Trade Slippage

- The Anatomy of a Trade: The Journey of a Packet

- The Hidden Culprits: Hardware and Local Infrastructure

- Understanding Intermediaries and Global Routing

- Broker Execution Models and Liquidity

- MM/DD brokers, STP brokers, ECN brokers, DMA, and Hybrids

- Market Conditions: The External Triggers

- Negative Balance Protection (NBP)

- Slippage Mitigation Strategies for Traders

- Order Selection

- Legal and Regulatory Perspective

Slippage is the difference between the price a trader expects and the price at which the order is actually filled (position opened or closed). On paper, that sounds simple. In practice, it sits at the intersection of market structure, network latency, broker routing, local hardware, liquidity depth, and timing. That is why slippage tends to attract bad explanations. The most common one is also the laziest: if the fill was worse than expected, the broker must have done something crooked. And yes, sometimes a sketchy or low-quality broker is the problem. And sometimes it is something else. Sometimes the setup is poor, the liquidity is thin, the order size is too large for the available depth, or the market moved before the order could reach the final venue. Either way, it’s essential that day traders understand the role of slippage, as it can have a real-world impact on trading results.

Often, slippage is not caused by just one thing; it is a chain of contributing factors that work together to make the slippage more noticeable. One weak link adds a millisecond here, another adds a half millisecond there, and so on. In fast conditions, that can be enough for significant slippage to occur.

Slippage is commonly expressed as:

Slippage = Executed Price − Requested Price

For a buy order, a higher executed price than requested is negative slippage. For a sell order, a lower executed price is negative slippage. What matters is whether the fill improved or worsened the economic result for the trader.

Positive slippage exists too. But, of course, you will not hear traders complain about those situations. If a buy order is filled below the requested price, or a sell order is filled above the requested price, the trader receives price improvement, and this is positive slippage.

Traders should treat slippage the same way they treat spreads, commissions, and financing: as an execution cost that can be measured, reduced, and compared, but never fully eliminated. Anyone promising zero slippage in all conditions is usually selling a fantasy, or hiding the trade-off somewhere else.

So, the practical question is not whether slippage exists. It does. The question is where it is coming from and how your trading must account for slippage based on your setup, your broker, your product, and your time of day. That is the part worth dissecting. Slippage is a cost of doing business. Not a moral event, not a conspiracy by default, and not something a retail trader can eliminate.

The right response is acceptance and improving what is possible and worthwhile to improve, based on your specific situation and trading strategy.

A few examples of factors that can reduce your issues with slippage:

- Use a computer that is fast and reliable.

- Use an internet connection that is fast and reliable.

- Consider a VPS near the broker’s server.

- Respect liquidity depth.

- Understand the different execution models and make an informed decision.

- Use limit and stop limit structures when price control matters more than fill certainty.

- Select a broker with strong liquidity and a clear execution policy. Keep records and compare brokers on actual fills.

- Do not keep your computer and internet connection busy with other tasks when you are trading.

- Avoid the worst timing windows unless the strategy explicitly depends on them and can survive the execution cost.

- Do not use WiFi. Use a wired connection where an Ethernet cable is plugged into your computer.

The Anatomy of a Trade: The Journey of a Packet

Every trade begins with a decision, but execution begins with a packet.

A trader places an order. That action creates an instruction containing the symbol, volume, order type, and any relevant price conditions. At that instant, the order has not entered the market. It exists only on the local device and in the software stack. This is the first place where the imagination of an inexperienced trader and the real process part ways. Novice traders often picture a straight line from click to fill, with no hurdles along the way. In reality, the journey involves several steps, and each one can add challenges.

This is why the complaint “But I clicked at that price” is of limited value. You clicked when your local platform displayed that price. That is not the same as saying executable liquidity at that price still existed when the order reached the venue. Those are two different moments, separated by hardware, software, cables, routers, servers, and market movement. In normal market conditions, the chain can feel invisible. During sudden market storms, slippage can suddenly become brutal.

1. Local Processing

The first stage of the chain is local. When a retail trader clicks “buy” or “sell”, the trading platform (e.g. MetaTrader 5) installed on their computer creates an order request and hands it off to the operating system’s networking stack. From there, the system queues the data for transmission. The network interface (your Ethernet or Wi-Fi adapter) sends the packet to your home router, which then forwards it to your internet service provider.

Delays can already occur at this stage. Not because each component is independently “deciding” things in sequence, but because they share resources. If the computer is under load (e.g. CPU spikes, limited RAM, background processes like updates are going on, or other browser tabs are sucking resources), the trading platform may take longer to generate or dispatch the order. The operating system might also delay network scheduling slightly under contention.

Wi-Fi can introduce extra instability compared to wired connections, and cable and DSL connections tend to have more variable latency than fiber.

All these delays can be tiny in human terms (think milliseconds) and still be enough for prices to move if the market is fast. By the time the order leaves your home network, it may already be behind the current market, which is where slippage begins.

2. From Your Location To Your ISP’s Nearest Network Point

The second stage is the connection from your home (or other location) to your internet provider’s (ISP’s) nearest network point. This stage consists of the link (e.g. fiber, cable, or a phone line) that carries your order from your router to your ISP’s nearest network point. It is the path between your home and the wider internet.

For a retail trader, this part of the connection can be one of the most important, but also most overlooked, sources of execution problems. Consumer internet is designed for everyday activities like streaming video, browsing, and gaming. Small delays and inconsistencies that do not bother you during these activities can still be enough to contribute to slippage. Even if your connection feels fast, that usually refers to download speed, not upload speed and consistency.

On a typical home connection, the time it takes for your order to reach your broker’s server is not perfectly stable. One order might take 18 milliseconds, the next 70, the next 24. This variation is called jitter. You usually don’t notice it, but in trading it can affect execution. If your order arrives quickly, it is more likely to be filled at the price you saw. If it arrives a few milliseconds later, the market may have already moved, and you will experience slippage.

These inconsistencies often originate in your home connection itself. Your line is shared with other users in your area, and network congestion can come and go. Importantly, these are not full outages. Your internet does not “go down”. Instead, it becomes slightly inconsistent, and that inconsistency is enough to put your order behind others in fast markets. If your connection delivers your orders at uneven speeds, you are occasionally trading on stale prices, and this can add up over time.

Consumer internet connections are built for average consumer use. Even though using online banks and brokers is now common, the type of trading where milliseconds matter is not considered average use. A line that feels fast while streaming video and gives you the advertised download speed can still show unstable latency, packet loss, jitter, and micro interruptions.

3. From The ISP Network Point To The Trading Server

From the ISP network point, the order moves through upstream networks and backbone providers, and this is where routing decisions start to matter. Your order does not travel on the physically shortest line to the broker’s infrastructure. It travels on the path chosen by the network, subject to peering arrangements, congestion, handoffs, and available routes.

A trader in Madrid connecting to a London-based trading server may get an efficient path one moment and a slightly worse one the next. A trader in São Paulo routing to New York may go through several major carriers before reaching the target data center. Each hop adds opportunity for delay.

