overall volatility of their portfolios.

During times of economic recession or market downturns, defensive assets such as government bonds or gold tend to perform well as investors seek safe havens. Growth assets such as stocks generally have large losses during these times.

Anti-growth assets can also provide a hedge against inflation or stagflationary conditions. As inflation rises, the value of growth assets can be eroded, but the value of defensive assets may hold steady or even increase.

Said differently, the goal is to engineer a portfolio that doesn’t depend on any single environment showing up. When you do that well, the result is a smoother return stream, a smaller drawdown profile, and a higher probability of compounding through cycles rather than getting blown out at the bottom.

Anti-Growth Assets List (Stores of Value)

Some of these assets include:

Predictable Cash Flow Equities

Predictable cash flow equities are stocks of companies that generate consistent and reliable cash flows, which allows them to pay stable and growing dividends over time.

Less volatile. They tend to be less volatile than growth or cyclical equities. Predictable cash flow equities typically represent mature, established companies in stable industries with a long track record of consistent earnings. Consumer staples and utility stocks are common examples because they sell things people need to physically live.

Dividends. The dividends provide a steady stream of income that can be reinvested or used to fund expenses. Reliable, growing dividends can also provide a partial hedge against inflation. The key word is partial. When inflation runs hot and central banks are slow to respond, even high-quality dividend payers can lose ground in real terms because their nominal cash flows don’t reset as quickly as prices do.

Supported by their own income streams. Even during periods of economic recession or market volatility, companies that generate consistent cash flows are often able to maintain their dividend payments and avoid significant declines.

There’s a caveat. In a deep credit contraction, even staples and utilities take a hit because the wealth effect operates broadly. As wealth falls first and incomes fall later, creditworthiness worsens, which constricts lending activity, which hurts spending.

People still buy toothpaste, but stock prices reflect more than current cash flows. They reflect the discount rate, the equity risk premium, and the appetite for any risk asset at all. In 2008, even the highest-quality dividend payers fell. Predictable cash flow equities are a defensive tilt, not a true safe haven.

Private Assets

Not traded publicly. Private assets are not traded publicly. This doesn’t mean they’re exempt from the same economic forces as their public counterparts, but it does mean that investors should expect to be compensated for the illiquidity, simply known as an “illiquidity premium.”

Longer-term time horizon. Private assets are often held by individuals or companies with a long-term investment horizon, which means they’re less likely to be influenced by short-term market movements.

Diversification benefits. Private assets can provide diversification benefits, as some may have low correlations with traditional asset classes like stocks and bonds.

Can be skill- or process-driven. Private assets may offer higher potential returns than publicly traded assets, as they often require specialized knowledge or skills. If you want to invest in commercial real estate, that takes a certain skill set to do successfully. It can also mean the asset will consume your time if it depends on your know-how, or you may need to hire out tasks, which creates costs. With private assets, you might be essentially buying yourself a job. It’s important to ensure it’s well-understood what exactly you’re signing up for.

Privacy. Private assets can provide a level of privacy and confidentiality that public assets do not offer.

A word of caution. The “low correlation” of private assets is sometimes partly real and partly an artifact of how they are marked. Private equity, private credit, and private real estate funds are typically valued quarterly by appraisal rather than by daily trading.

That smooths the reported returns and makes the asset look less volatile than it actually is. The underlying economic exposure is often quite similar to public equity or public credit.

Those who treat the smoothness as evidence of true diversification or lack of risk are kidding themselves. The illiquidity premium is real. The volatility reduction is partly a measurement artifact.

Gold

Gold is a classic example of a store of value, as it has been used as a currency for centuries, as something that almost everyone agrees has intrinsic value.

It is a finite resource that is difficult to extract and has limited supply, which helps to maintain its value over time.

Central banks also buy gold as a reserve. In recent years, central bank gold buying has run at the highest pace in modern history, particularly from countries that are wary of holding their reserves in dollars. That is itself an important signal about the international monetary system.

While gold doesn’t explicitly pay a yield and isn’t the best investment over the long run (about the same return as cash or a bit better), it’s no one else’s liability and generally holds its real (after-inflation) value over time.

This last point is the heart of gold’s case as a store of value. Currency and debt serve two purposes: to be a medium of exchange and a storehold of wealth.

When there is a big debt problem that is intolerably painful, central banks will print money and distribute it to make it easier for debtors to pay their debts, which will devalue the money and debt relative to other assets.

Gold’s job in a portfolio is to be the asset that benefits when that happens.

