Advanced Trading Strategies

Let’s look at some advanced trading strategies.

Most of what gets called “trading” is just directional betting in different costumes. The strategies in this piece are something else.

They’re relative value trades, basis trades, and arbitrage structures, the kind of positions put on by people who think about markets the way a mechanic thinks about a machine: with inputs, outputs, levers, and feedback loops.

They exist because markets are comprised of participants with very different mandates, constraints, tax treatments, regulatory burdens, time horizons, and so on, and those structural differences create dislocations between instruments that should, in theory, price off the same underlying cash flows.

Said differently: most of these trades exist because someone, somewhere, is being forced to do something for a reason that has nothing to do with fair value. A pension’s mandate changes. A bank has to shed risk under capital rules. A regulated insurer can’t hold a particular tranche. A foreign investor needs hedged dollar funding through one specific channel.

Those forced flows create the basis. The basis is the inefficiency. The trade is structured to harvest it.

Some of these aren’t directly pursuable for most traders. Not because they are conceptually hard. Because they require balance sheet, financing relationships, regulatory permissions, and operational infrastructure that retail traders and most small funds don’t have.

But they’re still worth understanding. They show the variety in how capital markets works, and they often inspire creativity in the smaller, simpler trades that ordinary traders can put on.

Let’s walk through them.

Key Takeaways – Advanced Trading Strategies

- Mortgage Basis Trade – Buy specific mortgage pools, short generic ones when pricing doesn’t match prepayment differences

- CDS Basis Trade – Buy a company’s bond, hedge with CDS when spreads don’t match

- On/Off-the-Run Treasury Trade – Short newest Treasury, buy older one, profit as liquidity premium fades over time

- Interest Rate Swap Spread Arb – Trade swaps against Treasuries when their yield gap looks unusual relative not necessarily to history but balance sheet costs

- Covered Interest Rate Parity Arb – Borrow cheap currency, invest higher-yield one, hedge the FX risk

- Convertible Bond Arbitrage – Buy convertible, short stock, dynamically hedge and profit from volatility mispricing and coupon income

- Capital Structure Arbitrage – Trade stock vs. debt, depending on relative valuation

- Curve Arbitrage – Trade different maturities when the yield curve looks distorted relative to expectations

- Municipal Bond Relative Value – Buy cheap munis (sometimes shorting more expensive ones)

- Sovereign Debt Basis Trade – Trade bonds vs. CDS

- EM External vs. Local Debt Arb – Choose between dollar debt or local debt depending on crisis stage, currency weakness, and reserve strength

- Securitization Arbitrage – Trade ABS vs. MBS when structurally similar assets diverge due to demand differences

- Index Arbitrage (CDX vs. Bonds) – Trade index vs. bonds (long cheap/short expensive)

- Volatility Arbitrage – Long cheap volatility vs. short expensive vol

- Correlation Convergence – Trade index vs. single stocks

- Mortgage Derivative Basis – Trade interest-only vs. principle-only

- Equity/Fixed Income RV – Trade stock vs. debt when valuation gaps appear across capital structure due to forced flows or stress

- Cross-Currency Basis Swaps Arb – Profit from global dollar funding imbalances and demand for hedged USD exposure

- Inflation Basis Trades – Trade TIPS vs. swaps

- Credit Contingent Notes RV – Compare structured notes vs. CDS

- Callable/Putable vs. Vanilla Arb – Compare option-embedded bonds vs. plain bonds to isolate and trade mispriced volatility

- Mortgage Refinancing Spread Trade – Trade gap between mortgage rates and bond yields driven by origination capacity and refinancing waves

- ABCP Arbitrage – Trade short-term credit instruments when yields diverge

- CLO Tranche Arbitrage – Trade different layers of CLOs when they’re priced inconsistently

- Dividend Arbitrage – Trade stocks around dividends based on tax and market behavior

- Merger Arbitrage – Buy takeover target (often short acquirer); profit if deal closes

- ETF Arbitrage – Profit when ETF price differs from underlying assets; short expensive, long cheap

- Repo Specialness – Lend in-demand bonds at premium rates

- Closed-End Fund Arbitrage – Buy funds trading below asset value, wait for gap to close

- Cash-and-Carry Futures Basis – Buy asset, sell futures to lock in price difference

- SPAC Arbitrage – Buy below cash value, redeem later for guaranteed return

Mortgage Basis Trade (Long/Short MBS Pools vs. TBA)

This trade pairs positions in mortgage-backed securities (MBS) pools with offsetting positions in the “to-be-announced” (TBA) market, which is a forward contract for the delivery of MBS pools.

