Offshore Brokers and Leverage: Benefits, Structural Risks, and Practical Controls

Using the term “offshore broker” opens up to misunderstandings and confusion because the term can mean several different things. Some people say offshore broker when they mean any broker that is lightly regulated and/or lightly supervised. Some people include brokers based in countries where financial services firms are strictly regulated and supervised, but where the lawmakers do not impose the same retail trader guardrails that we see in countries such as the UK, e.g. mandatory leverage caps. Some use the term offshore broker to mean any broker outside of the trader’s own country, i.e. synonymous with foreign broker. Some people assume any “offshore broker” is also a sketchy broker or outright scam. Some would consider a Belize broker that accepts a Belgian trader an offshore broker, but never call a U.S. broker that accepts a Belgian trader an offshore broker, even though the Belgian trader will be devoid of mandatory negative balance protection (NBP) in both cases. When you hear the term offshore broker, it is therefore important to clarify exactly what the speaker means to avoid misunderstandings.

In the specific context of leverage trading, the idea of the offshore broker often boils down to a broker that:

- Is based in a country where brokers are lightly regulated and not legally required to treat retail traders differently from professional traders when it comes to things such as leverage caps and negative account balance protection, and

- Accepts retail traders from countries where stricter requirements exist.

In other words, offshore usually means a broker entity incorporated and licensed outside the trader’s local high oversight regime, often in a jurisdiction designed to attract international financial services business. The products are often CFDs, rolling spot forex, indices, commodities (including metals), cryptocurrency derivatives, and synthetic baskets.

In addition to higher leverage, many of these offshore brokers also offer faster onboarding, more flexible trading conditions, and access to products and markets that the trader’s home country has restricted. In exchange, the trader gives up a lot of guardrails, e.g. mandatory negative balance protection for retail traders. There is also increased counterparty risk when you pick a broker knowing it is loosely regulated and not really supervised, and this risk is present for both retail and professional traders.

It is important to remember that traders do not always go offshore because they are naive. Yes, inexperienced traders are frequently lured in by flashy welcome bonus offers, the $5 minimum deposit, and the promise of 1:500 leverage. But there are also experienced traders who deliberately choose offshore entities due to factors such as capital efficiency, better API access, cryptocurrency derivative exposure, or account separation. The trader gains flexibility and is knowingly giving up statutory compensation, independent dispute resolution, strict client money segregation rules, mandatory negative balance protection, and strong broker conduct supervision.

Instead of simply asking “Are offshore brokers bad?” and expecting a clean answer, a retail trader in a Tier 1 jurisdiction needs to ask a series of more complex questions, including these:

- What legal and operational protections disappear or get weaker when I use a Tier 3 offshore broker instead of a Tier 1 broker based in my home country?

- Are the upsides worth the downsides in my particular situation?

- And how should these new conditions change factors such as deposit size, position risk, and maximum account balance?

Offshore brokers are not inherently flawed; for sophisticated strategies, a high-leverage account can be an optimal tool. However, these entities operate without the systemic retail safety nets of Tier 1 regimes. This shifts the burden of risk mitigation entirely onto the individual.While Tier 1 brokers are fundamentally structured to protect beginners from asymmetric market hazards, going offshore demands an advanced operational baseline and absolute accountability from the trader.

Offshore brokers exist because traders want the flexibility that Tier 1 retail regimes often restrict. Higher leverage, cryptocurrency derivatives, faster onboarding, open API infrastructure, and tactical account separation are real commercial benefits. For some traders, those benefits are useful, and they make an informed decision to open an offshore brokerage account.

For many inexperienced traders, the decision is much more impulsive, and might even be based on the encouraging words of a paid TikTok star or YouTube finfluencer. They jump into the world of offshore trading without understanding exactly what they are giving up when it comes to trader protection. Suddenly, they have signed a contract with a broker where client money segregation is contractual rather than statutory. Negative balance protection applies only in normal market conditions. Dispute resolution is local, expensive, and favors the broker. Governmental investor compensation schemes do not exist. And so on.

Offshore trading is not automatically reckless, but treating a Tier 3 offshore broker as if it were a Tier 1 bank is.

The Offshore Ecosystem

The Regulatory Tier Matrix

To make it easier to discuss the regulatory landscape, analysts tend to separate regulatory quality into structural tiers. Of course, this is a blunt classification, and it is always possible to argue the specifics. Typically, where a jurisdiction falls within this tier system is based on a combination of factors such as actual enforcement capacity, client money rules, capital standards, complaint routes, product intervention powers, and how painful it is for a broker to misbehave under the applicable financial authority. In short, it is both about what the rulebook looks like and how well those rules are actually enforced.

| Tier Classification | Core Characteristics | Key Jurisdictions & Regulators | Retail Safeguards |

|---|---|---|---|

| Tier 1 | Strict statutory oversight; active enforcement; accessible consumer recourse channels. | UK (FCA), Australia (ASIC), US (CFTC), EU (CySEC/BaFin), Japan (FSA), Hong Kong (SFC) | Mandatory NBP, strict leverage caps, independent ombudsman (e.g., FOS/AFCA), statutory fund compensation. |

| Tier 2 | Reputable oversight frameworks; balanced approach to retail restrictions. | South Africa (FSCA), UAE (DIFC), India (SEBI) | Flexible leverage limits, robust AML/KYC, standard corporate segregation. |

| Tier 3 | Light-touch supervision; often functions primarily as international business registration hubs. | Seychelles (FSA), Mauritius (FSC), Vanuatu (VFSC), Bahamas (SCB), St. Vincent (FSA SVG) | Discretionary/Conditional NBP, contractual segregation only, local/expensive legal recourse. |

A Tier 1 regulatory footprint does not automatically guarantee superior corporate integrity or operational reliability compared to a Tier 3 entity. However, selecting a Tier 1 broker contractually enforces statutory safety protocols – such as state-backed insolvency funds and non-discretionary negative balance shields – that simply do not exist under Tier 3 regulatory oversight.

Tier 1 Regimes

From the perspective of trader safety, Tier 1 regimes are the ones where trader protection rules are both strict and actively enforced. Accessible complaint pathways should exist even for small hobby traders who find themselves in a conflict with their broker and do not have the resources to open and run a civil court case against their broker on their own.

Examples of regimes that are considered Tier 1 are the United Kingdom, Australia, and the United States. The European Union (EU) and the European Economic Area (EEA) also include a lot of Tier 1 countries, due to a combination of EU-level and national-level regulations.

Within Tier 1 regimes, there are detailed conduct rules, capital requirements, reporting duties, product intervention powers, and established enforcement systems. The UK FCA has for instance made permanent restrictions on retail CFDs in PS19/18, including leverage limits, margin close-out rules, negative balance protection, incentive restrictions, and risk warnings. In Australia, ASIC maintains retail CFD product intervention measures, including leverage caps and negative balance protection. In the European Union, ESMA enacted temporary CFD intervention rules, until the respective national authorities could enact their own national rules.

There is no universally accepted official definition of Tier 1 regulatory jurisdictions, but in retail FX and CFD discussions, the following list includes a few examples of jurisdictions that are commonly referred to as Tier 1 jurisdictions because they combine strong trader protection legislation with active enforcement, compensation mechanisms, and a generally well-functioning legal system.

- United Kingdom (FCA)

- Switzerland (FINMA)

- United States (CFTC/NFA)

- Australia (ASIC)

- Canada (CIRO and provincial regulators)

- Singapore (MAS)

- Japan (FSA)

- Many but not all of the EU/EEA countries

Tier 2 Regimes

Tier 2 regimes are not as strict as Tier 1 regimes when it comes to trader protection rules (especially retail protections) and oversight, but they are still firm and have a good reputation. Examples of places commonly considered Tier 2 are South Africa and the Dubai International Financial Centre (DIFC) in the UAE. They have well-reputed financial authorities, licensing standards, AML rules, supervisory frameworks, and enforcement resources.