4. But What If I Use A Web Browser Trading Platform?

Today, many retail traders use a web browser trading platform instead of installing the platform software on their computer. This changes the exact mechanics a bit, but not dramatically.

When a platform such as MetaTrader 5 (MT5) is running on your computer, the platform talks more directly to the operating system and network stack. If you are using the web version instead, running in something like Google Chrome or Mozilla Firefox, there’s an extra layer to consider: the browser itself.

Let’s assume you are using MetaTrader 5 in a browser window. The browser is now on the critical path. If it’s busy (many tabs, extensions, heavy scripts), it can delay execution or network dispatch. The MT5 web app runs in JavaScript, which shares a single main thread (mostly). If something blocks it, even just briefly, your order submission can be delayed. Ad blockers, security tools, or other extensions can also interfere with or slow requests. Also, if your trading tab isn’t active, that can introduce extra latency, because browsers frequently deprioritize background tabs.

With that said, OS scheduling, system load, network interface, router, and ISP latency still matter as well. You can not get away from those potential friction points by using a web platform instead of installing the trading software on your computer. If anything, the web version is usually slightly more fragile in terms of latency consistency. If you’re optimizing for execution quality (and not just convenience), the desktop version or a VPS setup is generally more predictable.

5. The Broker’s Server and Order Routing

During the next stage, your order finally hits the broker’s server. This is another frequently misunderstood stage. What traders call “the broker” is often several layers of software and routing logic, and the broker’s server can be, but is not always, the final execution venue.

In many models, the broker’s software will authenticate the client, validate margin, check symbol parameters, confirm the order format, and then either match internally or forward the order onward to a liquidity bridge. If the order is passed outward, it reaches a bridge or aggregation layer and then one or more liquidity providers. This is where book depth starts to matter. The top of book might show a price for a small amount of volume, but your order may require more liquidity than that level offers. The result is partial fills across several levels or a single average price that reflects multiple executions. The trader sees one completed trade. Behind that, the fill may have been assembled from several pieces.

Let’s take a look at this stage in more detail:

Let’s say you are using MT5 and your order has just arrived at the broker’s trading server. At this point, the system performs pre-trade checks. It verifies that your account is valid, confirms you have enough margin, ensures the order parameters are acceptable for that instrument, and checks internal risk limits. If anything fails, the order is rejected immediately and never reaches the market.

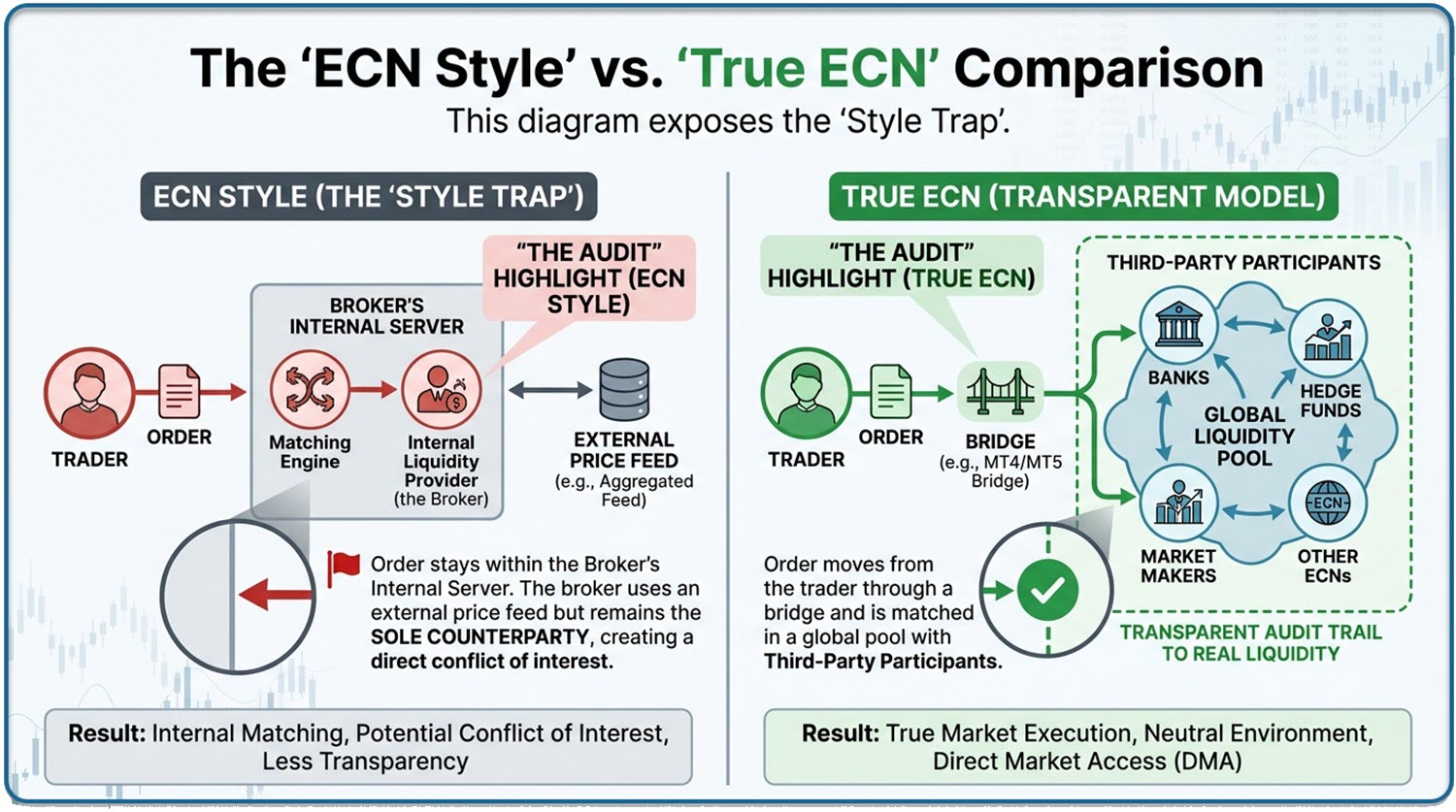

If the order passes validation, it moves into the broker’s execution infrastructure. This includes an order management system, which tracks the order’s lifecycle, a risk management system that enforces exposure limits, and routing components that determine where the order will actually be executed. The key distinction at this stage is whether the broker executes the order internally or routes it outward. What happens now will largely depend on which type of broker you are using, e.g. Dealing Desk (DD) broker, Straight-Through Processing (STP) broker, or Electronic Communications Network (ECN) broker.

If the broker operates as a principal, often called a market maker (MM broker), it internalizes the order. That means the broker itself becomes the counterparty to your trade and fills it from its own inventory or by offsetting it against other client orders. This process is called internalization. The broker may choose to keep the resulting market exposure or hedge it elsewhere, but from your perspective the trade is completed within the broker’s own system.