The mechanism. The TBA is the most liquid pool of mortgage-land. It trades on six standardized parameters and the seller has the option to deliver the cheapest pool that meets them.

So the TBA price is, by construction, the worst deliverable pool. Any specific pool with better characteristics trades at a premium called the “specified pool pay-up.”

A pool with low loan balances prepays more slowly. So does a low-FICO pool, or one concentrated in states where refinancing is operationally hard. Each of those characteristics has economic value because it reduces prepayment risk, and that value should be reflected in a pay-up.

When the pay-up is too low relative to the modeled value of the protection, you go long the specified pool and short the TBA.

When it’s too high, you reverse.

The pay-ups are highly sensitive to rates: when refinancing waves hit, slow-prepay pools become much more valuable. So you’re also taking a position on prepayment volatility.

CDS Basis Trade (Long Bond/Short CDS or Vice Versa)

Take opposing positions in a bond and its corresponding credit default swap.

Long bond, short CDS, or vice versa, to capture the difference between the bond’s yield spread and the CDS premium.

In theory, the two should be the same. Both price the same default risk on the same entity.

In practice, they almost never are. CDS contracts have specific trigger definitions and a standard auction process. Bonds have specific covenants, embedded options, and capital structure ranking.

The “cheapest-to-deliver” option in CDS settlement creates a wedge. And critically, the two are funded differently. The bond requires funding the cash position. The CDS does not.

That funding wedge is what drove the 2020 dislocation. When dealer balance sheets contracted under stress, the cash bond market gapped wider than the CDS market because nobody could finance the bonds.

Anyone in a “negative basis” trade (long bond, short CDS) at that moment got run over before it converged.

This is classically what happens in these trades: they look free – i.e., capturing the yield differential – until they aren’t. As a trader, the rule is to size them according to the funding stress you can survive, not the historical mean reversion you expect.

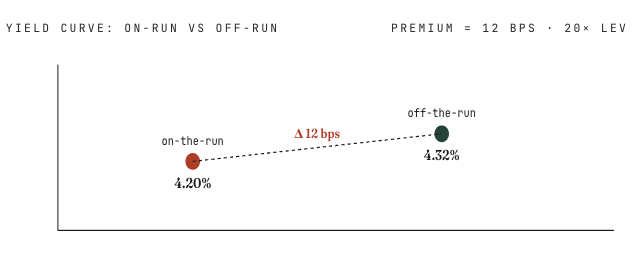

On-the-Run / Off-the-Run Treasury Basis Trade

This trade captures the yield difference between the most recently issued (“on-the-run”) Treasury and older (“off-the-run”) issues of the same maturity.

The on-the-run trades at a lower yield because it’s the benchmark, the most heavily traded, which is what hedgers and central banks demand. It carries a “liquidity premium.”

Over time, as a new auction creates a new benchmark, the on-the-run becomes off-the-run, and the liquidity premium decays.

The trade: short the rich on-the-run, long the cheap off-the-run, financed in repo, earn the convergence as the bonds age into each other.

For example, if the differential is 12bps (0.12%) and 20x leverage is applied, that gives a 2.4% yield, which can be worthwhile for mispricings that close relatively quickly.

The classic case is LTCM in 1998. The trade was correct in its long-run logic. The convergence did happen, eventually.

But the spread widened violently first as the world fled to the most liquid instrument, and the leverage required to make it economic produced losses that wiped the fund out before it could collect.

So therein lies the issue with all relative value trades: the math works on average, but the path matters more than the average.

