Negative Balance Protection in Leveraged Trading: Mechanics, Regulation, Broker Risk, and Trader-Level Defenses

- The Core Mechanics of Unlimited Liability in Leveraged Trading

- Examples of Historical Catalysts for Mandated Negative Balance Protection

- Regulatory Frameworks and Jurisdictional Divergence

- The Mechanics of Broker Risk Internalization

- Technical Loopholes, Structural Risks, and Contractual Gotchas

- Additional Risk Mitigation for the Retail Trader

- Appendix: Financial Jargon Explanations

Negative balance protection (NBP) means that your broker can not let your account balance fall below zero. In many jurisdictions, laws and regulations now stipulate that brokers must give NBP to retail accounts, i.e. accounts that are not classified as professional trading accounts.

It looks neat at first glance, but it is advisable to find out exactly what the NBP for your account entails before you put any money on the line. Among other things, these are a few examples of questions that need to be answered:

- Does the NBP for your account only pertain to losses caused by leveraged trading? Can the account fall below zero due to other causes, e.g. swap fees and financing charges?

- What does the NBP mean for your broker’s rights to automatically close your open positions and possibly realize losses in situations where you would have preferred to keep them open and ride out the storm? And how do you need to adjust your strategy with this in mind?

- Is your legal counterparty actually based in a jurisdiction where NBP is mandatory for retail accounts, or have you been signed on to another entity? A broker can feature their top-tier jurisdiction license or licenses heavily when they market their global brand, and still onboard clients through alternative companies in laxer, offshore locations.

In leveraged trading, a negative balance is not just a bad trade. It is the point where market risk crosses into credit risk. The trader no longer has a losing account, the trader has a debt to the broker, unless an external rule, a contract term, or a broker policy cancels that debt. That distinction matters because leverage changes the legal shape of a loss. A cash equity investor can lose the money paid for the shares. A leveraged CFD, rolling spot FX, spread bet, or futures trader can lose more than the deposit if the market moves through the broker’s liquidation process faster than the broker can execute.

Negative balance protection, usually shortened to NBP, is the rule or contractual promise that limits a client’s loss to the funds in the trading account. In some jurisdictions it is mandatory for retail accounts, i.e. accounts held by a non-professional trader. In others, it is optional, which means that it can also be made highly conditional or used mainly as a marketing gimmick without strong contractual backing. Traders who ignore these differences can end up paying a lot for that oversight.

In this article, we will examine NBP from the mechanical, historical, regulatory, broker, and trader perspectives. It assumes basic trading knowledge about things such as margin, leverage, stop losses, CFDs, futures, FX pairs, liquidity, and slippage. The focus is not on whether leverage is good or bad. The focus is simpler: under what conditions can a leveraged loss become a legal debt that you owe your broker, and what actually blocks that from happening?

Negative Balance Protection is fundamentally a risk-shifting mechanism, not a risk-elimination tool. While it successfully shields retail traders from catastrophic credit liability, it simultaneously forces brokers to insulate their own balance sheets upstream. To mitigate this transferred risk, brokers aggressively adjust their operating conditions—slashing retail leverage limits and executing earlier, highly automated platform close-outs. Understanding NBP means recognizing that your protection from debt is bought at the cost of tighter platform restrictions.

Negative balance protection solves one problem for the trader: it stops an NBP-covered leveraged trading loss from becoming a debt. That is a serious protection and it can have a huge impact on the trader’s personal financial situation. Events such as the Swiss National Bank (SNB) shock of 2015, the Negative West Texas Intermediate (WTI) oil price episode of 2020, and the Japanese yen carry trade unwind of 2024 have shown us with stark clarity that simply putting stop-loss orders on our open positions is not enough. When liquidity disappears, stop-loss orders can not be executed as planned. Several of our team have experienced this on many occasions over the years in their real-money trading activities.

For traders and investors with basic market knowledge, the practical view is straightforward. Before placing leveraged trades, know exactly which legal entity you have a broker agreement with, which jurisdiction that covers your legal relationship, the applicable financial authority, your own client classification, product coverage, margin close-out rules, and exact NBP wording. Then size trades as if stops can slip because they can. Consider using guaranteed stops where the gap risk justifies the cost. Keep broker exposure diversified enough that one firm’s bad day does not become your full balance sheet’s bad decade.

The Core Mechanics of Unlimited Liability in Leveraged Trading

Account equity

At any moment, your leveraged trading account will have a cash balance, a floating profit or loss, and an equity balance. The cash balance is what remains after deposits, withdrawals, realized gains, realized losses, commissions, swaps, financing, and fees. Floating profit or loss is the unrealized mark-to-market result on open positions. Equity is the broker’s estimate of what the account is worth at that moment.