Historically, when currency devaluations have occurred, gold has risen. Gold rose overnight when Roosevelt broke the gold peg in 1933. Gold rose sharply after the August 1971 breakdown of the monetary system, when Nixon delinked the dollar from gold. Gold rose during the 1970s stagflation.

Gold rose after the post-2008 wave of debt monetization. The pattern is consistent: when private market demand for government bonds is inadequate to meet the supply, central banks step in with money printing and buying the bonds, and gold generally benefits as an inverse currency.

There are also storage and insurance costs to consider with physical gold, which also shows up in the shape of its upward-sloping futures curve (contango), which represents these costs, as seen below.

Gold Futures Term Structure

Silver and Other Precious Metals

Silver, platinum, and palladium share some of gold’s properties as stores of value but behave differently in important ways.

Silver is what’s sometimes called a hybrid asset. Roughly half of its annual demand is industrial. The rest is monetary and investment demand. That means silver is more growth-sensitive than gold.

When global manufacturing is strong, silver tends to outperform gold, and the gold-to-silver ratio falls. When growth disappoints, silver tends to underperform. Silver is also a much smaller and less liquid market than gold, which makes it more volatile in both directions.

Platinum and palladium are even more growth-sensitive because most of their demand comes from auto catalysts. They, like other PGMs, are barely stores of value in the gold sense. They are growth-sensitive commodities that happen to be precious metals.

Silver can play a role as a higher-beta version of gold, useful in inflationary environments where industrial demand and monetary demand both strengthen. But it isn’t a substitute for gold. It is a complement at most.

Inflation-Linked Bonds (TIPS and Equivalents)

Inflation-linked government bonds are an underappreciated and underused asset class relative to their potential.

The mechanics are straightforward. The principal of an inflation-linked bond is adjusted based on a measure of inflation (in the US, the CPI). Coupons are paid on the adjusted principal. So as inflation rises, both the principal and the coupon payments rise with it. The investor’s real return is locked in at purchase.

Why does this matter? Because the real bond yield is the most important number to watch in finance. It tells you what real return you can certainly get (free of inflation risk and default risk) on your wealth. It’s the most foundational rate for all capital markets.

When real yields are positive and meaningful, inflation-linked bonds are an excellent defensive holding. They protect against unexpected inflation, provide a real income stream, and are issued by the sovereign, which means default risk is limited (in the home currency, at least).

When real yields are negative, the calculus shifts. A negative real yield means the bond is a guaranteed loss in real terms if held to maturity. That can still be defensive in a portfolio context (because nominal bonds and stocks are likely losing more), but it’s worth being clear-eyed about what you’re buying.

Two policy patterns to watch closely. When central banks engage in large-scale asset purchases, they often suppress real yields directly, which makes inflation-linked bonds less attractive as a forward investment but more valuable as a hedge against further suppression.

And the two things that should not happen, but if they do should be viewed as big red flags, are another round of quantitative easing to force real interest rates down, and the central government gaining control over the central bank.

In either of those scenarios, inflation-linked bonds become critical because they remove the policy maker’s ability to inflate away your purchasing power.

Because the government is both the issuer of inflation-linked bonds and the record-keeper of what inflation is set at, there are some concerns that the metric can be rigged to lower the liability on inflation-linked payouts (among other reasons).

Long-Duration Government Bonds

In a deflationary environment, long-duration government bonds are the single best-performing asset class. When growth falls and inflation falls, central banks cut rates, bond yields decline, and long-duration bonds rise sharply because of their convexity.

This is the deflation hedge. Stocks fall, gold can be mixed (it depends on whether the deflation is being met with money printing), commodities fall, and high-quality long-duration government bonds rally hard.

The case is strongest when starting yields are high, the central bank has gas in the tank (room to cut rates materially), and the sovereign is investment-grade in a credible reserve currency.

The case weakens substantially when starting yields are low, the central bank has very little gas in the tank, and the sovereign’s debt situation is nearing the point of no return. In that scenario, the central bank may be forced to monetize the debt, which makes nominal long bonds the worst asset to hold rather than the best.

Long-duration bonds are the archetypal deflation hedge, but only when policymakers are credible and has room to maneuver.

Real Estate

Real estate is a tangible asset that has historically held its real value and has the potential for long-term appreciation.

While real estate values can fluctuate in the short-term due to market conditions and the fact it’s a debt- and interest rate-sensitive investment, over the long-term, it has been a relatively stable investment.

It’s also important for people to differentiate real estate for living in and real estate for investment.