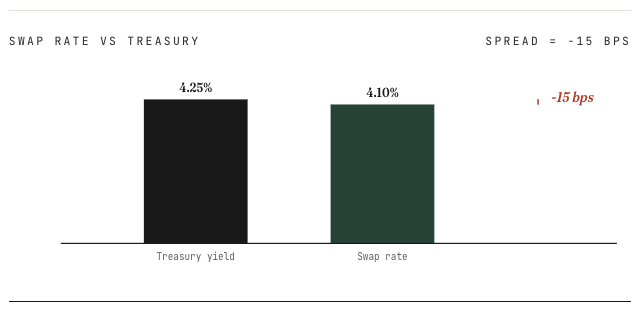

Interest Rate Swap Spread Arbitrage

Take opposing positions in interest rate swaps and Treasuries of the same maturity. Profit from the spread converging to its historical norm.

This is worth thinking about because swap spreads have done something genuinely strange since the GFC – they went negative. For example:

That should be impossible if you think about it naively, because the swap rate is supposed to embed bank credit risk over the “risk-free” Treasury rate.

How does a credit-risky rate trade below the risk-free rate?

The answer is that “risk-free” was never quite right. Treasuries require balance sheet to hold. Swaps don’t.

As post-crisis regulation made balance sheet expensive (the Supplementary Leverage Ratio, capital charges on dealer inventory), the price of that balance sheet started showing up in Treasury yields.

Treasuries got cheap because they were a balance sheet hog. Swaps got rich because they weren’t. As a derivative, they generally require less collateral to hold. The spread inverted.

Put another way: the swap spread is no longer a credit spread. It’s a balance sheet rent.

Covered Interest Rate Parity Arbitrage

This trade works as such:

- Borrow in the low-interest-rate currency

- Convert proceeds into the high-interest-rate currency (spot market)

- Invest in a higher-yield asset denominated in that currency

- At the same time, enter a forward contract to sell the high-yield currency

- Lock in the forward exchange rate at trade initiation

- Hold position until maturity

- Repay original loan + interest

- Capture risk-free arbitrage profit if parity is violated

For decades, covered interest parity was treated as a textbook identity. It was the closest thing to a free arbitrage the literature (and many practitioners) recognized.

Since 2008, it has failed to hold. The cross-currency basis has been measurable, durable, and at times very large.

Why? Same reason as the swap spread. Balance sheet became expensive.

The arb requires a bank to put on a fully hedged FX position, and the regulatory cost of that position now eats most or all of the theoretical profit.

The cost of bank capital is now embedded in what used to be called a free trade. The inefficiency didn’t disappear because the market got smarter.

It exists because the regulatory regime changed in a way that makes the arbitrage impossible to do at scale without paying a balance sheet rent. The trade is a way to extract that rent.

Convertible Bond Arbitrage

Long the convertible bond, short the underlying stock in the right delta-neutral ratio. As the stock moves, re-hedge.

A convertible is a bond plus an embedded equity call option. Decompose the two pieces, value them separately, and you have a theoretical price.

If the market price is below theoretical, you buy the convert and short the stock. The position throws off “gamma” income from stock volatility, plus the bond coupon, minus the cost of the short.

It works best in two regimes. Heavy convert issuance, which causes new paper to come at concessions and creates a steady pipeline of cheap volatility. And realized volatility running higher than the implied volatility embedded in the convert at issuance.

Both conditions tend to coincide with stress in equity markets, which is also when financing costs spike and forced unwinds hit.

This is classically how the trade blows up: cheap volatility, high financing cost, forced selling. 2008 was the textbook case.

Capital Structure Arbitrage (Bonds vs. Loans vs. Stocks)

This trade exploits relative mispricing within a company’s capital structure. Long an undervalued bond and short an overvalued stock of the same firm, or vice versa.

The intellectual framework is Merton’s structural credit model: the equity is a call option on enterprise value, struck at the face of the debt. If you know the volatility of the enterprise and the leverage, you know what each piece should be worth conditional on the others.

In practice, the model is a starting point, not an answer. Different parts of the capital stack are owned by different investor bases with different mandates.

Loans live with banks and CLO managers. Bonds live with insurance companies and credit funds. Equity lives with everyone.

When one base gets stressed and forced to sell, the mispricing across the cap stack can be very large. The trade is to identify which leg is being driven by flow rather than fundamentals, take the other side, and wait for the structural model to reassert.

Curve Arbitrage (Across Different Maturities)

Take opposing positions in interest rate instruments at different maturities. Profit from mispricing between points on the yield curve.

The shape of the curve is set by two things: expected future short rates, and the term premium for taking duration risk. Both move.