Especially for retail traders, Tier 2 regimes can be appealing due to having fewer mandatory retail restrictions when it comes to leverage, product access, and bonuses/perks for retail traders.

Tier 3 Regimes

Regimes that are not Tier 1 or Tier 2 are typically lumped together in the Tier 3 category. This is a wide and heterogeneous category where regulation and enforcement vary a lot between the different jurisdictions. Some jurisdictions simply do not have much relevant regulation and supervision for retail financial trading because it is still such a rare activity there. Other countries have deliberately positioned themselves as hubs where company groups headquartered in other parts of the world register companies and subsidiaries when they want to be able to offer online retail trading under light regulation and supervision.

Examples of jurisdictions considered Tier 3 are the Seychelles (FSA), Mauritius (FSC), Vanuatu (VFSC), the Bahamas (SCB), and St. Vincent and the Grenadines (FSA SVG). All of these five examples are locations that company groups controlled from other parts of the world pick when they want to set up a brokerage company under light regulation and supervision, a practice often referred to as offshoring. There can also be significant tax benefits and privacy benefits associated with being based in one of these countries.

Some of the Tier 3 jurisdictions issue actual broker licenses and similar, or at least a general financial services license. Others are more company registration venues than actual regulators for retail trading, and if you start digging around, you will find that your “brokerage company” does not hold anything more than a general business registration.

The fact that a company is registered in a Tier 3 jurisdiction does not automatically mean that it is sketchy or a scam, but it increases the risk. It can also be much more complicated for the trader to find recourse if there is a conflict between the broker and the trader.

When A Multinational Company Group Operates Under A Global Brand

Many large brokerage and financial services groups operate a large number of companies while marketing their client-facing services under the same global brand. Within this type of structure, it is common for the group to set up companies in different countries to comply with different financial authority requirements.

That in itself is not a red flag. Many times, having a domestic presence is actually a requirement to obtain a local broker license, and setting up a local company can also make it easier to comply with other aspects of local regulation. A trader in Australia can be onboarded by the brand’s ASIC-licensed entity, a trader in the UK can be onboarded by the FCA-licensed entity, and a trader in Germany can be onboarded either by a BaFin-licensed entity or by an entity licensed by another EU/EEA financial authority, as long as passporting rules are followed.

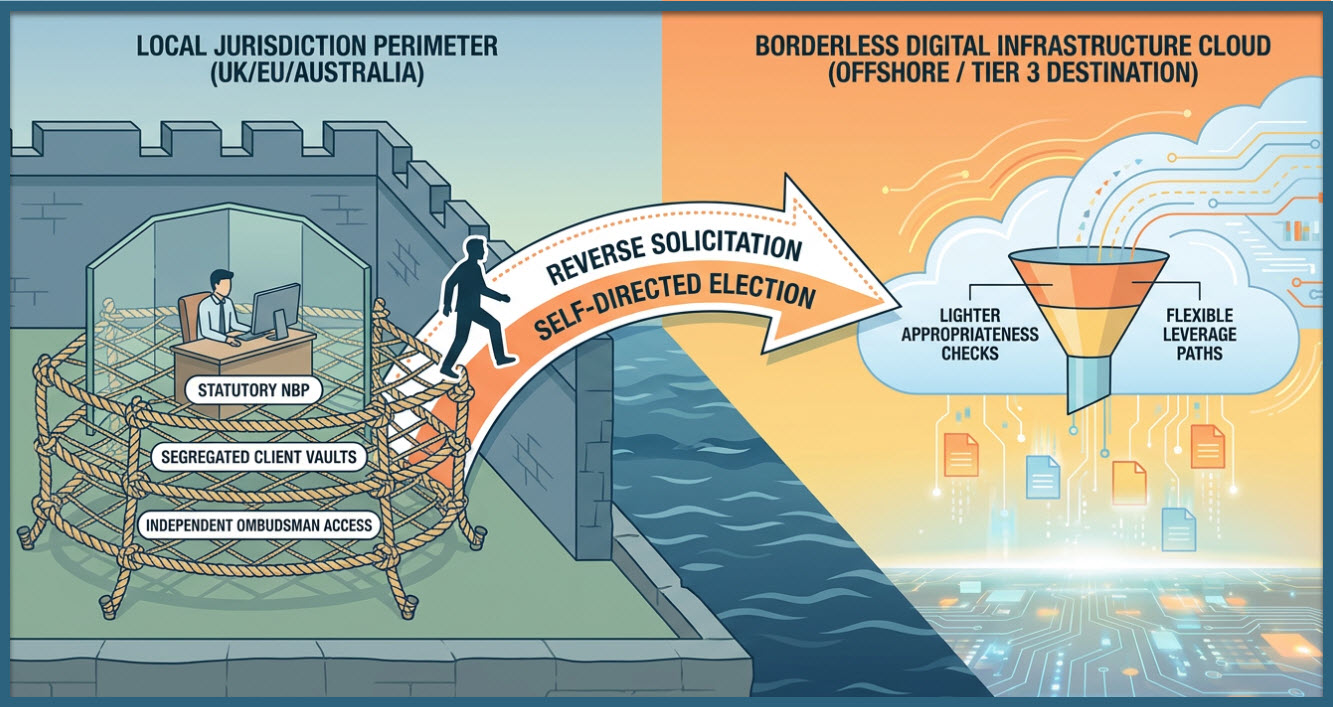

What can become a problem for traders is when a global brand heavily features one or more Tier 1 or Tier 2 licenses in their global marketing, but then discretely onboard clients through a company based in a Tier 3 jurisdiction. The brand, website design, trading app, symbol list, account portal, and customer support channels may look nearly identical across entities, while the legal reality can be entirely different depending on exactly which company you signed up with. When the different contract partner results in a different regulator, it can also mean different capital treatment, different leverage rules, different negative balance protection, and different complaint routes.

Always explicitly verify the exact legal entity underwriting your account during registration. This designation, combined with your legal nationality, dictates your actual regulatory baseline. Be acutely aware that global brands frequently route international applications away from their featured Tier 1 units and directly into light-touch Tier 3 offshore subsidiaries.

Example: The broker brand is Wonderful Broker. The company Wonderful Broker UK Ltd is based in the UK and holds an FCA-license, which is featured heavily in Wonderful Broker’s global marketing. This helps Wonderful Broker to build trust, since the UK and FCA have a great reputation when it comes to trader protection. However, only clients who live in the UK are onboarded through the Wonderful Broker UK Ltd company. The group maintains a Tier 1 licensed entity for UK clients, and for marketing purposes, but runs one or more subsidiaries for non-UK clients. Typically, these subsidiaries will be registered in Tier 3 jurisdictions, such as the Seychelles, Mauritius, Vanuatu, or the Bahamas.

Traders in the UK have Wonderful Broker UK Ltd as the contract partner printed in their user contract, while traders in places such as Latin America and Africa get a contract with Wonderful Broker SYC Ltd, which is based in the Seychelles and governed by Seychelles law. The Wonderful Broker brand can thus comply with strict local rules in the UK while offering other terms to clients outside that perimeter.

The offshore subsidiary is not necessarily a low-quality brokerage firm, and traders signed up with Wonderful Broker SYC Ltd might get access to the same trading software, customer service, educational materials, and so on. But their legal reality is different. Even if Wonderful Broker SYC Ltd is a well-functioning entity with audited accounts and group-level backing, it is still a company that operates outside the UK FCA framework.

This is one of the reasons why it is important to actually read the client agreement and find out exactly who your legal contract partner is before you sign anything. Brands such as “Wonderful Broker” will usually not outright lie; they just put UK LICENSED BROKER in very heavy print in their marketing materials, and then quietly funnel traders to their Seychelles entity, knowing that most people are eager to start trading and definitely not eager to start reading the fine print of a user agreement.

Sometimes, there is even a process where the trader “elects” to be signed up with the Tier 3 entity, e.g. because the trader is asked to choose how much leverage they want access to (leverage is capped at 1:30 for retail clients in the UK and not capped at all for retail clients under the laws of The Seychelles).