Real estate for living comes with a stream of expenses that typically isn’t supported by an offsetting income stream from the asset itself. It has to be funded from other income sources, and there are expenses associated with homes that are infrequent and occur over longer cycles, which makes it very easy to chronically underestimate the operating costs.

It typically is not a good store of value because you normally don’t get a nominal rate of return that compensates you for the sum of the inflation rate and the annual net carrying costs expressed as a percentage of the notional market value of the home. It’s also not a very effective inflation hedge over the short-run because of its debt and rate sensitivity that makes it cyclical. That equity is also illiquid until it’s realized, and there are costs associated with that.

Accordingly, primary residences should be a reasonable part of one’s budget.

Real estate for investment purposes is a different story and is a large and diverse asset class. Within it, some segments behave more defensively than others. Multifamily residential and grocery-anchored retail tend to have the most stable cash flows. Office and hotel are heavily growth-sensitive. Industrial has been driven by the secular shift to e-commerce. Specialized property types (data centers, life sciences, medical office, self-storage) each have their own demand dynamics.

The thing investors often miss is that real estate is essentially levered. Most ownership involves a mortgage. That means real estate behaves like a leveraged play on growth and rates. When rates rise, valuations fall and refinancing risk rises.

When the credit contraction produces an economic contraction, vacancy rises, rents soften, and equity gets impaired quickly because the leverage works in both directions. That’s why real estate behaved like a risk asset in 2008-09.

Infrastructure

Infrastructure is increasingly recognized as a distinct asset class with strong defensive characteristics.

Toll roads, regulated utilities, airports, ports, pipelines, electricity transmission, water systems, and renewable power assets generate cash flows that are typically contracted, regulated, or both.

The contracts often have explicit inflation linkage, which makes infrastructure one of the better real-asset inflation hedges in the portfolio.

Three properties make infrastructure attractive as a store of value. Demand for these services is highly inelastic. People drive on toll roads, use water, and consume electricity regardless of the business cycle.

The cash flows are long-dated and contractual, which gives them bond-like predictability. And the regulatory or contractual structures often include inflation adjustments, providing automatic protection in inflationary regimes.

The risks are also clear. Infrastructure assets are typically held with high leverage, which makes them rate-sensitive in the same way real estate is. Regulated utility returns can be cut by regulators in politically charged environments. And privatization of public infrastructure can be reversed politically.

For most retail investors, infrastructure exposure is best obtained through listed infrastructure funds or specialized REITs.

Farmland and Timberland

Farmland and timberland have historically been excellent stores of value, though they are operationally complex and largely available to institutional or high-net-worth investors.

Farmland is finite. Arable land can’t be manufactured. Demand for food grows roughly with population and income, while supply is constrained by available land, water, and soil quality.

Farmland produces an income stream (lease payments or crop revenue) and tends to appreciate in real terms over long periods. It is an inflation hedge because the underlying commodities respond to inflation, and the land itself is a tangible, finite asset.

Timberland has similar properties with one additional feature: the inventory grows whether you harvest it or not. Trees appreciate biologically. In years when timber prices are weak, the owner can simply not harvest and let the inventory build.

The optionality on timing the harvest is a structural advantage few other assets share.

Both have low correlations with traditional financial assets, partly because their returns are driven by biology, weather, and slow-moving demographic forces rather than by daily liquidity flows.

They also have meaningful idiosyncratic risk: drought, disease, fire, regulatory shifts on water rights, and changes in agricultural subsidies.

Related: Teak Wood as a Financial Asset

Art

Art is another tangible asset that can serve as a store of value.

While the value of individual works of art can be highly variable, the overall art market has shown to be relatively stable over time.

What’s considered “art” and how it’s valued varies wildly. The serious investor in art is buying very specific things: works by established artists with documented provenance, ideally works that are already in the auction record.

The retail investor buying contemporary work from a gallery is doing something closer to consumption than investing.

Art has structural characteristics that make it more of a wealth preservation tool than a return generator. It generates no income. It has carrying costs (storage, insurance, conservation). It has high transaction costs at sale (auction fees can run 25% or more on the buyer’s side). And it is highly illiquid.

But it is also no one else’s liability, it is portable in a way real estate is not, and at the high end the buyer base is global, which provides some insulation from any single country’s economic conditions. For very high net worth individuals, art has historically functioned as a storehold of wealth across generations and across regimes.

Rare Collectibles

Rare collectibles, such as stamps, coins, and other items that have historical or cultural significance, can be valuable and serve as a store of wealth. This can also include things like wine, scotch, watches, vintage cars, sports memorabilia, rare books, and historical documents.

These assets are often not correlated with other investments, making them a useful diversification tool.