When an order is instead routed externally, it passes through a bridge or gateway into the broader liquidity network. This can include banks such as JPMorgan Chase or Deutsche Bank, as well as non-bank liquidity providers like XTX Markets or Citadel Securities. In some cases, an order is sent into electronic matching venues such as EBS or Refinitiv Matching, where multiple participants compete to provide liquidity.

Note: Many brokers pass the order through a liquidity aggregator instead of sending it straight to the liquidity venue. A liquidity aggregator collects quotes from multiple providers and constructs a composite order book, allowing the broker to select the best available price at that moment. This is still an over-the-counter environment, so there is no single centralized exchange, but the aggregator approximates one by consolidating fragmented liquidity.

6. The Order Is Executed!

Finally, the order is executed, either internally or at an external venue. A fill is generated, which may be complete or partial depending on available liquidity. Confirmation must now travel back through the same chain of systems to your computer for you to know what’s going on.

7. Confirmation Travels Nack

After execution, the confirmation travels back along the chain in reverse. The broker server processes the response, updates the account state, sends the result to the platform, and the platform finally prints the fill. Only then does the trader know the actual execution price.

The Hidden Culprits: Hardware and Local Infrastructure

Retail traders are quick to compare spreads and commissions, but many of us are oddly casual about the machines we use to place orders. That is backwards, since a weak local setup can damage execution before the broker ever sees the order. Local improvisation can feel boring, but it is often worthwhile.

Many small improvements can add up. Use a wired Ethernet connection instead of WiFi, strip the machine down to what is needed for trading, disable unnecessary startup tasks, and avoid mixing entertainment, office work, and live execution on the same device. Keep the operating system healthy through required updates, but schedule them well, and do not let it surprise you during active market hours.

A lot of slippage blamed on “broker tricks”, actually begins closer to home. Not all of it, but enough that any serious trader should rule it out before shouting fraud.

Computer

If you are serious about reducing slippage, start with the computer. An old processor, insufficient RAM, a busy disk, thermal throttling, or a bloated operating system can all delay how fast the terminal reacts and how fast it hands off the order. This is rarely a dramatic delay, but it does not need to be to make a difference in fast-paced trading. If a local platform freezes for half a second during a market event, it can make a huge difference, and even smaller interruptions matter in super-fast markets.

The issue is not just speed in the benchmark sense; we need to look at consistency. Traders need a predictable system response. A machine that handles normal use well but spikes in CPU load when antivirus scans, sync tools, browser processes, charting software, and trading terminals all compete at once is not a stable execution machine.

Many small-scale traders do not have a dedicated trading computer but are still electing to use super fast-paced trading strategies, entering their orders into the MT5 platform they installed on a multitasking office laptop.

Activity Hygiene

Background software matters more than most traders like to admit. Operating system updates, cloud sync clients, messaging apps, browser tabs with live content, streaming services, backup tasks, and even ad-heavy web pages can compete for system resources.

None of them feels serious on its own, but together they create noise, and noise in a trading setup means delay variance. The result can be a wider spread between the price you saw and the price that can still be filled when the order lands.

Internet Connection

WiFi is convenient, but convenience and execution quality are not the same thing. Wireless links are vulnerable to interference, signal degradation, contention with other devices, and retransmissions. The result is not always a slower speed, but the risk of jitter and packet loss is increased, and that is often worse. For trading, stable latency is important.

The home router can be another weak point. Consumer routers are built to handle mixed traffic, not latency-sensitive order flow. When someone in the house starts a video call, backs up files to the cloud, or streams 4K video, the router has to queue packets. Your order joins the queue like everything else, and the market does not pause to let it catch up.

Understanding Intermediaries and Global Routing

Once an order leaves the trader’s premises, it enters a part of the chain many retail users do not fully understand. This is where routing quality, data center geography, peering, and specialist infrastructure providers begin to shape execution. Not all internet paths are equal, and an ISP might not have a direct, clean path to the broker’s hosting environment. You might know where the broker’s main server sits (e.g. in a major financial data center such as London or New York), but you do not know the exact route chosen by the network, and your package might be passing through several intermediary systems before getting to its destination. When trading, every extra hop is another chance for congestion, rerouting, or variance.

Peering is a large part of this. Networks exchange traffic with each other through commercial and technical relationships. If your ISP peers well with the upstream carriers that have efficient routes into the broker’s hosting environment, latency may be decent. If not, the path can be clumsy. Two traders in the same city using different ISPs can see very different performance to the same broker server for this reason alone. That difference may not be visible on a generic internet speed test, but trading traffic is more sensitive than that.

Geography adds another hard limit. Data does not teleport, and even in fiber, distance costs time. A trader manually executing from one continent into a server on another is accepting more baseline latency than a trader hosted near that server. In calm markets, it may not matter much. In fast markets, it absolutely can, and that can make it a real consideration for active trading strategies like day trading. This is why location choices for servers, ISPs, VPS providers, and brokers all matter together. Traders who optimize only one piece of the path and ignore the rest often see disappointing results.

Between the broker server and the final liquidity source, there is often another specialist layer, the bridge or aggregation technology provider. In many FX and CFD setups, software firms provide the infrastructure that connects client-facing platforms such as MT4 or MT5 to external liquidity providers. That bridge can aggregate quotes, apply routing logic, manage risk rules, and transmit the order onward.

The trader does not see this layer directly, but it can shape how fast the order moves and how the broker sources liquidity. This is an important distinction because some complaints vaguely aimed at the broker are really complaints about the broker’s overall stack. The front end may look simple. The back end might involve the trading platform server, a bridge, an aggregator, one or more liquidity providers, internal risk rules, and venue-specific logic. That is not a defence of bad execution, but if you want to understand why and how delay is occurring, you need to understand that there are several places where it can occur.

Professional trading firms spend a lot of money and effort to “pave the road” for their own trading packages. They rent servers in financial data centers, buy cross-connects, and shorten the physical and logical path between strategy and execution venue. A cross-connect is not marketing fluff; it is a physical link inside or between facilities that reduces the number of external network segments between systems. Fewer segments usually mean less latency and less variance. For high-frequency firms, this is old news, but many novice hobby traders do not know that institutional traders treat network design like part of the trading edge.

Broker Execution Models and Liquidity

Talking about slippage makes no sense without execution model and liquidity context. For traders, the practical lesson is blunt. Slippage can be caused by several different issues, including technology issues, broker issues, and liquidity issues. You cannot solve a liquidity problem with a better internet connection, and you cannot solve a hardware problem by picking another brokerage company.

MM/DD Brokers, STP brokers, ECN brokers, and DMA

Execution model matters because not all brokers handle the incoming order in the same way. In a straight-through processing or ECN-style setup, the order is generally passed into external liquidity with minimal dealing desk intervention. That can improve transparency around market based slippage, though it does not eliminate it.