When the curve has a kink at a particular maturity, that kink either reflects a real shift in expected policy at that horizon, or a flow imbalance. It’s often driven by mortgage servicer hedging, insurance duration matching, or sovereign reserve managers.

A “butterfly” trade isolates the kink. Long a barbell of two- and ten-year instruments, short a bullet of fives, or vice versa. You’re left with a position roughly neutral to parallel curve shifts and to slope shifts, but exposed to curvature.

The hard part is figuring out whether the curvature is information or flow.

Municipal Bond Relative Value Trades

Long undervalued munis, short overvalued ones. Or hold the cheap ones and collect the carry.

The municipal market is structurally inefficient and has been for as long as it has existed. The reason is the tax treatment.

Munis are owned almost exclusively by US tax-paying individuals, because the tax exemption is what creates the yield. International investors, sovereign wealth funds, and tax-exempt institutions have no real reason to be there.

That investor base is unsophisticated relative to corporate credit. The trading is fragmented across thousands of small issuers. Dealer balance sheet in munis is a fraction of what it is in Treasuries.

The result is that ratings, credit research, and relative value all get priced lazily. Two bonds with nearly identical credit profiles can trade at very different yields because one is a well-known issuer and one is a small school district nobody covers.

The trade is to do the credit work the market hasn’t done, buy the cheap obscure bond, and either hedge or sit on the carry.

The market isn’t deep enough for everyone to do this, which is precisely why the inefficiency persists.

Sovereign Debt Basis Trades

Long the sovereign bond, short the CDS, or vice versa. This gets the basis as it converges.

The sovereign version has an extra wrinkle the corporate version doesn’t:

- what currency is the bond in

- what currency does the CDS settle in, and

- what happens if the country redenominates

During the eurozone crisis of 2010-2012, the basis on peripheral sovereigns blew out. The bonds were Italian-law, euro-denominated.

The CDS was English-law, euro-denominated. If Italy left the euro, the bond might convert to lira, but the CDS would still pay in euros.

That redenomination risk priced very differently into the two instruments and produced a basis that wasn’t really a mispricing at all – just a measurement of how the market priced the probability of a euro break-up.

When a basis blows out, the right question isn’t always “when does it converge?”

Sometimes it’s “what is the basis actually pricing that I haven’t thought about?”

Emerging Markets External / Local Debt Arbitrage

This trade plays the relative value between emerging market sovereign debt denominated in a major reserve currency (e.g., USD) and local currency.

The structural difference: external debt is a claim on the country’s hard currency reserves. Local debt is a claim the country can print to repay.

In virtually all past cases, when an EM country gets into trouble, the path is the same. Capital outflows tend to happen when the environment is inhospitable. The currency weakens. Local-currency real bond yields rise. External debt either gets serviced (because losing reserve currency access is fatal) or restructured (because reserves run out).

Knowing where a country sits on that path tells you which leg to be on.

If reserves are adequate and the currency weakness is temporary capital flight, local debt at distressed real yields can be the trade.

If the country is heading toward default on external obligations, external debt at par is the short.

This is the EM version of distinguishing between a solvency problem and a cash-flow problem.

Securitization Arbitrage (ABS vs. MBS)

Long undervalued ABS, short overvalued MBS, or some structured combination.

Why mispricing exists: who can hold what. MBS is a benchmark asset. It sits in nearly every fixed income index, every bank’s available-for-sale book, the Fed’s balance sheet.

ABS is more bespoke. Different sub-sectors (auto loans, credit cards, student loans, equipment) have different specialist investor bases, and when one experiences a flow disruption, spreads can move violently relative to MBS without underlying credit fundamentals changing at all.

The hard part is that documentation, prepayment behavior, and cash flow profiles are all different across sectors, so the hedge is never clean. You’re always taking residual basis risk, and the residual is what makes or breaks the trade.

Index Arbitrage (Cash Bond Portfolio vs. CDX)

Construct a portfolio of bonds that closely replicates the CDX index, then take an opposing position in the index. Capture the basis.

When credit fund flows are positive, money tends to come into cash bonds first because that’s the natural vehicle for credit funds, and the cash bonds richen relative to the index.

When credit deteriorates, hedging demand pushes the index wider faster than the cash bonds can move. The basis flips. So the trade gives you a way to express a view on the flow of credit money rather than on credit itself, which is a different thing.