Sometimes, brands will even allow clients in Tier 1 jurisdictions to sign on with the Tier 3-licensed company. This is of course not something that the Tier 1 financial authority recommends, but it is typically not illegal for a Tier 1 jurisdiction resident to sign up with a Tier 3-licensed broker. It is, however, a big decision, since it removes so much of the legal guardrails that a trader in a Tier 1 jurisdiction expects. It is not a decision one should make simply because one has been promised 1:500 leverage and a $100 first deposit bonus.

Do not attempt to bypass jurisdiction restrictions using a VPN to register under a Tier 1 entity. Regulatory protections are tethered to verified residency, not digital location. Falsifying your onboarding parameters ensures you will be excluded from local statutory compensation pools, and you risk immediate account liquidation or withdrawal forfeiture for breach of contract.

Tier 1 jurisdictions typically have marketing bans that prohibits Tier 3-licensed brokers from marketing themselves to Tier 1 jurisdiction residents. In practical reality, fully enforcing these prohibitions has proven to be difficult, especially when marketing campaigns are run online and brokerage companies are hiding away in lax offshore locations that will not act against them even if foreign financial authorities are launching formal complaints.

So-called “reverse solicitation” is one of the more delicate parts of this model. In basic terms, reverse solicitation means the client approaches the broker on their own initiative, rather than the broker actively marketing into a restricted jurisdiction. In theory, this can allow a broker to serve a client without breaching local marketing rules. In practice, it is often rather obvious what’s going on when a broker is running local language campaigns, offering local payment rails, paying regional influencers, and sending traffic to country-specific landing pages, all while calling the client “self directed”.

For traders, the important documents are not the glossy company group license pages but the actual individual contract or contracts you sign/approve, e.g. the Client Agreement. These documents identify the contracting entity, regulator, governing law, dispute forum, compensation coverage, client money treatment, negative balance protection terms, and whether the account sits inside or outside a strong statutory regime.

Brokers and financial firms use several different names for what is essentially the contract that governs your relationship with the broker. Common alternatives include:

- Client Agreement

- Customer Agreement

- Trading Agreement

- Retail Client Agreement

- Client Terms and Conditions

- Terms of Business

- Account Agreement

- Brokerage Agreement

- Investment Services Agreement

- Customer Terms

- Client Contract

- General Terms and Conditions

- Master Agreement

You can also be asked to sign additional contracts, e.g. a Margin Agreement, a Forex Trading Agreement, and a CFD Agreement. It is important to read these contracts as well and find out if you are signing on with the same entity as before, or if a certain aspect of your trading is being shipped over to another entity.

Why Traders Deliberately Seek Offshore Entities

Offshore brokerages and expanded leverage limits present legitimate operational advantages for sophisticated market participants. However, extracting this commercial utility safely requires a comprehensive, preemptive understanding of the structural and jurisdictional risks involved before committing capital.

Higher Leverage (Especially for Retail Traders)

When traders in Tier 1 jurisdictions seek out offshore brokers, it is often because they want access to higher leverage. Many of the Tier 1 jurisdictions have capped how much leverage brokers are allowed to give to retail traders. The idea is to protect non-professional traders from using very high leverage.

Example: In the EU/EEA countries, retail CFD leverage is capped at 1:30 for major forex pairs, and even lower caps are in place for asset types that are considered more risky, such as minor forex pairs. For speculation on individual shares, the cap is down at 1:5, which means a 20% margin requirement. Contrast this with offshore brokers, who commonly advertise retail leverage from 1:100 to 1:500, and sometimes even 1:1000, depending on product and exact jurisdiction.

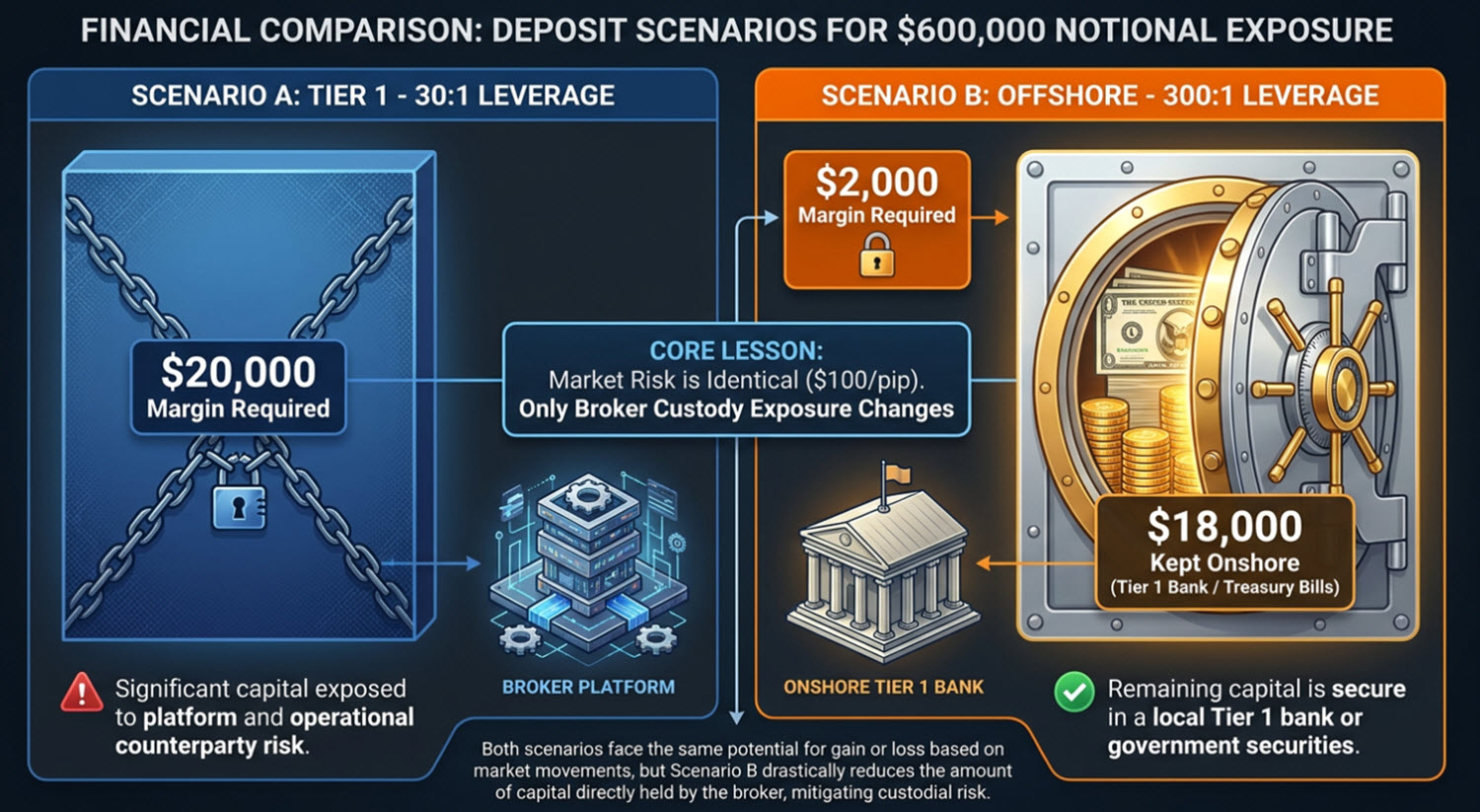

For many traders, high leverage is attractive, since it gives them the opportunity to use their capital more efficiently and safeguard their cash better. A high-volume intraday trader may not want to keep a large cash balance sitting inside a broker just to meet margin requirements. Broker cash is not the same as bank cash. Cash sitting in your trading account carries platform risk, operational risk, counterparty risk, and withdrawal risk. A trader who can run the same strategy with less broker-deposited margin may prefer to hold most capital in a local bank, Treasury bills, or a securities account, then transfer only the required trading float to the broker.

The required margin is calculated as:

Margin required = Notional exposure / Leverage

Assume we have a trader with a maximum EUR/USD exposure of $600,000.