True market-based routing can even make slippage more visible because the system is exposing the trader to real conditions rather than smoothing them away. In a market maker model, the broker can internalize flow and take the other side of the trade, hedge selectively, and manage exposure across the book. That does not automatically mean worse execution, and many market makers can provide fast fills in normal conditions because they control more of the internal process.

But the incentives are different, and the trader needs to understand that. A market maker broker can choose how aggressively they internalize, when to hedge, and how to handle price changes during the life of the order request. That is why execution policy disclosures matter so much.

The idealized and over-simplified broker type recommendation sometimes sounds roughly like this: ECN is good, market maker is bad, STP is a compromise. However, reality is less tidy. A badly configured ECN route with weak liquidity can produce awful fills. A well-run and reputable market maker with deep internal flow and disciplined risk management can produce good fills in routine conditions. There are many situations where a trader will pick an STP broker even when ECN alternatives are attainable.

In the section below, we will take a better look at MM/DD brokers, STP brokers, ECN brokers, and Direct Market Access (DMA), and how these models differ from each other.

Order Handling Methods: Market Execution vs. Instant Execution

With market execution, the order is filled at the best available price when it reaches the execution point. That means the requested price is not a guarantee. The market can move, and the fill can be better or worse. That is the cleanest framework for understanding slippage because it accepts price movement as part of the process.

Instant execution works differently. The trader requests a quoted price, and if that price is no longer available, the broker may return a requote instead of filling at the changed price. Traders sometimes think this protects them from slippage. In one narrow sense it can. In a broader practical sense, a requote is often just a delayed refusal to trade at the original price. The market has moved, and now the trader must accept a new price or miss the trade. In a fast move, that can be worse than transparent slippage because the second decision comes after the market has already shifted.

The trading platform documentation can tell you about the existence of maximum acceptable price deviation settings in order placement, which is the platform level way of defining how much movement can be tolerated before the order handling changes.

Liquidity Depth

A lot of trader anger about slippage comes from confusing price display with executable liquidity. They are related, but they are not the same thing. Quotes invite but liquidity decides. If your order size is too large for the available depth at the time you trade, slippage is expected behavior.

Inexperienced traders who see a quote often assume there is unlimited size available there. In reality, the displayed best bid and ask represent the top of the market, not the whole market. If you try to buy a size larger than the liquidity available at the best ask, the order must consume liquidity at worse price levels. The final fill becomes a weighted result of what was available.

Last Look

The last look feature means that a liquidity provider that your broker relies on, e.g. a bank or large trading firm, gets a tiny window, typically just a few milliseconds, to decide if they still want to fill the trade at that price. They will accept or reject the trade, and for you, this flexibility can show up as requotes, rejected orders, and slippage (good and bad).

Some brokers pass orders to liquidity providers that have “last look” privilege, while other brokers use “no last look” providers, and this is one of many reasons why execution can behave differently with different brokers.

For a liquidity provider, the last look feature is about protection. Markets move extremely fast, and without that last look, the provider can get “picked off” by traders (or algorithms) hitting stale prices before they update. Providers can use that last look to filter toxic or high-frequency flow, manage risk in fast markets, and avoid filling trades at outdated prices.

If you experience partial fills, it can be because your order was split between multiple liquidity providers, and each provider independently decided whether to accept or reject their portion. (Although this is just one of several factors that can result in a partial fill.) There can also be delays happening as the system tries other providers after a rejection.

Example:

You place a large buy order.

- Provider A accepts part of it.

- Provider B rejects it.

- Provider C accepts the rest at a slightly worse price.

As a result, you get a partial fill, at least two different prices, and possibly a small delay.

Is last look exclusive to forex trading?

No, last look isn’t exclusive to forex trading, but that’s where it’s most common and most talked about. Foreign exchange is largely an OTC (over-the-counter) market, meaning there’s no single centralized exchange. Prices come from different banks and liquidity providers, and because of that structure, quotes are often indicative (not fully firm), and liquidity providers use last look to protect themselves before committing.

Last look exists even outside of forex, but that is less common. When requotes and order rejections show up on retail platforms for CFD trading and spread betting, last look can be a factor. We also see last look in certain OTC bond and derivatives markets. Conceptually, request-for-quote (RFQ) systems are very similar to last look, even though the two are structured differently.

MM/DD brokers, STP brokers, ECN brokers, DMA, and Hybrids

| Model | Execution Control for the Broker | Slippage Type | Broker Incentive |

|---|---|---|---|

| MM/DD | High | Managed / filtered | Profit from spread + client losses |

| STP | Medium | Market-based | Spread markup and/or commission |

| ECN | Low | True market slippage | Commission |

| DMA | Very low | Pure market slippage | Commission and/or access |

1. Market Maker / Dealing Desk (MM/DD) Brokers

A Market Maker (MM) broker, also known as a Dealing Desk (DD) broker, internalizes client trades. This means the broker itself becomes the counterparty to the client’s position rather than sending the order to the external market.

When you place an order, it is typically filled within the broker’s own system. Prices are derived from external markets, but the broker can set its own bid/ask spread, decide how orders are matched internally, and choose whether or not to hedge exposure externally.

Execution is often instant or near-instant, especially in calm markets, because no external routing is required.

Slippage characteristics with an MM/DD broker:

- Slippage can be controlled or filtered by the broker

- Slippage may not reflect true market depth, since trades are internalized

- Some brokers may offer fixed spreads or limited slippage in normal conditions

- In fast markets, execution may involve requotes (order rejected, new price offered) and delayed fills

- In extreme volatility, a broker may widen spreads significantly rather than pass through raw slippage.

With this broker model, the broker can earn from client losses and spreads. Many of these brokers offer commission-free trading and low first deposit requirements, which makes them appealing to new retail traders. The broker controls the execution environment. Execution quality depends heavily on broker integrity and applicable regulations. There is a built-in conflict of interest present when a broker profits from trader losses, and this conflict must be managed responsibly.

2. Straight Through Processing (STP) Brokers

An STP broker routes client orders directly to external liquidity providers (LPs), such as banks or larger brokers. There is no dealing desk intervention.

A typical STP broker will aggregate quotes from different providers, and your order is filled at the best available price among them. Execution is usually market-based, meaning no requotes, but fills depend on available liquidity. Unlike MM/DD brokers, STP brokers generally do not “smooth” execution.

Slippage characteristics with an STP broker:

- Slippage is real and market-driven

- Slippage can be positive or negative

- Compared to the MM/DD broker, the STP broker has less control over execution quality. The STP broker relies on the liquidity providers’ pricing and fills.

The STP broker is not your counterpart in your trades, so that conflict of interest does not exist. STP brokers typically make most of their money from spreads and commissions.

3. Electronic Communication Network (ECN) Brokers

An ECN broker connects traders directly into a shared liquidity pool where multiple participants interact. The liquidity pool is usually made up of a mix of participant types, each contributing quotes (bids/offers) or consuming liquidity. The exact mix varies by broker and venue, but the most common groups are tier-1 banks (primary liquidity providers), non-bank liquidity providers (market-making firms), prime brokers, prime-of-prime firms, hedge funds and asset managers, proprietary trading firms (prop firms), high-frequency trading firms, and sometimes also other retail brokers (they tend to be liquidity takers).