Volatility Arbitrage (Options vs. Realized Vol)

Short overpriced options, long underpriced ones. Profit from the convergence of implied volatility and realized volatility.

There is a structural reason implied volatility tends to run above realized in equity index options.

The buyers are pension funds, asset managers, and corporates hedging tail risk. They are relatively price-insensitive demanders of insurance.

The sellers are dealers and vol funds, and they require a risk premium for taking the other side. That premium is the variance risk premium – aka volatility risk premium – one of the most durable risk premia documented in financial markets.

Durable doesn’t mean monotone. In the realized vol shocks of 2008, 2020, and a few briefer episodes since, the people who were systematically short variance lost catastrophically in days. At the same time, it’s hard for longs because the high payouts are so infrequent.

The trade is structurally profitable on average but structurally lethal at the tails. What matters isn’t whether the average is positive (it is) but whether your size lets you survive the tail.

Correlation Convergence Trades

Profit from mispricing in the correlation between assets.

The cleanest expression is dispersion: short index variance, long a basket of single-stock variance.

The spread between those two is implied correlation. When implied correlation is high relative to what realized correlation is likely to be, the trade is profitable on average.

When markets enter a crisis and everything moves together, realized correlation spikes and the trade loses fast. You are short a particular form of insurance, this time against everything moving together, and you collect a premium most of the time and pay it out in the tails.

Mortgage Derivative Basis Trades

The two halves of an MBS are an interest-only (IO) strip and a principal-only (PO) strip. They have very different sensitivities to prepayment.

When rates fall, prepayments accelerate (people refinance their mortgages), principal comes back faster (good for PO holders), and the interest stream shortens (bad for IO holders).

Their durations are mirror images and very large. So when prepayment expectations embedded in IO/PO pricing diverge from what the rates and refinancing market are telling you, there is a trade.

Sometimes used as a directional rate hedge with attractive convexity, sometimes as a relative value play between the two halves and the whole pool.

Equity / Fixed Income Relative Value

This is cap structure arb expressed across the equity-debt boundary specifically.

Where it gets most interesting is in distressed situations. As a company approaches insolvency, the equity becomes a deep out-of-the-money call option on firm value, and the debt prices increasingly like a recovery claim.

The relative value can shift very quickly, and the legal architecture of the bankruptcy (e.g., priority, fulcrum security, equity wipeout) is what determines who gets what. Many of the best distressed credit funds are really cap structure arb shops with an in-house legal capability.

Cross-Currency Basis Swaps Arbitrage

The cross-currency basis tells you something few other prices tell you: how badly someone needs dollar funding.

When global dollar liquidity tightens, foreign banks and corporates that need dollars to fund their dollar assets bid aggressively for them through the basis swap. Hence, the basis goes deeply negative. Watch the yen and euro basis through periods of stress.

The 2008, 2011-12, and 2020 episodes all show the same pattern. The Fed’s swap lines with foreign central banks were created precisely to relieve that pressure. This makes the basis a useful indicator even for those who never trade it. It’s, in effect, a real-time price of global dollar scarcity.

Inflation Basis Trades (TIPS vs. Swaps)

Long TIPS, short inflation swaps, or vice versa. Profit from the inflation basis converging.

The inflation-indexed bond market tends to be underappreciated and underused relative to its potential.

The real bond yield is the most important number to watch in the financial world, because it’s the foundational rate for all capital markets and tells you what real return you can certainly get, free of inflation risk and default risk, on your wealth.

The basis between TIPS and inflation swaps is in part a measure of how well that real yield is being priced.

The trade can also be structured to achieve a strategic goal, such as having the portfolio better protected from inflation over time, which is often the more important use case than the arbitrage itself.

Note that TIPS are not inflation swaps. In other words, they’re not a pure inflation hedge. They still carry duration/interest rate risk.

Credit Contingent Notes Relative Value

Credit contingent notes (CCN) are debt securities that transfer a portion of credit risk from the issuer to the investor/trader, with the principal amount adjusted based on the credit performance of a reference entity or portfolio.

The arb compares CCN pricing to the implied price of the same risk in CDS or cash bond markets, and trades the difference.