- With 30:1 leverage, we get this: Margin required = $600,000 / 30 = $20,000

So, the required margin is $20,000. - If the trader instead gets access to 300:1 leverage, the required margin drops to a mere $2,000.

Margin required = $600,000 / 300 = $2,000

The trade exposure is the same in both examples, and the market risk per pip is the same. What changes is the amount of capital trapped at the broker. A five pip loss on $600,000 notional is not safer because the trader deposited $20,000 instead of $2,000. The extra $18,000 is collateral, not a magic volatility shield. The trader may rationally prefer to keep that $18,000 somewhere safer.

That is the clean capital efficiency argument. It only works if the trader does not increase notional exposure simply because more leverage is available. If the trader uses 300:1 leverage to run a $6 million position instead of a $600,000 position, the argument collapses into ordinary over-leverage. Sophisticated traders use high leverage to reduce the deposits required for a fixed exposure. Reckless traders use high leverage to increase exposure just because the platform allows it.

Better Access To Restricted Products Such As Perpetual Futures and Crypto Derivatives

A second reason retail traders seek offshore accounts (accounts that are not under Tier 1 regulation) is that they often provide better access to certain financial products that Tier 1 regulators have put limitations on. Two examples are perpetual futures and crypto-linked derivatives.

In the European Union, regulators have begun considering whether perpetual futures should fall under CFD product intervention rules. On February 24, 2026, ESMA issued a public statement reminding firms that derivatives marketed as perpetual futures or perpetual contracts, including those providing leveraged exposure to crypto assets such as Bitcoin, may fall within existing national CFD product intervention measures. The EU/EEA members already have extensive product interventions in place for retail CFDs, including leverage limits, margin close-out requirements, negative balance protection, mandatory risk warnings, and bans on monetary and non-monetary incentives.

The reason why this, in particular, matters a lot to many traders right now is because perpetual contracts have become such a big thing within the sphere of cryptocurrency speculation. Perpetual futures do not expire in the same way as traditional futures, and funding payments keep the contract price aligned with the underlying spot market. Traders use them for directional exposure, hedging, market neutral funding trades, basis trades, and intraday speculation. In many ways, a leveraged perpetual can behave economically like a CFD, and this is why they have caught the attention of Tier 1 regulators.

Even if we don’t go into the specifics of perpetuals, offshore brokers are often appealing to retail traders interested in cryptocurrency speculation, as many Tier 1 regulators are trying to curb retail access to leveraged cryptocurrency products. For regular CFDs in places such as Australia and the EU/EEA, retail leverage is capped to 2:1 for CFDs based on cryptocurrency. In 2021, the UK went even further by banning the sale of crypto-asset derivatives (including most crypto CFDs) to retail consumers altogether.

Unsurprisingly, offshore brokers and cryptocurrency derivative venues fill a lot of the demand that can not be filled with Tier 1 regulated brokers. Traders who want uninterrupted access to cryptocurrency perpetuals, synthetic baskets, tokenized index products, and leverage crypto CFDs look for businesses who are willing to provide this.

Again, the commercial driver is real. A trader running crypto basis strategies, hedging spot holdings, or trading weekend volatility may regard offshore access as necessary. But the product risks and the counterparty risks are also real. Crypto liquidity can fragment across venues, index pricing can fail, funding spikes can become violent, and weekend gaps can hit while larger bank transfers have to wait until Monday. Crypto trades continuously, but much of the traditional financial system used to fund and de-risk positions, especially larger positions, does not. If your offshore trading account’s negative balance protection is discretionary and conditional, you can easily end up owing your broker money.

Algorithmic and Programmatic Optimization

Some traders go offshore because their strategy needs execution access that the onshore brokers that are available to them restrict. Expert Advisors on MT4/MT5, high frequency API access, scalping, news trading, cross exchange hedging, copy trading, signal replication, and latency sensitive systems can all sit in this area, depending of course on the exact strategy details.

Onshore brokers are not uniformly hostile to automation and many FCA, ASIC, CySEC, MAS, and FSCA-authorized firms allow MetaTrader EAs, FIX API access, VPS hosting, and algorithmic order flow. The issue is that Tier 1 jurisdictions typically also impose heavier controls around suitability, best execution, financial promotions, client categorization, and product governance. Brokers may respond by banning some strategy types, raising minimum balances for API access, imposing order throttles, widening spreads around news, rejecting toxic flow, or limiting maximum message rates.

Likewise, offshore brokers are not uniformly more permissive, but permissive offshore brokers do exist and these types of traders seek them out. They may for instance need a broker that allows high leverage scalping accounts, unrestricted EAs, low minimum deposits, copy trading, high frequency bridges, and flexible server setups. For a trader running a programmatic strategy, that freedom has value. A two-second execution delay, a minimum stop distance, or a FIFO-style restriction can turn a profitable strategy into a losing one. The strategy may show excellent returns in a backtest, but once broker restrictions are applied, the edge disappears.

Just as discussed above, using an offshore broker will typically not just remove the specific guardrails that you dislike, but also the ones that would have been beneficial for you, such as mandatory negative balance protection and having access to a smooth pathway for recourse if you end up in a conflict with your broker. Offshore client agreements often reserve broad rights to classify trading as abusive, toxic, exploitative, or inconsistent with market conditions. A trader may be allowed to run an EA for months, then face canceled trades or denied withdrawals after a major profit event. That is not common with every broker, but the possibility is written into enough contracts that it cannot be ignored.

Onboarding Ease

Fast onboarding with few hurdles is another offshore advantage. Tier 1 retail onboarding can be slow because complex instruments require appropriateness checks, risk disclosures, legal client categorization, financial information, experience questions, source of funds checks, and sometimes wealth verification. ESMA has long treated complex products sold to retail investors as an investor protection concern because inexperienced clients may not understand the risks, costs, and expected returns.

Offshore brokers still run AML and KYC checks, and you can expect them to do things such as verify identity, screen your identity against sanctions lists, monitor payments, and request source of funds where required. But the suitability and appropriateness process is usually lighter, and the account can often be opened and funded faster. For clients living outside the Tier 1 countries, and whose documents do not fit neatly into any of the Tier 1 compliance workflows, an offshore broker is sometimes the more realistic choice if the trader wants to avoid a prolonged struggle with customer support to get their documentation approved.

Account Isolation

Some traders use offshore entities for account isolation. A trader may keep a local regulated account for long-term investments, a separate futures account for exchange-traded exposure, and a small offshore account for high leverage intraday FX or crypto derivatives. The offshore account becomes a tactical account, not the household vault, and the fact that this account is not based in the trader’s home country is a positive and not a negative.

This type of structure can be sensible if the deposit and account balance are kept low enough. It becomes much more risky if the offshore account is allowed to become the trader’s main capital pool, e.g. because the platform is convenient, the leverage is high, and withdrawals have worked well so far. Sometimes, everything works great until it doesn’t work at all, and that is how traders find out what counterparty risk and jurisdictional complexity actually entail.

Counterparty Risk

The biggest offshore risk is not spread widening or a bad fill; it is the broker failing to honor the user agreement, e.g. due to broker insolvency or simply because they don’t want to. Below, we will look at a few issues connected to counterparty risk, and why counterparty risk tends to be higher for traders who are using brokers based in offshore (Tier 3) jurisdictions.

Why Mandatory Client Fund Segregation Is So Important When A Broker Becomes Insolvent

In Tier 1 regimes, client money rules are designed to separate client assets from brokerage firm assets. One example is the UK, where firms are subject to the FCA’s Client Assets Sourcebook (CASS), which governs custody assets and client money protections. The purpose is simple; client funds are not allowed to be comingled with company funds, and the FCA has the legal powers to investigate and take actions against FCA-licensed brokers who do not comply.