When you use an ECN broker, orders are matched within a centralized order book and participants can see the depth of market (DOM). Trades are executed based on available bids and offers.

Execution is typically fully market-driven, anonymous, and based on real-time liquidity.

Slippage characteristics with an ECN broker:

- Slippage reflects true order book conditions

- Partial fills are common. (Large orders may be split across price levels.)

- Both positive and negative slippage occur naturally.

- During volatility, liquidity can disappear temporarily and prices can gap through levels.

- There are no requotes, only what the market provides.

The transparency of the ECN broker model appeals to more advanced traders. The broker truly acts as a connector. ECN brokers tend to earn the bulk of their money from commissions. Since their target group is advanced traders, ECN brokers rarely offer the type of hand-holding that benefits novice traders. The infrastructure is more complex, and the broker does not control pricing and execution. The exact quality of the trading experience will depend a lot on the broker’s liquidity relationships.

4. DMA (Direct Market Access)

Direct Market Access (DMA) is similar to the ECN model but emphasizes direct interaction with underlying market venues, such as exchanges or institutional liquidity pools.

Orders are sent directly to external venues (e.g., an exchange or liquidity providers), and the trader effectively accesses the same pricing stream as institutional participants. DMA is especially common for equity trading, futures trading, and certain advanced forex setups. Execution is fully transparent and market-driven.

Slippage characteristics with a DMA:

- Slippage is entirely dependent on market liquidity

- The broker does not intervene or filter

- Partial fills are common

- Order book sweeping for large trades is common

- During fast markets, significant slippage can occur as gaps are passed through directly

DMA appeals to professional traders and advanced retail traders, as it provides institutional-grade access. The model requires sophisticated infrastructure. Just as with ECN, the rules will not cater to small-scale hobby traders. Expect a large first deposit to be mandatory. The broker earns money from commissions and access fees. The broker has minimal control over execution outcomes.

5. Hybrid Brokers (B-Book / A-Book Mix)

Many modern retail brokers don’t fit neatly into a single category like pure Market Maker or pure STP. Instead, they operate a hybrid model, often referred to as B-book / A-book routing. This setup allows the broker to dynamically decide how each trade is handled, balancing profitability, risk, and execution quality.

- A-book: The broker routes the trade externally to liquidity providers

- B-book: The broker internalizes the trade, acting as the counterparty

A hybrid broker uses both simultaneously, choosing on a per-trade or per-client basis. When you place an order, the broker’s system can evaluate factors such as trade size, instrument, market conditions, and client profile (e.g., profitability, strategy, latency sensitivity). Based on this, the order is either kept in-house (B-book) and filled internally or sent to liquidity providers (A-book) and executed in the external market. This decision is typically made in milliseconds by risk engines, not manually.

Slippage characteristics:

- A-book side (external routing) will have slippage that reflects real market conditions. Slippage can be both positive and negative. Partial fills are common. Expect liquidity-driven price gaps, especially during stormy periods.

- B-book side (internalization) can have slippage that is smoothed or controlled by the broker. The broker can, for instance. reduce extreme negative slippage, limit positive slippage, and widen spreads during volatility. Execution may feel more stable in normal conditions.

If you are using a hybrid broker, you might experience clean, stable fills on some trades and then sudden slippage or different behavior on others. That can be the result of the broker switching between B-book and A-book execution paths. Generally speaking, hybrid brokers tend to lean more toward internalization in calm market conditions and do more external routing in stormy conditions. This flexibility helps brokers survive tail-risk events, especially under frameworks with mandatory Negative Balance Protection (NBP).

From a trader’s perspective, hybrid execution can feel unpredictable. You may get minimal slippage in one trade (internalized) and then significant slippage in another (externally routed). You usually don’t know whether your trade was B-booked or A-booked, nor will you know when or why routing decisions change.

Despite the downsides, many inexperienced retail traders do well with a hybrid broker, since they benefit from the balance between execution quality and business viability. Many hybrid brokers cater strongly to small-scale hobby traders and offer beginner-friendly conditions, tight spreads, fast execution, and low first deposits. A pure ECN or DMA model is often too expensive or complex for mass retail clients, while a pure Market Maker model carries too much concentrated risk. A hybrid broker is essentially a dynamic execution system that switches between internal and external liquidity depending on risk and opportunity.

Market Conditions: The External Triggers

Even a strong setup runs into the market itself, and the market can be violent. The unpleasant truth is that some slippage is not fixable because it reflects a real market change between intention and execution. No internet tweak changes the fact that the market moved. What traders can control is their willingness to trade in conditions where that movement will be more violent than normal, such as major releases and session opens, to trade in thin liquidity windows, to place oversized orders, and to engage in reactive clicking after the move has already started. So many execution horror stories begin with one sentence: “I knew it was volatile, but I took it anyway.” Fair enough. Just do not act surprised when volatility behaves like volatility.

In this context, I would like to point out that a stop-loss order is not a price guarantee. A stop-loss order is simply an instruction to create a market order when the trigger is hit. If liquidity is poor or price jumps through the level, the fill can land far away from the stop point.

Breakout entries also deserve a warning. Traders love breakouts because they appear decisive. The trouble is that the order is often sent precisely when everyone else is also hitting the market. By the time the order arrives, the best displayed price has already been consumed. In a textbook screenshot, the entry looks obvious. In live execution, the order joins a queue.

Macro Releases

A well-known example of an external trigger is the scheduled macro release. Nonfarm payrolls, CPI, central bank rate decisions, and similar events can move prices faster than retail infrastructure can process, route, and confirm an order. In those windows, the quote on the screen is often stale by the time the order arrives. Maybe only stale by fractions of a second, but that can be enough to cause problems. During sharp repricing, the market can effectively gap through levels very fast.

This is where inexperienced traders often confuse spread widening with slippage. The two are related, but they are not the same. Spread is the distance between bid and ask at a given moment. Slippage is the difference between the expected price and the execution price. A market can widen the spread without generating much slippage if your order still executes near the expected tradable quote. A market can also keep the spread looking moderate while the order slips because the available liquidity at the displayed quote vanishes before your order reaches it.

Thin Liquidity

Thin liquidity makes the problem worse. Certain sessions, especially quieter regional hours, can have less depth than headline liquidity suggests. Exotic currency pairs are the obvious example, but even major pairs can trade with lighter depth at awkward times. The market may still print prices normally, but that does not automatically mean that those prices can absorb size cleanly. When there is not much volume standing at the best levels, even modest orders can move through the book.

Session Transitions

Session transitions are another source of trouble. The open of London, the open of New York, equity cash opens, and the overlap between major sessions can produce short-lived bursts of spread widening, quote updates, and aggressive repositioning.