Callable / Putable Bonds vs. Vanilla Arbitrage

A callable bond is a vanilla bond minus a call option that the issuer holds. A putable bond is a vanilla bond plus a put option that the holder holds.

The market should price each accordingly.

When it doesn’t, you can construct the implied option from the spread between the two bonds and check it against the option-adjusted spread implied by your model.

If the implied vol embedded in the callable looks too low, you go long the callable and short the vanilla, effectively buying volatility cheap. If it looks too high, you reverse.

Let’s run through an example:

- Vanilla bond: 5% yield, price = 100

- Callable bond (same issuer/maturity): price = 98 -> implies cheap call option

Model says embedded call should be worth 3 points, but market implies only 2 -> vol underpriced.

Trade:

- Long callable (98)

- Short vanilla (100)

You’ve synthetically bought volatility cheap via the mispriced embedded option.

If pricing normalizes (call value -> 3), callable rises relative to vanilla -> profit from spread convergence.

Mortgage Refinancing Spread Trades

The “primary-secondary spread” is the gap between the rate the homeowner pays and the rate the MBS trader receives. It’s essentially the cost of origination, servicing, and capacity in the mortgage banking system.

When refinancing waves come, capacity gets strained and the spread widens. When refinancings collapse, capacity is excess and the spread compresses.

Watching this spread tells you a lot about the actual transmission of monetary policy into the housing economy.

Asset-Backed Commercial Paper Arbitrage

Trade ABCP yield spreads against other money market instruments. Worth remembering: in 2007, the ABCP market was the canary.

When prime money market funds started refusing to roll ABCP, that was the beginning of the credit contraction that produced the depression of 2008 (same type of dynamic as 1929 but with faster response). The pricing dislocation that summer was, in retrospect, an enormous tell.

CLO Tranche Relative Value Arbitrage

CLOs repackage corporate loans into tranches with varying levels of risk. Different tranches go to different investor bases.

AAA tranches go to banks and Japanese institutional money. Mezzanine goes to credit funds and insurance companies. Equity goes to a small set of specialists.

Because each base has its own cycle of demand and forced selling, the tranches frequently move out of line with the underlying loan portfolio.

That dislocation is the trade.

Dividend Arbitrage using Bond / Equity Positions

Long the undervalued security around an ex-dividend date, short the overvalued one. The mispricing comes from different tax treatments and different reactions among holders to the dividend payment.

Tax-exempt holders, taxable individuals, and foreign institutions all process dividends differently, and that produces predictable flows in bonds and equity around payment dates.

Merger Arbitrage

Long the target of an announced acquisition, short the acquirer if there’s stock consideration.

After an announcement, the target trades at a discount to the offer price. This has to do with deal probability, time to close, and financing cost. The arb captures that discount as the deal closes, or eats the loss if it breaks.

The structural reason the discount exists is that the natural holders of the target stock want to sell into the bid and redeploy capital, and the natural buyers of deal risk are a small set of arb funds with the legal, regulatory, and antitrust analytical capacity to underwrite it.

The payoff profile looks like a short put on deal completion: small positive returns most of the time, occasional large losses when deals break.

In tightening regulatory environments, especially for cross-border deals or large horizontal mergers, break risk is materially higher than naive historical averages suggest.

Merger arb is also wanted for its diversification value, as it doesn’t have traditional correlation to other assets. That said, there’s still modest correlation, as M&A is more likely to happen and go through during times when the markets and general economy are doing well.

ETF Arbitrage (NAV vs. Creation/Redemption)

When an ETF trades at a premium, authorized participants deliver the basket of underlying securities to the issuer, receive ETF shares, and sell them in the market for a small profit.

When it trades at a discount, they buy the ETF, redeem for the basket, and sell the basket. This continuous arbitrage is what keeps ETF prices anchored to NAV.

It gets interesting when liquidity in the underlying basket dries up. In high-yield bond ETFs and emerging market debt ETFs in 2020, the basket essentially stopped trading.

The ETF kept trading, because the secondary market for the ETF was deeper than the secondary market for the bonds inside it. The ETF dropped to a substantial discount to its stale NAV, and the question for arbs was whether the ETF was at a discount or whether the NAV was simply wrong.

Price is a transactional concept. NAV is a reported number. When liquidity disappears in the constituents, the ETF’s discount is the better signal of true value, not the other way around.