Tier 3 offshore accounts rarely offer comparable protection. A broker may say client funds are segregated, but that could be empty words. In a Tier 1 regime, segregation is a legally required and audit-backed structure with prescribed rules, reconciliations, and consequences. In a weak offshore setting, segregation may simply be a contractual promise that client money is held in a separate bank account. That is better than nothing, but it may not create the same insolvency barrier, especially when brokers know that they are not being supervised and audited in any meaningful way.

Why is client money segregation so important? Firstly, it reduces the risk of client funds being misused by the firm. When client money is held in segregated accounts separate from the firm’s own funds, it becomes more difficult and less tempting for the firm to use those funds to cover operating expenses, address cash-flow problems, or meet other business obligations.

Segregation also improves transparency and makes regulatory oversight more effective. Secondly, and even more importantly, client money segregation provides significant protection if the firm becomes insolvent. In many jurisdictions, properly segregated client funds are not treated as assets of the firm and therefore do not form part of the insolvency estate. As a result, those funds can often be returned to clients more quickly and with a higher likelihood of full recovery.

By contrast, if client funds have been commingled with the firm’s own money, clients may be left with unsecured claims in the insolvency proceedings. In that situation, they must compete with other unsecured creditors for recovery and will generally rank behind secured creditors. This can significantly delay the return of funds and will usually result in clients recovering only a portion of what they are owed. After all, if the firm had enough assets to cover all its debts, it would probably not have filed for bankruptcy in the first place. For these reasons, client money segregation is one of the most important safeguards in the financial services industry.

In Tier 3 jurisdictions, client fund segregation is usually either not mandatory or mandatory but not strongly supervised and enforced. If a Tier 3-licensed broker fails, the trader’s position will largely depend on factors such as local law, bank account structure, trust recognition, local insolvency practice, and the broker’s records. The trader might have been promised client fund segregation, only to find out that the firm has not upheld this promise. So, the traders who believed their money was segregated are now just unsecured creditors, or client money claimants in a precarious legal position, depending on the exact legal system.

Recovery can take a long time and the amount recovered may be a fraction of the balance. And suing a company for breach of contract (if there was a segregation promise) when it is already in bankruptcy proceedings will rarely yield something worthwhile, especially not in a Tier 3 jurisdiction on the other side of the globe. Even a $10,000 or $20,000 account balance can be too small to justify that type of complex foreign legal action.

This is one of the reasons why offshore trading accounts should not be used as cash or asset warehouses. Using high offshore leverage precisely because it requires less deposited capital is one thing. Parking a full portfolio with an offshore broker is simply foolish.

Third-Party Investor/Trader Protection Schemes

Even when strict rules are in place, there are always those who break them. We know this from all aspects of society and financial services firms are no exception. Since it is possible for a broker to violate the mandatory client fund segregation rule and use up client money before failing, many (but not all) Tier 1 jurisdictions (and some in the Tier 2 category) have a second safety net in place for traders and investors in the form of a compensation scheme that can pay out when a locally-licensed broker is failing and not capable of honoring its legal obligations to a client.

Typically, these schemes have been designed to chiefly function as a type of consumer protection, and are intended to increase consumer faith in investing and to reduce the harm to small-scale investors when a firm fails. Therefore, you will usually see caps that are high enough to make a big difference for most hobby investors and traders, but not high enough to keep large professional accounts out of harm’s way.

If you decide to use a broker in a Tier 3 jurisdiction instead, it is important to keep in mind that Tier 3 offshore jurisdictions typically won’t have well-capitalized investor compensation schemes for brokerage failure. Where any type of scheme exists, it is usually small, narrow, and unevenly enforced, and there is no explicit sovereign guarantee. You are thus stepping away from this type of protection and are much more likely to lose your account balance if the broker fails.

How Investor and Trader Protection Schemes Can Help – If Your Account Is Covered

One example is from the UK, where the Financial Services Compensation Scheme (FSCS) can compensate eligible customers if an FCA-authorised financial firm fails. For investment claims, the current protection limit is up to £85,000 per eligible person, per firm, subject to the FSCS rules and eligibility requirements.

While Australia is considered a Tier 1 regime, it actually does not have any broad investor compensation scheme that protects clients against losses arising from the failure of an investment firm in the way that the UK’s FSCS does. Instead, investor protection in Australia relies on client asset segregation requirements, insolvency law, professional indemnity insurance, and the Australian Financial Complaints Authority (AFCA).

Since 2024, eligible consumers may also have access to compensation of up to A$150,000 through the Compensation Scheme of Last Resort (CSLR) if they have obtained an unpaid AFCA determination and meet the scheme’s eligibility requirements. CSLR provides an additional layer of consumer protection, but it is considerably narrower in scope than the UK FSCS.

The EU/EEA sits somewhere between the UK and Australia. EU/EEA countries are required to have investor compensation schemes under EU law. The protection is not fully harmonized and each country operates its own scheme. Each member state is required to operate a national scheme under the Investor Compensation Schemes Directive (ICSD), which was adopted in 1997, and the minimum level of protection required is currently €20,000 per investor. Coverage, eligibility requirements, and claims procedures vary between jurisdictions under the ICSD investor compensation framework. As a result, an investor with an eligible claim of €20,000 will not necessarily receive the full amount in all EU/EEA countries.

In Cyprus, the investor compensation scheme generally pays 100% of eligible losses, subject to a maximum compensation limit of €20,000 per investor. In Ireland, the scheme typically pays 90% of eligible losses, also subject to a €20,000 maximum cap. This means that an investor with an eligible loss of €20,000 in Ireland would typically receive €18,000 in compensation, whereas a similar claim in Cyprus could be compensated in full up to the €20,000 limit, assuming all eligibility conditions are met.

Kenya is an example of a country that is not considered a Tier 1 regime when it comes to trader protection, but that still operates an Investor Compensation Fund. The Kenyan Investor Compensation Fund (ICF) was established by law and the scheme provides compensation to investors who suffer losses due to the failure of Capital Markets Authority (CMA) licensed intermediaries, subject to regulatory limits and the availability of fund resources. While compensation caps have been increased over time and are commonly referenced at around KES 200,000 per investor per claim in current practice, the actual payout is determined under ICF rules and is not structured as an automatic fixed entitlement equivalent to regimes such as the UK FSCS.

The ICF is not funded like an insurance policy or a government guarantee scheme. It is a pooled industry fund built mainly from contributions within the capital markets system. The primary funding comes from mandatory contributions by CMA-regulated firms. This is thus chiefly a fund that can make a notable difference for micro retail traders in Kenya.

Legal Recourse Issues

The legal recourse problem is something that few people think about until something goes wrong. We assume that if trader protection rules are in place, they will also be followed. When a conflict eventually arises between a trader and a broker, it suddenly becomes very clear that being right is not enough; an authority with strong muscles must also be both willing and able to make the broker follow the rules.

In Tier 1 jurisdictions, there is typically a clear pathway to follow, and it has been made accessible even for small-scale hobby traders. A small-scale hobby trader is probably not going to hire legal representation out of their own pocket and launch a full-on civil court case against a big broker over a frozen account with €1500 in it. Therefore, it is important that the relevant financial authority provides a simpler route. Many issues can be resolved comparatively quickly and easily when it is possible to report a problem to the applicable financial authority or ombudsman and have them evaluate the case. This does not mean that you can expect them to side with you and automatically fight for you like a privately hired attorney would. Instead, the idea is that you can file your grievances with someone who can make an independent investigation and evaluation of the case.

If a locally licensed broker refuses to adhere to a decision made by a Tier 1 financial authority, the authority normally has plenty of tools in its toolbox to escalate the situation. In cases of suspected criminal activity, such as fraud, they can also work together with the wider criminal justice system.

Example: If a UK FCA-licensed broker misprices a CFD, freezes your account, refuses to acknowledge a complaint, or to apply NBP, an eligible retail client may complain to the firm and then to the Financial Ombudsman Service (FOS), the UK’s independent dispute-resolution body for financial services complaints. Issues can also be reported to the FCA, and the FCA can take supervisory or enforcement action. Getting in touch with FOS and the FCA to report a broker is not difficult or costly, and there are pathways available specifically designed with small-scale hobby traders in mind.