Market Fragmentation

Another external trigger is market fragmentation. In products with multiple venues or liquidity pools, prices can update unevenly across sources. Aggregators do their best to form a usable quote, but during stress, the quote composition itself can change rapidly, and that can create visible drift between one platform’s display and another’s fill quality. Traders then assume one feed is fake, without realizing it is just different pools repricing at different speeds.

Negative Balance Protection (NBP)

Slippage is often described as a slide from one price to another, but in extreme conditions, it is better understood as a jump. A true gap is not a smooth move through every intervening price. It is a discontinuity in available liquidity, which causes one tradable level to disappear and the next real executable level to be materially lower or higher. That distinction matters because it explains why stop losses can fail to behave the way inexperienced traders expect.

Take a simple example. Suppose a long position is protected by a stop at 1.1800, while the last meaningful market before the event traded near 1.2000. If a shock event hits and liquidity disappears, the next executable market may print at 1.1500. In technical terms, there was never a tradable market at 1.1799, 1.1750, or 1.1600 for the order to hit. The stop did trigger, but once triggered, it became a market instruction in a market that no longer existed at the expected range. The fill at 1.1500 is not a malfunction; it is a fill at the only price that was actually available.

So, the stop-loss did not “fail” per se. The stop-loss order was triggered and the position was closed. The trader is disappointed because their assumption about continuous liquidity was wrong. Markets usually feel continuous because, under normal conditions, there are enough resting bids and offers to create that impression. In a tail event, that impression disappears very quickly. The gap reveals the underlying rule: an order can only be filled when someone else is willing and able to take the other side.

This is why stop-loss orders are not enough to guarantee that positions will actually be closed at or even near that price point, and this truth can hit traders especially hard when positions are leveraged. This is also why many financial jurisdictions around the world require brokers to give retail trading accounts Negative Balance Protection (NBP). Without NBP, a trader can end up owing the broker a lot of money when the market moves against a leveraged position, and the stop-loss orders placed by the broker fail to be enough to close the positions before the account balance falls below zero.

ASIC in Australia and the FCA and the UK are two well-known examples of financial authorities that require brokers to give retail trading accounts (non-professional trading accounts) Negative Balance Protection. The same is true for all the financial authorities in the EU member states, e.g. BaFin in Germany, CySEC in Cyprus, and so on.

Negative Account Balance can not change how markets work and it will not protect you from losing money when the market gaps. It is only there to protect you from ending up in debt. Example: The market gaps from 1.2000 to 1.1500, and the trade is filled around 1.1500 because that is where liquidity reappeared. Negative balance protection does not cancel the gap and does not improve the execution price after the fact. What it does is stop the retail trader’s liability from extending beyond the funds protected by the account rules. In other words, the market event creates the loss, but the regulatory framework determines who is left carrying any part that exceeds the client’s balance.

That leads us to the broker’s burden. In a severe gap event, the broker may be unable to recover the shortfall from the retail client because of the mandatory NBP. Yet, the broker may still owe money upstream if hedges were filled at far worse levels, if liquidity providers stood firm on the execution, or if the broker had to honor client protections while receiving no matching protection from its own counterparties. The broker must absorb the difference. During ordinary conditions, that risk is manageable. During tail risk, it can break a brokerage company.

In a stormy event, each layer of the trading chain will try to protect itself. This means that the broker can hope that its liquidity provider will provide fair treatment in stressed markets, but in true dislocation, the liquidity provider will try to save its own skin. For this reason, any serious broker will put special protections in place for leveraged NBP accounts where losses can not be passed on to the trader beyond the account balance.

The Downside of NBP, From A Trader’s Perspective

Negative Balance Protection (NBP) shields the client from going into debt and shifts tail risk onto the broker. Brokers don’t just accept that risk passively; they manage it actively, and this will impact how open trader positions are treated.

Most retail brokers run either a B-book (internalizing client trades) or a hybrid/A-book (hedging some exposure with liquidity providers). In both cases, they implement broker-level risk controls on top of whatever stops you place yourself. Here are a few examples:

- Automatic margin close-out (stop-out): If your equity / margin ratio falls below a certain threshold (e.g., 50%, 30%, or even 100% depending on regulation, account type, financial products, and the broker), the platform starts closing positions automatically. This is effectively a broker-imposed stop loss based on your account health.

- Real-time liquidation engines: During fast markets, systems will close positions at the best available prices to cap further losses and protect the firm from NBP-driven deficits.

- Internal “house limits” and throttles: Brokers may reduce leverage, widen margins, or restrict new orders when volatility spikes.

For you, as a trader, it means that your position or positions can be closed before any of your own stop-loss levels have been reached. Your trade might still be above (for longs) or below (for shorts) your personal stop level, but if your margin level breaches the broker’s threshold, the platform will order liquidation anyway. Forced liquidations in thin liquidity can mean large slippage and you may end up closed at unfavorable prices. Even if your thesis is long-term and you’re willing to sit through volatility, the system won’t allow it once risk limits are breached. Tight margin requirements and automatic liquidation can invalidate strategies that rely on wider stops or temporary drawdowns.

When your account has NBP, the broker is on the hook if your account goes negative, so the broker’s systems will be designed to prevent that scenario from happening. In other words, NBP removes your ability to choose holding over protection. You’re protected from ending up owing money, but you lose the ability to hold through extreme volatility if it threatens your margin. You can not decide to “ride out the storm” and wait for the market to stabilize.

Professional Trading Accounts

In many jurisdictions, the legal reality changes sharply once the client has been formally classified as a professional trader. Retail protection is built around the assumption that a non-professional client needs a hard liability cap. Professional clients are not viewed with the same eyes by the regulators, and even when NBP is available for professional trading accounts, many pro traders elect to waive that protection because they dislike the downsides.

Without NBP, the gap mechanics remain the same, but the allocation of loss is different. A professional client can be left with a negative account balance that remains legally collectable, depending on the account terms and local framework. Same gap, same slippage, same market physics, but a different legal aftermath. That distinction changes how tail risk should be thought about. Retail traders under protected regimes still face execution risk, stop loss failure in gaps, and sudden account wipeouts, but the secondary disaster of owing money after the account is gone. Professional clients typically work without that shield and can end up in the red.

Slippage Mitigation Strategies for Traders

Slippage cannot be abolished, but it can be managed. Examples of common risk management strategies are order selection, platform configuration, timing, and sizing. As discussed above, we can also improve the hardware and software infrastructure to the best of our ability, and use tools such as a Virtual Private Network (VPN) or Virtual Private Server (VPS).

Record keeping and regular evaluations are also essential to make sure you know how your setup works when it comes to slippage and find out quickly if something needs to be altered.

Order Selection

Limit orders

Limit orders are one of the cleanest tools against paying worse than a chosen entry or exit price. A buy limit will only execute at the limit price or better. A sell limit works the same way in the other direction. The downside of using a limit order is obvious: the market may never trade there in executable size, and the order may not fill at all. You need to decide if you are willing to do that trade-off and exchange fill certainty for price certainty. Your order is less likely to fill, but can only fill at your selected point or better.