Repo Specialness

When a particular Treasury issue is heavily shorted (often because traders are using it to hedge other positions), demand to borrow that bond in repo runs above the general collateral rate.

The owner can lend it at a much lower repo rate and earn a “specialness” premium.

Some of the most consistent income in fixed income relative value comes from holding the bonds that are most heavily shorted and lending them into the squeeze.

The rent exists because (1) the specific bond has become operationally essential to a particular hedging trade, and (2) the owner has pricing power over the people who need it.

Closed-End Fund Arbitrage

Unlike ETFs, closed-end funds have no creation/redemption mechanism, so prices can drift far from NAV and stay there for long periods.

Buy at deep discounts, then either wait for the gap to close (it sometimes does, slowly) or push for it through activism – e.g., open-ending the fund, tendering shares at NAV, replacing the manager.

The discounts tend to last because the natural holders are retail investors who bought at IPO and have inertia, and the natural arbitrageurs face the friction of needing to take action to realize value rather than just holding and waiting.

Cash-and-Carry Futures Basis

The oldest arbitrage out there.

When a futures contract trades above the spot price plus the cost of carry (financing, storage, dividends), sell the future, buy the spot, finance the position to delivery, and lock in a riskless profit.

Reverse when it trades below.

In equity index futures, the carry is mostly financing rates and dividends.

In commodity futures, it includes storage.

In Treasury futures, it includes the implied repo rate, and the cheapest-to-deliver option creates wrinkles similar to the TBA market in mortgages.

The existence of this basis is largely about balance sheet rent. The trade requires real money to finance the cash leg, and real money is more expensive than it used to be.

Example

For example, consider this trade on the S&P 500, using ES (e-mini futures) and the ETF SPY.

Short the e-mini:

Long the ETF (cash market):

So after transaction costs, you’re getting around $16,100+ in profits.

If this trade runs 230 days (i.e., until the end of the future contract), this is 0.63 years.

So to calculate the yield, it’s the annualized profit divided by the cash market investment.

Yield = $16,100/0.63 / $720,000 = 3.55%

This should roughly match up with prevailing Treasury yields of the same duration.

SPAC Arbitrage

After a SPAC‘s IPO, its shares are essentially short-dated Treasury bills (the IPO proceeds sit in trust earning interest) plus a free option on the eventual deal.

When the SPAC trades below trust value, buy the shares, redeem for trust value at the deal vote, and pocket the spread plus the optionality of the warrants.

The trade was extremely consistent during the SPAC boom, less so afterwards, because the structural features that made it work depended on a particular regulatory and investor-base configuration that has since changed.

What These Trades Have in Common

Look across the list and a few patterns emerge.

The Influence of Constraints

First, almost every one of these trades is a way of capturing a structural rent that exists because someone is constrained.

The constraint might be regulatory, institutional, informational, tax-related, or operational.

The rent is the price the constrained party pays to the unconstrained party for taking the position they cannot.

Similar Return Profile

Second, almost every trade has a similar return profile: small, consistent gains most of the time, with rare and severe drawdowns when the structural conditions that created the rent shift suddenly.

The variance risk premium pays out most of the time and crushes you the other less frequent times. The CDS-bond basis converges most of the time and explodes when funding markets seize. Covered interest parity is profitable until balance sheet costs blow it out.

Understanding Cause and Effect

Third, almost every trade is fundamentally about understanding the cause-and-effect chain that produces the basis.

- Why does this dislocation exist?

- Who is forced to be on the other side of the trade?

- What conditions would relax their constraint?

- What conditions would tighten it further?

Until you can answer those questions, it’s more about guessing at mean reversion and hoping the path is short.

What These Trades Reward

These trades reward traders who think about the underlying mechanics of how these trades work, who understand the institutional architecture that produces prices, and who size their positions according to what they can survive rather than what the historical average suggests they should expect.

The math of any individual trade is rarely the hard part. The hard part is understanding the underlying cause-effect mechanics that produce the inefficiency. They anticipate when that machine is about to stop producing it and get out before the path matters more than the destination.

Circumstances vary considerably. Most readers won’t run any of these trades themselves. But it provides awareness and can jumpstart your creative juices. Understanding how they work changes how you read every other price in the market.