If you instead sign up with a Tier 3 regulated broker, recourse can prove much more difficult to attain. For starters, you are probably less familiar with the applicable legal system than your own. When you want to report the issue, you might find that the financial authority does not offer a smooth complaint path, or simply receives your email, and then does nothing. And who is going to force them? Exactly how issues are handled will also vary depending on the user agreement, and can for instance involve local courts, arbitration, internal complaint handling, or having the case referred to a “license provider” who is actually a business from which anyone who pays the license fee gets a “broker license”.

You can also find that what you think is illegal or broker malpractice is actually permitted by the laws and financial regulations of the Tier 3 country. Or it is a violation, but the local legal systems prove really unwilling or unequipped to do anything about it. Brokers pick these offshore jurisdictions for a combination of reasons, and two of those reasons are often light regulation combined with a government and legal system that have developed a reputation for not really being eager to fight the financial services companies as long as they pay their fees.

For a retail trader with a $7,500 dispute, formal litigation in a foreign island jurisdiction is often economically and practically irrational, as legal fees and associated costs will quickly exceed the claim.

The brokers know this very well. That does not mean every offshore broker abuses the position. It means the bargaining structure favors the broker. If you experience an unfair canceled fill, your account gets frozen out of the blue, or your big EA profit is suddenly deemed abusive, your access to recourse is limited. Public complaints, credit card chargebacks, regulator emails, and social media and media pressure may help sometimes, but that is very different from being able to escalate a complaint to a resourceful financial authority that takes trader protection seriously.

It can take a long time to realize how weak your position is, because as long as everything works correctly, this risk is invisible. The broker can process deposits and withdrawals for years, offer tight spreads, and run a good platform. Then one liquidity event, one ownership problem, one bank account freeze, one cyber incident, or one internal fraud suddenly changes the entire situation.

Product and Pricing Discretion

Offshore CFD contracts often give the broker wide discretion over prices, spreads, trading hours, margin requirements, and corporate actions. Of course, some level of discretion is necessary and to be expected because CFDs are OTC contracts. The broker is not simply copying an exchange order book in every product; it may use reference prices, liquidity provider feeds, synthetic cash indices, futures adjustments, dividend adjustments, funding rates, and internal markups to determine the perimeters.

The risk is that without firm rules and supervision from a strict financial authority, brokers can be tempted to manipulate price information, or simply use their discretionary powers to act in a way that unfairly favors the broker. Especially during market turbulence, price formation can become contested. If gold spikes during a liquidity void, was the broker’s quote valid? If a crypto index diverges from major spot exchanges, which feed controls? If a single stock CFD is halted, how is the position valued? If an index CFD opens after a weekend gap, which cash or futures reference is used?

In a Tier 3 jurisdiction, applicable law and the client agreement usually give the broker very broad room to answer. Tier 1 regulation does not remove every dispute, but it narrows the broker’s room to move.

Vague Conditional Negative Balance Protection (NBP)

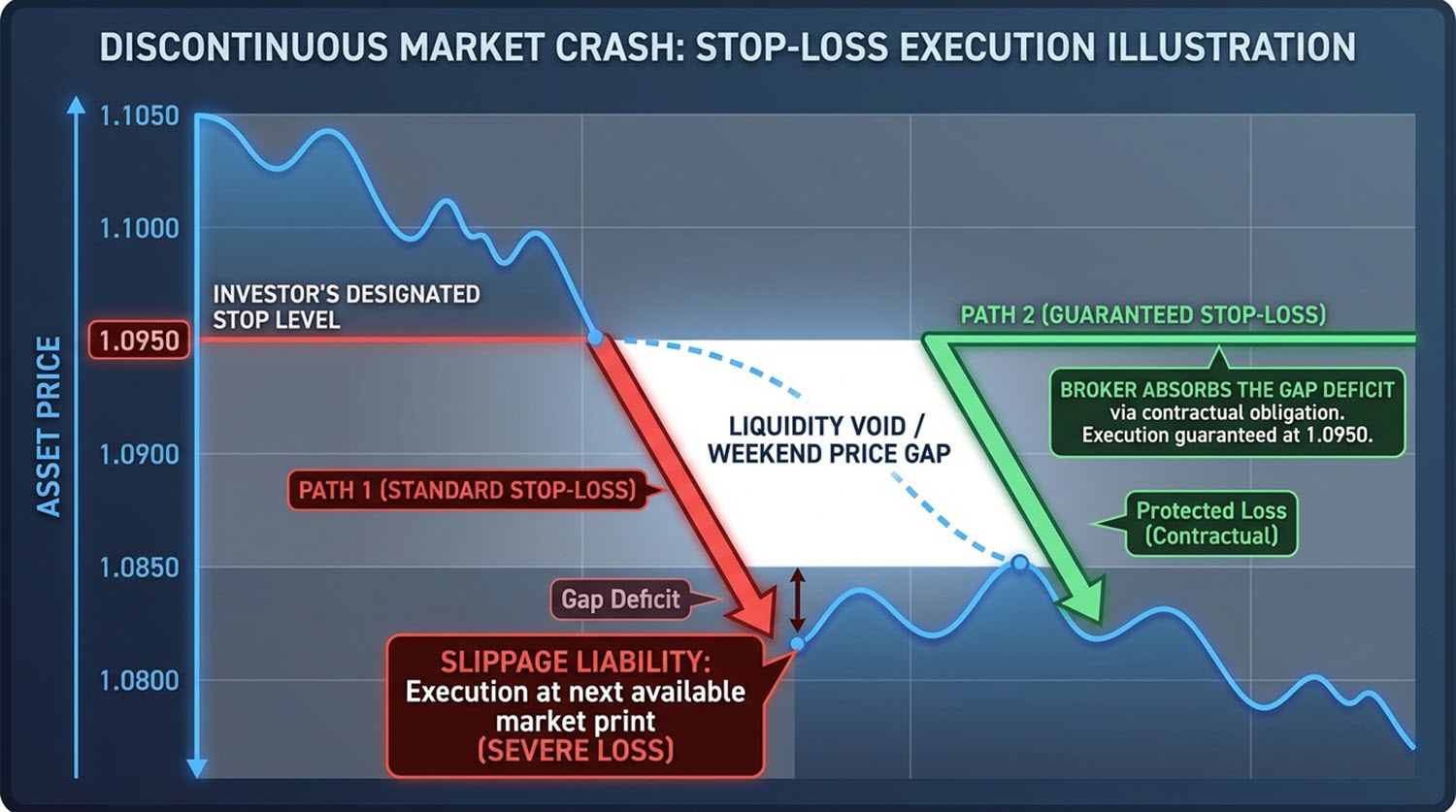

Negative balance protection is another area where offshore terms can look safer than they are. Many offshore brokers advertise NBP. The landing page may say clients cannot lose more than their account balance. The nitty-gritty details of the client agreement may say something less cheerful, and when NBP is not required by law, the client agreement will determine the outcome when your account has suddenly dropped to negative $50,000 after a national bank announcement sent shock-waves through the forex market and your stop-loss orders could not be executed at the expected price points.

In user agreements for brokers based in Tier 3 countries, you will often find a bunch of qualifiers and exceptions that render the NBP promise pretty useless. A very common qualifier is “normal market conditions”, which means that your account will stop having NBP as soon as the broker decides that your sub-zero balance was caused by “abnormal market conditions”. Of course, a leveraged account dropping down far below zero despite stop-loss orders and margin requirements is almost always the result of market conditions not being normal, so you will lose the NBP when you actually need it. One example of this is VT Markets’ Mauritius agreement, which states that its trading systems are designed with safeguards to protect clients from negative balances when trading under normal market conditions. That wording is very far away from a statutory NBP guarantee or even a strong contractual NBP. It implies that outside normal conditions, the safeguard may fail or may not apply.