Stop Limit Structures

Stop limit structures can be useful too, especially for traders who want to define a worst acceptable entry after a trigger. A stop-limit order is a two-step mechanism:

- Stop (trigger price): This is the level that activates the order. Nothing happens until the market reaches this price.

- Limit (execution price): Once triggered, the order becomes a limit order, meaning it will only execute at your specified price or better.

This structure is useful when you want to avoid slippage, but it comes with a trade-off. Unlike a stop-market order (which prioritizes execution), a stop-limit order prioritizes price control. That means that if the market moves quickly past your limit price after triggering, your order may not get filled at all.

Traders use stop-limit structures to define a worst acceptable entry or exit. It can be useful in breakout strategies where you don’t want to chase price too far beyond the trigger, and it can also help a trader maintain price discipline in fast markets.

Example: You have an open long position. You want to cut losses if the price drops, but you don’t want to sell too cheaply. You place a stop price at 1.2000 and a limit price at 1.1990. If the price falls to 1.2000, the order is triggered, and a sell limit order is placed for 1.1990. You will only exit at 1.1990 or better.

You might get lucky and see your order fill, but there is no guarantee that this will happen. If the price gaps straight to 1.1950, your limit (1.1990) is skipped, and the position is not closed. What you are saying with this type of order is: “If the market turns against me and hits 1.2000, I want out, but I refuse to sell below 1.1990. I´ll rather keep the position open than sell below 1.1990.”

Stop Market Order

A stop-market order is the simpler (and more aggressive) cousin of a stop-limit. It’s an order that triggers at a specific price (the stop) and becomes a market order, meaning it executes immediately at the best available price.

It is possible for the market order to be split up and result in partial fills at different prices, because a market order will “eat through” available liquidity.

Traders typically use a stop market order to enter fast-moving markets (breakouts, news) and to exit trades reliably (but with no fixed price). With a stop market order, there is a high probability of execution, but the fill price or prices are uncertain.

- Stop-market: “Get me in/out no matter what.”

- Stop-limit: “Get me in/out, but only at this price or better.”

Platform Configuration

Another example of a useful tool is platform configuration. On some platforms, deviation settings let the trader define the maximum acceptable price difference in relevant order handling contexts. That will not magically improve the market, but it will tell the platform how much movement is tolerable before the trade is handled. Traders should understand that a strict deviation setting may reduce bad fills but increase rejected or missed trades. A loose setting may secure participation, but at weaker prices. There is no free lunch, just a policy choice.

Timing

The third tool is timing. Avoiding the first few minutes around major scheduled releases, session opens, and liquidity transitions removes a large share of avoidable slippage. Many traders act as if every move must be caught from the first tick. That is ego talking. A trade taken after the first burst often has a worse headline price but better actual execution quality and more reliable market structure.

Sizing

Order size matters too. Traders should think in terms of market capacity, not just personal conviction and ability. If the instrument is thin, splitting entries or reducing size can materially improve average execution.

Networking Solutions: VPNs and VPS

When traders start to care about execution, they eventually run into two common ideas: use a VPN or use a VPS. These are not interchangeable, and for most situations, one tends to be more useful than the other.

A Virtual Private Network (VPN) changes the route your traffic takes by tunneling it through another server first. In some cases, this can be helpful to reduce slippage. If your ISP has poor routing to the broker’s infrastructure, a low-latency VPN endpoint in a better-connected location may improve the path. The order effectively takes a detour that turns out to be cleaner than the default road. This is possible, and in some setups it works. But most VPNs do not reduce latency. VPNs add encryption overhead, extra distance, and one more stop, and this can actually harm execution. VPNs can be great for privacy, but that is not the same thing as quick execution, and traders should be very skeptical of generic claims that a VPN reduces slippage. At best, a carefully chosen low-latency route can reduce a bad routing problem. At worst, the trader adds more delay and congratulates themself for being secure while the fills get worse.