The same caveats apply as with art. No income, real carrying costs, high transaction costs, illiquid markets, and high authentication and condition risk. The collectibles market is also notoriously prone to bubbles. The vintage watch market, sports trading cards, and certain segments of the wine market have all gone through cycles where prices became disconnected from any sensible valuation framework, then corrected hard.

The principle is the same as with art: at the high end, with documented provenance and serious buyers, collectibles can preserve wealth across generations. At the retail end, they’re closer to consumption with optional resale value.

Cryptocurrencies

It is controversial to include cryptocurrency as a store of value.

Crypto is almost a pure liquidity asset because it’s not an asset that’s supported by its own income stream. It essentially requires the production of new liquidity to find the next buyer.

While cryptocurrencies can be volatile, some traders/investors view them as a potential store of value over the long term due to their limited supply and decentralized nature. They are a relatively new asset class and come with higher risks compared to other traditional assets.

Crypto is also a relatively small asset class (a fraction of the size of the market of just Apple common stock, for example), so it’s normally not practical for large institutional investors or central banks, and doesn’t fit what they look for in an asset.

The case for Bitcoin specifically rests on its capped supply (21 million coins), its decentralization, and its growing institutional acceptance. The case against is that its price has been extraordinarily volatile, its correlation to risk assets has been higher than its proponents claim during liquidity stress, and its store of value thesis has not been tested through a full long-term debt cycle.

What I am saying is this: crypto may eventually function as a store of value the way gold does, but that proposition is still being tested in real time. Treat it as a small allocation in a diversified defensive sleeve, not as a one-for-one substitute for tested stores of value.

Commodity Currencies

Commodity currencies are currencies that are heavily influenced by the price of a particular commodity, such as oil, gold, or agricultural products. These include the Canadian dollar (CAD), Australian dollar (AUD), New Zealand dollar (NZD), Norwegian krone (NOK), and Chilean peso (CLP).

Commodity currencies can be a good store of value for a few reasons:

- Inflation hedge – Commodity currencies tend to perform well in times of high inflation as commodity prices typically rise with inflation. The currency tends to rise in tandem with the price of the commodity.

- Diversification – Commodity prices are often driven by different factors than traditional assets like stocks and bonds, which means commodity currencies can provide currency diversification.

- Global demand – Commodity currencies are linked to global demand for the underlying commodity. As such, they can benefit from global economic growth and rising demand for commodities.

Commodity currencies can also be subject to significant volatility, as commodity prices can be volatile themselves.

Reserve Currencies and Safe-Haven Currencies

The flip side of commodity currencies is the safe-haven currency. Historically, the Swiss franc and the Japanese yen have played this role, as has the US dollar to some extent.

The mechanism is straightforward. When global risk appetite contracts and capital outflows happen, money tends to flow to currencies issued by countries with current account surpluses, low inflation, credible institutions, and deep, liquid bond markets.

The Swiss franc has been the canonical example for decades. The yen has often played a similar role, particularly when Japanese investors repatriate capital during global stress.

The dollar is a more complicated case. It is the leading reserve currency of the leading world power, the most widely used and accepted currency of the greatest and most credible world power. That gives it safe-haven properties during global liquidity events.

But the US is undermining its reserve currency status by a number of things it is doing, including running large deficits, monetizing its own debt, weaponizing the financial system in foreign policy disputes, and tolerating a fiscal trajectory that brings the long-term debt situation closer to the point of no return.

For the non-US investor, holding some allocation in dollars has historically been a defensive move during global stress. For the US investor, holding some allocation in non-US safe havens (Swiss francs, gold, possibly some Asian currencies of fiscally credible nations) is the analogous move. Deglobalization raises the value of geographic diversification.

Less Growth-Sensitive Commodities

Less growth-sensitive commodities, such as agricultural products, can be a good store of value for several reasons:

- Limited supply – Unlike currencies, which can be printed at will, the supply of agricultural commodities is limited by what can be grown or raised in a given period. This limited supply helps protect the value of the commodity over time.

- Diverse use – Agricultural commodities have a diverse range of uses, from food and clothing to fuel and building materials. Demand can come from a variety of sources, which insulates them from economic downturns.

- Non-correlated – Agricultural commodities have historically had low or negative correlations with stocks and bonds, helping to diversify a portfolio and reduce overall risk.

- Inflation hedge – Agricultural commodity prices tend to rise with inflation (or even partially cause higher inflation), which can help to protect the value of the investment.

Geographic Diversification as a Store of Value

One last point that doesn’t fit neatly into a single asset class but matters more than any single line item: geographic diversification is itself a store of value.