Another common qualifier is “exceptional market conditions”, i.e. NBP will not or may not apply during exceptional market conditions. This is essentially the same thing as saying NBP will only apply during normal market conditions. One example of a contract that uses this wording is Tickmill’s Seychelles client service agreement, which states that the company may determine that an emergency or exceptional market condition has occurred, including market suspension or closure, failure of a referenced event, excessive movement in the level of a margin trade or underlying market, or the company’s reasonable anticipation of such movement. Admirals SC uses similar wording in its Seychelles terms, allowing the firm to determine that an emergency or exceptional market condition has occurred and listing suspension, closure, failed reference events, and excessive movement as examples.

Force majeure clauses are common around the world, but in many Tier 3 jurisdictions, they can be interpreted extremely broadly, and the brokerage firm gets to decide whether a certain event was force majeure or not. A Mauritius general terms document from Credit Financier Invest states that the firm may determine that an emergency or exceptional market condition exists as a force majeure event, and in the same document, the client is told that liability may exceed credit or other account limits and that the client must pay back any deficit on the account. Once again, it becomes clear that when markets are panicking and falling through stop-losses, you will not have any NBP.

Abusive trading clauses add another layer. Vantage’s global client agreement includes trading with the intention of abusing the negative balance protection facility among behaviors that may be treated as prohibited or abusive, and Exclusive Markets’ client agreement says that any trading strategy based on using the negative balance protection mechanism and creating unfair advantages can be treated as improper or abusive behavior, granting the company an absolute right to suspend the account and terminate the agreement.

Of course, it makes absolute sense that a firm should protect itself against abusive trading, and that clients should not be allowed to utilize strategies that deliberately seek to exploit the NBP. But problems arise when a broker is given the power to unilaterally determine exactly what constitutes abusive trading and apply the clause at their own discretion. Traders need to be able to appeal broker decisions in a meaningful way to avoid being exploited. These clauses are therefore not automatically unreasonable on their own. Brokers do need tools against stale price exploitation, coordinated NBP abuse, and strategies designed to create asymmetric losses at the broker’s expense. The problem is instead the legal asymmetry. The broker decides whether the trading was abusive, and the trader does not have any substantive way of disputing that decision in a legal system that takes trader rights lightly.

Practical Risk Controls for Offshore Accounts

Verifying the Entity Behind the Brand

The first control is entity verification. A trader should identify the exact company that will hold the account. The account application, client agreement, deposit confirmation, and regulator register should all match. The trader should check whether the website clearly separates entities, whether deposits go to bank accounts in the contracting entity’s name, whether the regulator register confirms the license, whether the directors and beneficial ownership are visible, and whether audited financial or group accounts are available.

The trader should verify whether the offshore subsidiary belongs to a wider company group holding Tier 1 licenses. This does not make the offshore account Tier 1 regulated, but it can improve practical confidence. A company group where some of the companies hold licenses from Tier 1 financial authorities typically has more reputational value at risk than an anonymous island company with a rented address. This does not in any way guarantee fair treatment, but it can make it marginally easier to put pressure on the broker group if one of their Tier 3 companies behaves in a way that is not aligned with the overall brand image the group wishes to maintain. Still, group reputation should not be confused with legal guarantee. If the client agreement says the counterparty is a Seychelles company, the UK entity is usually not liable for the Seychelles account unless there is an expressed guarantee, which is rare.

The fact that a broker is willing to ignore the rules of your home country, e.g. by marketing retail binary options to you even though such marketing is banned in your Tier 1 country, tells you a bit about how little regard they have for their reputation in your country, and how blatantly they are willing to go against your home financial authority. Do not assume that your position as a Tier 1 citizen will protect you if the offshore broker decides to freeze your account for bogus reasons.

Contract Review

When few mandatory guardrails are in place concerning retail trader protection, the wording of the user agreement becomes even more important, since the broker can put pretty much any clause in there and not have it invalidated by the court. They might not be able to actually extract your left kidney, but they will definitely be able to freeze your entire account at their own discretion.

The trader should read the user agreement carefully, including sections covering governing law, dispute resolution, client money segregation and safekeeping, negative balance protection, force majeure, abnormal market conditions, abusive trading, order execution, pricing errors, withdrawal rights, set off, account termination, and bonus terms.

Set off clauses need special attention if you will have more than one account with the same broker or within the same company group. A broker may reserve the right to combine balances across accounts or apply positive balances against amounts owed. Fortrade’s Mauritius agreement, for example, states that the company has the right to combine trading accounts and consolidate balances on termination, while also saying it operates negative balance protection on each trading account.

That combination may be harmless in ordinary trading, but it matters during a dispute. You believe you have negative balance protection separately on each individual account, but the broker has established its right to take money from any of your profitable accounts to cover a loss in any of your negative accounts if they combine it with a termination.

Bonus terms are another trap. Offshore brokers often offer deposit bonuses and similar incentives to deposit and trade. The bonus/perk terms and conditions can for instance restrict withdrawals until a very high trading volume is met or allow the broker to remove credit during drawdown. Getting $500 in “free money” is great until you realize your account has been frozen and no withdrawals are possible.

Internal Negative Balance Rules

As we have already touched upon, Tier 3 jurisdictions will typically not require brokers to give retail accounts negative balance protection. This means that any NBP you have comes from the user agreement and is limited by the contract clauses. In many cases, these clauses include a lot of exceptions and limitations, which means your NBP will not be as useful as in a Tier 1 jurisdiction with mandatory retail account NBP.

Because of this, a trader using a Tier 3-licensed broker should always run their own strategy to prevent a negative balance, independent of the broker’s marketing and vague NBP promises. The account should be treated as if broker NBP will fail during the exact event that matters. That assumption can change position sizing, leverage usage, where to put stop loss points, and the use of guaranteed stop-loss orders (when available and trustworthy).

If the stress loss exceeds the offshore account balance and the product has no reliable guaranteed stop, the trader must assume the account can go negative.

The trader can calculate a stress loss using notional exposure and a gap scenario:

Stress Loss = Notional Exposure × Stress Move

This calculates the loss that would occur if the market moved by the specified stress scenario amount.

Example:

If notional exposure is $10,000 and the stress move is 5%, the stress loss is $5,000.

Stress Loss = $10,000 × 5% = $5,000

For FX, a trader can express the same test in pips:

Stress Loss = Pip Value × Gap Size (Pips)

Pip Value = profit or loss per pip movement for the position

Gap Size (Pips) = the assumed adverse price move in pips under the stress scenario

Example:

If the pip value is $100 per pip and the gap size is 50 pips, the stress loss is $5,000.

Stress Loss = $100 per pip×50 pips = $5,000

The stress gap should be product-specific. Major FX pairs may be tested at 100 to 300 pips for shock scenarios. Minor and exotic pairs need wider assumptions. Index CFDs should be tested for weekend gaps of several percent. Cryptocurrency derivatives should be tested for double-digit moves and exchange outages. Commodities should be tested for contract-specific events, not just daily average volatility.

The point is not to predict the exact gap. The point is to size positions so that a plausible discontinuity does not create a debt large enough to matter. Traders who say “that cannot happen” should study events such as the Swiss National Bank EUR/CHF Floor Removal (2015), the WTI Crude Oil Negative Price Event (2020), and the Japanese Yen Carry Trade Unwind (2024), all of which produced market moves far beyond normal daily volatility and made a lot of trading accounts drop far below zero when stop-loss orders could not be executed.

The Operational Capital Cap

Another very important offshore risk control is to limit how much you deposit and how much you keep in your trading account or accounts with the same company group.

Do not deposit your full trading capital at an offshore broker. Deposit only the amount required to run the strategy, plus a defined loss buffer.

The logic is mechanical. Higher offshore leverage reduces the margin required for a fixed exposure. The trader should use that feature to keep capital outside the broker, not to expand exposure until the whole portfolio is at risk again. Inexperienced traders have a tendency to go crazy when they are suddenly given access to high leverage, and instead of using the higher leverage to keep less money in their trading account, they use it to run wild strategies with extreme exposure. This is not the smart way to go.