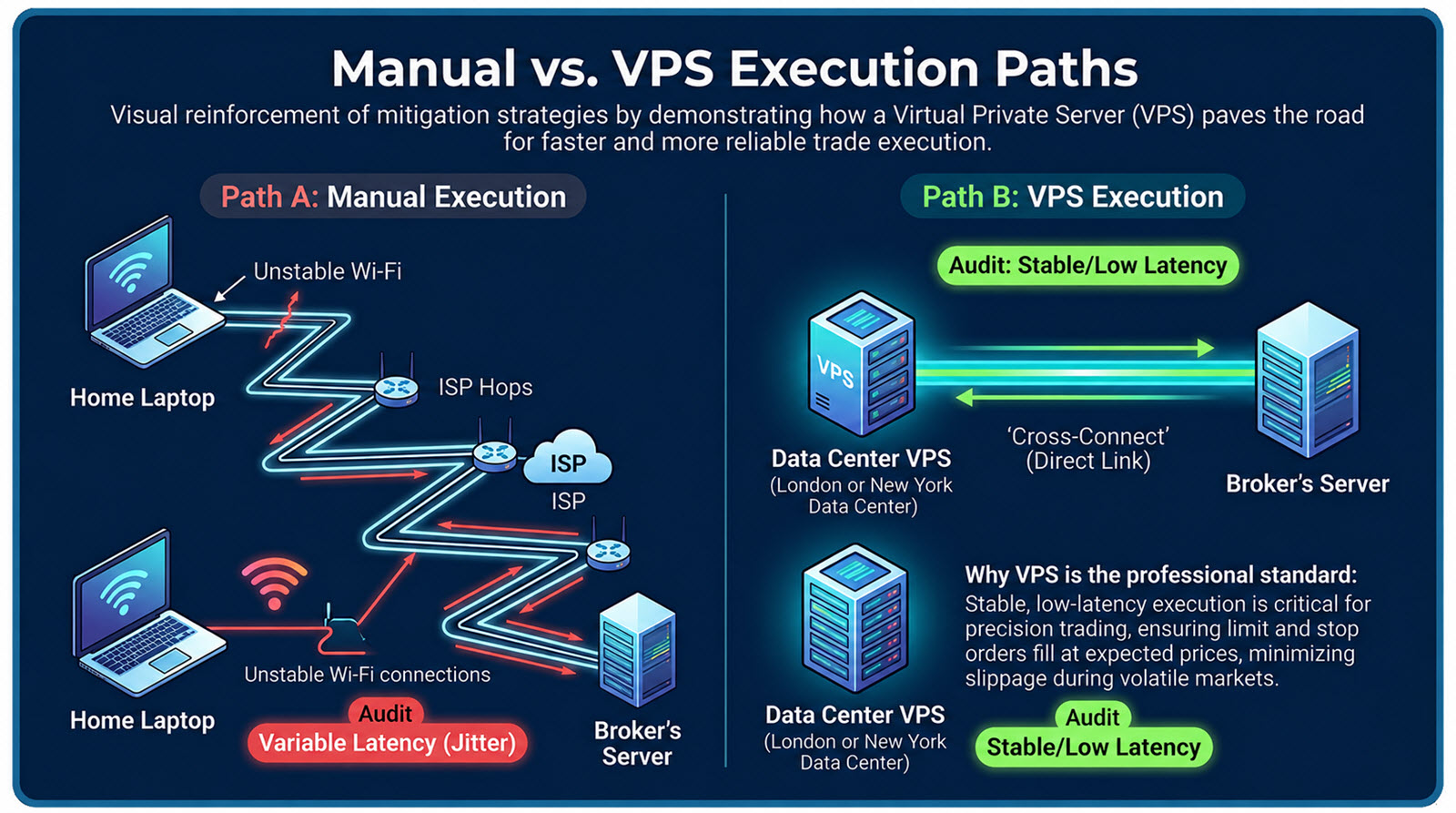

A Virtual Private Server (VPS) is different. A virtual private server places the trading platform itself in a remote data center, often much closer to the broker’s server. That matters because it removes the trader’s local machine and local connection from the critical execution path, provided you are using pre-entered orders. (If not, the order still needs to run from your home computer to the trading platform in the heat of the moment.) If the terminal is running in the same city, or even the same facility region, as the broker’s trading infrastructure, the baseline latency can drop sharply and, just as important, become more stable.

This is why VPS hosting is standard for serious automated traders and common among serious manual traders. It does not eliminate slippage caused by market movement or shallow liquidity, but it does eliminate a large share of slippage caused by local hardware, home internet inconsistency, and long geographic distance between trader and broker.

While a VPS can play an important role in reducing slippage and improving execution consistency, its benefits are often misunderstood. The key distinction is not simply “faster internet” but where and when the order decision is executed relative to the broker’s server.

To understand this, it helps to separate retail trading into two modes: manual, real-time execution from a home computer, and pre-placed orders or automated execution.

When a trader places an order manually from a home computer, the execution path includes several steps before it even reaches the Internet Service Provider’s first hub. Your request is processed within your computer, travels from the local device through your home internet connection, moves across various network nodes, and finally reaches the broker’s trading server. Even in optimal conditions, this introduces latency. More importantly, that latency is variable due to Wi-Fi fluctuations, ISP congestion, background applications suddenly making your computer slower, routing inefficiencies, and more.

A VPS changes this structure by relocating the trading platform itself into a data center that is physically and network-proximally closer to the broker’s infrastructure. Instead of the execution path originating from a home computer, the trading platform runs continuously on the VPS. This means the critical execution path becomes VPS → broker server, often within the same data center ecosystem or at least within the same metropolitan network hub. The result is lower latency and, just as importantly, far more stable latency. Stability matters because slippage is not only about speed but also about predictability.

Of course, if you want to frantically punch in your orders manually on your home computer in the heat of the moment, having a VPS makes less sense, because you are not cutting out the path from your computer to the VPS. Traders who use a VPS typically rely on pre-placing their orders (such as stop, limit, or stop-market orders) far in advance or using automated trading systems (e.g. algo trading). Once the orders are set, they no longer depend on the trader’s home computer and internet connection. The VPS continuously monitors price feeds and sends execution instructions immediately when conditions are met. A pre-placed order on a VPS can be triggered and transmitted to the broker within milliseconds of price conditions being met, without waiting for the trader to react or for a home connection to transmit the request. In fast markets, this reduction in reaction delay can help ensure that orders are submitted closer to the intended price level, reducing the gap between expected and actual fills.

However, it is important to be precise: a VPS does not eliminate slippage, nor does it guarantee better fills. Slippage still depends heavily on liquidity and broker execution models. What a VPS improves is timing consistency and speed of order transmission, which indirectly helps reduce avoidable slippage caused by factors such as a slow home computer or unstable connectivity.

Used properly, a VPS does not turn a mediocre broker into a great one, but it can remove local issues, and that alone makes it worth considering. But using a VPS costs money, and not every VPS is good. Cheap hosts can oversubscribe resources, produce noisy neighbor problems, and deliver unstable performance. The phrase “hosted near the broker” matters less if the actual virtual machine is slow and inconsistent. Traders should test latency and stability before considering any longer-term commitment.

Record Keeping

Record keeping will not reduce slippage in itself, but it is necessary to monitor slippage and evaluate your setup. Traders should log the requested price, executed price, timestamp, symbol, order size, platform ping, market condition, and whether the trade occurred during news or session change.

Once you have enough samples, patterns appear. Some symbols slip more. Some hours are cleaner. Some brokers behave better under stress than others. Without records, every bad fill can feel like “bad luck”. With records, it becomes data, and you can pinpoint the weak points.

This is an important activity, even if it feels tedious, and contributes to a wider secure trading environment.

Legal and Regulatory Perspective

Execution quality is not just a technical matte; it is also a regulatory one. Above, we have already discussed slippage, stop-loss orders and how many financial authorities have made negative account protection mandatory for retail accounts, but that is definitely the only spot where a discussion about slippage runs into legal territory. In many jurisdictions, trader protection rules are in place to ensure firms take sufficient steps to provide high-quality execution.

Within the European Union, the Markets in Financial Instruments Directive II (MiFID II) contains rules regarding best execution obligations. MiFID II is a major piece of financial regulation in the European Union that governs how investment services are provided across financial markets. When it came into force in January 2018, it significantly tightened rules on transparency, investor protection, and market structure within the EU. Under MiFID II, firms are required to take sufficient steps to obtain the best possible result for clients while considering factors such as price, costs, speed, likelihood of execution, and settlement. More exact details about what constitutes “sufficient steps” under MiFID II are found in materials published by the European Securities and Markets Authority (ESMA). For more information, a good starting point is ESMA’s 2025 final report on order execution policies, which discusses Article 27 of MiFID II and the obligation for firms to describe the processes they use to achieve best execution.

In Australia, the Australian Securities and Investments Commission (ASIC) guidance under the market integrity rules states that the best execution obligation applies from the moment an order is received through to settlement, and that participants must take reasonable steps to obtain the best outcome for the client. ASIC’s guidance also stresses the value of accurate and complete records of order handling and execution decisions for monitoring and compliance.

These are just two examples from different parts of the world, and it is important to understand that the rules can differ from one country to the next. For traders in countries where best execution obligations are strong, the useful takeaway is not that regulators will save them from every bad fill (they will not), but that regulated firms are required to maintain transparent execution policies, handle orders under defined standards, and keep records. When a trader suspects abnormal execution, they can contact the broker or the applicable financial authority and file a report. A broker should be able to provide execution logs, server-side timestamps, order receipt time, routing details if available, and confirmation of the execution policy that applied to the order. The answer may still be unsatisfying, but at least the discussion moves from emotion to traceable events. If a broker cannot explain how it handled the order, or refuses to provide meaningful records, that is also telling you something, and escalating to the financial authority or ombudsman is the next recommended step.