The internal political order/disorder cycle, the external geopolitical order/disorder cycle, and acts of nature (droughts, floods, and pandemics) are three of the five most important drivers of change.

They all operate at the country level. A portfolio concentrated in a single country, denominated in a single currency, regulated by a single legal system, and dependent on a single set of policymakers is exposed to risks that no asset-class diversification can hedge.

Holding assets across multiple legal jurisdictions, multiple currencies, and multiple political systems is a structural defense against the kind of shocks that periodically wipe out concentrated investors. As the global order shifts, the assumption that any single country is permanently safe becomes harder to defend.

For the practitioner, this often means holding some portion of wealth in foreign equities, foreign currencies, foreign-domiciled funds, foreign-held gold, and possibly foreign real estate. The exact mix depends on the investor’s home country, tax situation, and circumstances. The principle is universal.

FAQs – Anti-Growth Assets (Stores of Value)

What are anti-growth assets and why are they important in a portfolio?

Anti-growth assets, aka defensive assets or stores of value, are investments that hold their value over time and perform well during economic downturns or recessions. Including these assets in a portfolio can help mitigate risk, provide stability, and diversify the range of environmental sensitivities, reducing overall volatility.

What are some examples of anti-growth assets?

Examples include predictable cash flow equities (consumer staples, utilities), private assets, gold and other precious metals, inflation-linked bonds, long-duration government bonds, some forms of real estate, infrastructure, farmland and timberland, art and rare collectibles, cryptocurrencies, commodity currencies, reserve and safe-haven currencies, and less growth-sensitive commodities.

The extent to which any given asset within these categories qualifies as a good store of value depends on its character and how it may change through time.

What about inflation-linked bonds?

Inflation-linked bonds (TIPS in the US, linkers elsewhere) provide a contractual real return. The principal adjusts with inflation, and the coupon is paid on the adjusted principal.

They’re one of the cleanest defensive holdings against unexpected inflation, particularly when starting real yields are positive. The inflation-indexed bond market is underappreciated and underused relative to its potential.

When are long-duration government bonds a good store of value?

Long-duration government bonds are the strongest performer in deflationary environments where the central bank still has gas in the tank to cut rates.

They are a poor store of value in inflationary environments, and especially poor when sovereign debt is being monetized. The same instrument flips from defensive to offensive depending on which environment shows up.

Can non-income-generating assets be good stores of value?

For a non-income-generating asset, if the nominal rate of return doesn’t compensate for the sum of the inflation rate and the net carrying costs as a percentage of its notional value, the owner is being stripped of economic value.

Even if something is supposedly worth a lot or increasing in nominal value, cash-flow problems can develop if the all-in holding costs are too high because the equity is illiquid.

Can cryptocurrencies be considered a store of value?

Cryptocurrencies are a controversial store of value due to their lack of intrinsic value, high volatility, and relatively small market size (less than the market cap of the largest companies).

Some traders/investors view them as a long-term store of value due to their capped supply and decentralization.

The thesis hasn’t been tested through a full long-term debt cycle, so calibrated confidence is appropriate.

How do commodity currencies provide a hedge against inflation?

Commodity currencies such as the Canadian dollar, Australian dollar, and New Zealand dollar tend to perform well in times of high inflation as commodity prices typically rise with inflation. This helps maintain the currency’s value alongside the price of the commodity.

How much of a portfolio should be in anti-growth assets?

Risk parity frameworks typically allocate 40-60% of risk (not capital) to assets that perform in non-growth environments, with the rest in growth-sensitive assets. The exact allocation depends on risk tolerance, goals, time horizon, and view on which environments are most likely.

The key principle is balance: own assets that do well when growth is rising and assets that do well when growth is falling.

Conclusion

Including some level of anti-growth assets in a portfolio can help to balance risk and provide a store of value during times of less-than-stellar economic conditions, or to simply have better balance and diversification.

The specific allocation will depend on an investor’s risk tolerance, investment goals, and market conditions, as well as where we are in the long-term debt cycle.

The deeper idea. Most investors are concentrated in growth assets and don’t realize it. They think they are diversified because they own many stocks across many sectors and many countries.

But all of those positions have the same environmental sensitivity. They all do well when growth is rising and inflation is contained, and they all do poorly together when those conditions reverse.

True diversification means owning assets with different environmental sensitivities, not just different tickers. That is what stores of value are for. Build the defensive sleeve, balance it across inflation hedges and deflation hedges, balance it across geographies and currencies, and let it do its job when the cycle turns.