Suppose a trader has $15,000 allocated to trading. The strategy requires a maximum $500,000 notional FX exposure. At 30:1 leverage, the required margin would be around $16,667, which exceeds the trader’s capital and makes the position impractical. At 250:1 leverage, the required margin is only $2,000. The trader might place $5,000 to $8,000 with the offshore broker: $2,000 for margin, plus additional capital to absorb drawdowns and variation margin. The remaining $7,000 to $10,000 stays in a Tier 1 bank, Tier 1 brokerage account, Treasury bill fund, or another safer custody arrangement.

This does not reduce market risk per trade, but it reduces broker custody risk. If the offshore broker freezes withdrawals, fails, or disputes profits, the trader has not trapped the full $15,000. If the trading strategy suffers a loss, the operational account can be refilled later according to a pre-established rule, not emotion. Alternatively, the trader can employ a new trading plan that requires less notional FX exposure, and gradually rebuild the account instead of refilling it.

The cap should be written down. Traders are very good at inventing reasons to add money after losses. “Just one more transfer to normalize margin” is how an operational float becomes a hostage situation. A fixed cap forces the trader to respect the original reason for going offshore: less idle capital at the broker.

Withdrawal Discipline and Profit Extraction

Keeping your deposit low is only one part of the equation. You also need to keep the total capital in the account below a predetermined cap as your account grows from your trading profits, which means you need to have a plan in place for withdrawals.

Offshore account risk rises with retained profits. A trader may start with a $5,000 operational float, make $18,000, and leave the full $23,000 in the account because compounding feels efficient. And we feel disciplined when we don’t withdraw profits “to waste them” but allow them to stay in the trading account where they “can be put to work to bring in more money”. Unfortunately, this thinking converts trading profit into offshore custody exposure.

A withdrawal rule solves this. The trader can set a balance ceiling, such as two or three times the required operating margin. Any excess is withdrawn weekly or monthly to a safer account. If the broker delays withdrawals, requests more documents, or changes terms, that red flag will become clearly visible while the amount at risk is still comparatively low and not when you already have $100,000 sitting in the account. A broker that processes deposits instantly but withdrawals slowly compared to other brokers deserves scrutiny. Some delay is normal because AML checks and other necessary routines take time. But the delay needs to be reasonable compared to the standard within the industry. Repeated excuses, newly appearing bonus conditions, new volume requirements, surprise verification loops that go on for a long time, or pressure to keep funds trading are warning signs. That is when the trader should stop adding capital, reduce their exposure, and make a plan for capital recovery.

Execution Testing Before Increasing Size

Execution quality should be tested before the account carries serious size. The trader should compare quoted spreads, actual fills, slippage, rejection rates, rollover charges, funding, swap treatment, and order execution around active sessions. A demo account is not enough. Demo execution is often ideal. Live micro-sized trading tells you more and can be done without risking big money.

The trader should test market orders, limit orders, stop orders, stop losses, partial closes, platform disconnections, mobile execution, and API orders. If the broker offers multiple account types, the trader should check how execution changes between the account types that are relevant to you, e.g. standard, raw spread, ECN labeled, pro, or VIP accounts (if applicable).

The goal is not to find perfect execution. Perfect execution is marketing poetry. The goal is to identify whether the broker behaves consistently and whether costs match the strategy. A scalper with a two-pip target cannot tolerate an account where the average slippage is one and a half pips during normal conditions. A swing trader may care less about entry slippage and more about weekend gap policy, financing, and dividend adjustments.

The Guaranteed Stop Security Layer

Guaranteed stop loss orders (GSLOs) can be extra valuable in offshore accounts where statutory NBP may be absent or restricted. Of course, GSLOs are only valuable if the broker actually honors their GSLOs when you need them the most, and some of them won’t.

The difference between a normal stop-loss order and a GSLO is that the second one is guaranteed by your broker.

A standard stop-loss order is not a guarantee that you’ll exit at a specific price. Instead, it is an instruction to the platform to send a market order once a specified trigger price is reached. Under normal conditions, the fill you get may be very close to the stop-loss price point. However, the execution price is always determined by available liquidity, not by the stop price itself. A market order can only execute against actual liquidity available in the market. If no trades occur at 1.0950, where your stop-loss point is, there is nothing to fill against at that price. When your order finally fills, the price might be much worse. This is how trading accounts can become depleted during tail events even if every open position has been fitted with a stop-loss.

A GSLO is a contractual guarantee of the exit price, usually for a premium or wider dealing cost. The premium may be charged upfront, embedded in the spread, or refunded if not triggered. Having a GSLO instead of a normal stop-loss matters during gaps. With a GSLO, your broker assumes the risk that the stop-loss order runs into thin liquidity.

Not every offshore broker offers GSLOs. Many do not, because guaranteeing a stop creates broker tail risk. Those that do offer them may restrict them in various ways, e.g. through special rules regarding eligible products, minimum distances, maximum trade sizes, and trading hours. The trader should read the terms and use small positions to test how GSLOs behave around weekends, earnings, central bank decisions, and commodity expiry periods.

A GSLO is not a full substitute for Tier 1 NBP. It protects only the position to which it is attached, and only according to its terms. But for gap prone trades, it is one of the few tools that can turn an uncertain loss into a defined loss, provided that the broker honors the GSLO.

GSLOs are most useful where discontinuous pricing is plausible. That includes single stock CFDs around earnings, equity index CFDs over weekends, oil or natural gas near contract events, FX pairs around central bank surprises, and crypto products during low liquidity periods. For liquid intraday major FX trades, the premium may not be worth paying.

The Broker’s Own Risk Management In The Context of GSLOs and Tail Events

How likely your Tier 3 broker is to properly honor the GSLO will partly depend on how well the company does its own risk management around tail events. A GSLO is only as good as the broker’s ability and willingness to absorb losses when extreme market moves occur. A strong, well-capitalized broker that carefully manages tail-risk events is more likely to honor GSLOs smoothly during market crises than a weakly capitalized broker with poor risk-management routines.

Brokers manage the risk of GSLOs much like an insurance company manages the risk of providing insurance coverage. When a broker offers a GSLO, it is promising to fill a client at a specified price even if the market gaps through that level. If the market moves violently and there is no available liquidity at the stop price, the broker must absorb the difference between the guaranteed price and the actual market price.

One way brokers manage this risk is by charging a GSLO premium. Most guaranteed stops are never triggered, so the fees collected from many clients help offset the losses incurred when GSLOs are activated during extreme market events. Brokers also typically require GSLOs to be placed a certain minimum distance away from the current market price. This reduces the likelihood that ordinary market fluctuations will trigger the guarantee.

Exposure limits are another important risk management tool here. Brokers often restrict the maximum position size that can be covered by a GSLO and may limit the total guaranteed exposure they are willing to accept in a particular market. This prevents a single client or a concentration of clients from creating excessive liability for the firm.

Many STP/ECN brokers hedge their net exposure with tier-1 banks or institutional liquidity providers. If clients are collectively long a currency pair, the broker may hold an offsetting position in the institutional market to neutralize directional risk. While this baseline hedging substantially reduces the broker’s overall market exposure, it does not eliminate localized GSLO risk.

Crucially, institutional tier-1 banks do not offer GSLOs to retail brokerages. When an offshore broker guarantees a stop, they are almost entirely absorbing that specific execution gap risk internally on their own balance sheet – relying strictly on their internal premium pools to smooth out tail events. If a discontinuous market gap exceeds the broker’s internal capital reserves, the contractual guarantee faces immediate structural default.

The reason these precautions are necessary is that tail events do occur. During the 2015 Swiss franc shock, for example, some currency pairs moved thousands of pips in a matter of minutes after the Swiss National Bank unexpectedly removed its exchange-rate floor. Events of that magnitude can create substantial losses for brokers that have guaranteed client stop prices. A broker’s ability to honor its GSLO commitments, therefore, depends not only on the wording of the guarantee but also on the quality of its risk management, hedging practices, and financial resources.