The standard equation is:

Equity=Balance+Floating Profit or Loss

Understanding Margin

Margin is collateral (posted by the trader) against open exposure. Used margin is the amount locked to support current positions. Free margin is the remainder that can absorb losses before margin controls begin to matter.

The margin level expresses the health of the account:

Margin Level = (Equity / Used Margin) × 100

The margin level is normally expressed as a percentage. What the formula measures is “How many times bigger is my equity compared to the margin I’ve used?”

A simple example shows the basic process:

A trader deposits $5,000 and opens a leveraged position requiring $2,500 of used margin. The account starts with $5,000 equity and a margin level of 200%. If the position loses $1,250 on a mark-to-market basis, equity falls to $3,750 and margin level falls to 150%. If the loss grows to $2,500, equity falls to $2,500 and the margin level falls to 100%.

Let’s verify step by step.

1) Initial state

- Equity = $5,000

- Used Margin = $2,500

Margin Level = (5,000 / 2,500) × 100 = 2 × 100 = 200%

Question: How many times bigger is my equity compared to the margin I’ve used?

Answer: Your equity is 200% (5,000) of the margin used (2,500).

2) After the $1,250 loss

- Equity = 5,000 − 1,250 = 3,750

- Used Margin = $2,500 (unchanged)

Margin Level = (3,750 / 2,500) × 100 = 1.5 × 100 = 150%

Question: How many times bigger is my equity compared to the margin I’ve used?

Answer: Your equity is 150% (3,750) of the margin used (2,500).

3) When the position has lost $2,500 in value

- Equity = 5,000 − 2,500 = 2,500

- Used Margin = $2,500

Margin Level = (2,500 / 2,500) × 100 = 1 × 100 = 100%

Question: How many times bigger is my equity compared to the margin I’ve used?

Answer: Your equity is 100% (2,500) of the margin used (2,500). It is not any bigger than the margin used.

Margin Calls and Forced Closing of Positions

After the loss in the example above, inexperienced traders might think the broker will simply close the trade, but that is not universally true. Each broker has a margin call level, a stop-out level, liquidation rules, position sequencing rules, market closure rules, and execution rules. Also, the broker needs a tradable price and enough liquidity to close the position. Simply putting something up for sale does not mean a purchase will be made.

An account deficit forms when account equity falls below zero before the broker can close the position at a price that preserves the account balance. Put differently, the broker has already allowed the client to control a notional exposure larger than the money in the account. If the asset price drops past the point where the collateral is enough, the loss belongs to somebody. Without negative balance protection (NBP), that somebody is the trader.

While the account has positive equity, the trader is losing that money. Once equity is negative, the broker has paid, credited, or become exposed to a loss beyond the trader’s cash. Without NBP, the negative balance is treated as an amount due from the client to the broker, in accordance with the account agreement. In broker language, the deficit may be called a debit balance, negative equity, account shortfall, or unsecured obligation.

Negative balance protection changes who gets stuck with the bill. It does not stop the market from moving and it does not prevent poor liquidity. It only decides who carries the shortfall after the position is closed. In a mandatory NBP regime, the broker must limit the retail client’s liability for covered products to the funds in the account. The account can still be stopped out at a terrible price and it can absolutely drop down to zero. The platform can even record a negative figure for the account. The difference is whether that figure becomes a collectible debt that the trader is required to pay. With NBP, it does not. The trader can lose everything in the account when a leveraged trade cannot be closed quickly enough, but not more. This is a risk that brokers are aware of when they extend credit (leverage) to traders.

Mathematical Modeling of a Margin Breach

Assume a trader opens a long position in a CFD or rolling spot FX product.

Let:

-

D = Account deposit

-

B = Account balance before floating Profit or Loss (PnL)

-

Q = Position size in units

-

P0 = Entry price

-

Pt = Current price

-

L = Leverage multiple

-

m = Margin requirement as a decimal (where m = 1 / L)

-

UM = Used margin

-

Et = Equity at time t

-

S = Broker stop-out margin level (expressed as a decimal, e.g., 0.50 for 50%)

For a long position, floating PnL can be simplified as:

Floating PnL = Q * (Pt – P0)

Ignoring fees and financing for clarity:

E_t = B + Q * (P_t – P_0)

Where:

E_t = equity at time t

B = account balance

Q = position size

P_t = current price at time t

P_0 = entry price

Used margin is:

UM = Q * P_0 * m

Where:

UM = used margin

m = margin requirement

The margin level is:

ML_t = [B + Q * (P_t – P_0)] / [Q * P_0 * m] * 100%

A broker stop-out trigger occurs when:

ML_t <= S

Where:

S = stop-out level

If the stop-out level is 50%, then:

[B + Q * (P_t – P_0)] / [Q * P_0 * m] <= 0.50

Solving for the trigger price on a long position:

P_t <= P_0 + [(0.50 * Q * P_0 * m – B) / Q]

This can also be written as:

P_t <= P_0 + (0.50 * P_0 * m) – (B / Q)

The zero-equity price is lower than the stop-out trigger if the stop-out system works normally:

0 = B + Q * (P_t – P_0)

Solving for the zero-equity price:

P_t = P_0 – (B / Q)

A trader with $10,000 equity controlling $500,000 notional exposure does not need an outrageous move to wipe out. A 2% adverse move exhausts the account before fees. In normal trading, the broker may liquidate around a margin threshold and leave residual equity. In a discontinuous move, the tradable market may reopen 3%, 5%, or 10% away. On $500,000 notional exposure, a 5% gap equals $25,000. The account is now not simply down, it is negative $15,000. And that is before any financing, spread widening, and liquidation costs have been included in the calculation.

A stop-loss order does not remove this risk because a stop-loss order only works as intended when there is someone on the other side willing, and able to buy the long position you want to close. A standard stop-loss is an instruction to execute when a trigger condition is met. It is not a guaranteed fill price. If EUR/USD is quoted at 1.1000 and the next executable bid is 1.0950, a sell stop at 1.0990 will not magically create enough liquidity at 1.0990. The platform can trigger the order, but it cannot force a bank, non-bank market maker, exchange participant, or liquidity provider to trade at the stop-loss price point.

Slippage Impact on Realized Deficits

The deficit can be modeled more directly by separating the stop trigger price from the actual fill price.

For a long position stopped out in a falling market:

Deficit = [(P_fill – P_stop) * Q] – E_trigger

This formula needs sign discipline. For a long position, P_fill is lower than P_stop, so the price difference is negative. In practical risk terms, traders often express the slippage loss as an absolute value:

Slippage Loss = |P_fill – P_stop| * Q

Then the realized deficit is:

Deficit = Slippage Loss – E_trigger

Where:

P_stop = the price at which the stop-out or stop-loss was triggered

P_fill = the actual execution price

Q = position size

E_trigger = account equity remaining when the trigger fired

If the slippage loss is smaller than the equity remaining at trigger, the trader survives with reduced equity.

If the slippage loss exceeds the equity remaining at trigger, the account moves negative. That is the moment where market loss turns into credit exposure.

Take a retail FX account trading 5 standard lots. In most major FX pairs, one standard lot is 100,000 units of base currency, so 5 lots is 500,000 units. On many USD-quoted pairs, a one-pip move on 5 lots is approximately $50.

Assume the trader still has $2,000 of positive equity at the stop-out trigger. The broker’s liquidation engine triggers a close at the stop price, but the market gaps 50 pips before the order is filled.

The slippage loss is:

50 pips * $50 per pip = $2,500

The realized deficit is:

$2,500 – $2,000 = $500

That is the conservative version. It shows how quickly a positive balance can become a debt. But a larger debt requires either a larger gap, a larger position, or both.

Now use the same 5-lot position with a 240-pip discontinuous gap, which is not fantasy during a central bank shock, a weekend repricing, or a flash liquidity event in a thinner pair.

The slippage loss is:

240 pips * $50 per pip = $12,000

With $2,000 equity remaining at the trigger:

Deficit = $12,000 – $2,000 = $10,000

The trader did not “risk $10,000” in the way traders usually speak. The trader may have believed the remaining balance was $2,000 and the stop-out system would close the trade. The gap turned that assumption into a debit balance.

To keep the requested 50-pip gap while showing a $10,000 debt, the position size has to be larger than 5 standard lots. A 50-pip gap needs a pip value of $240 per pip to create a $12,000 slippage loss. That means 24 standard lots on a USD-quoted major pair, not 5 lots.

The arithmetic is:

50 pips * $240 per pip = $12,000

Then:

$12,000 – $2,000 = $10,000

So the clean version is this:

A 50-pip gap on 24 lots can turn $2,000 of remaining equity into a $10,000 debt.

A 240-pip gap on 5 lots can do the same.

The mechanism is identical. Only the position size and gap size change.

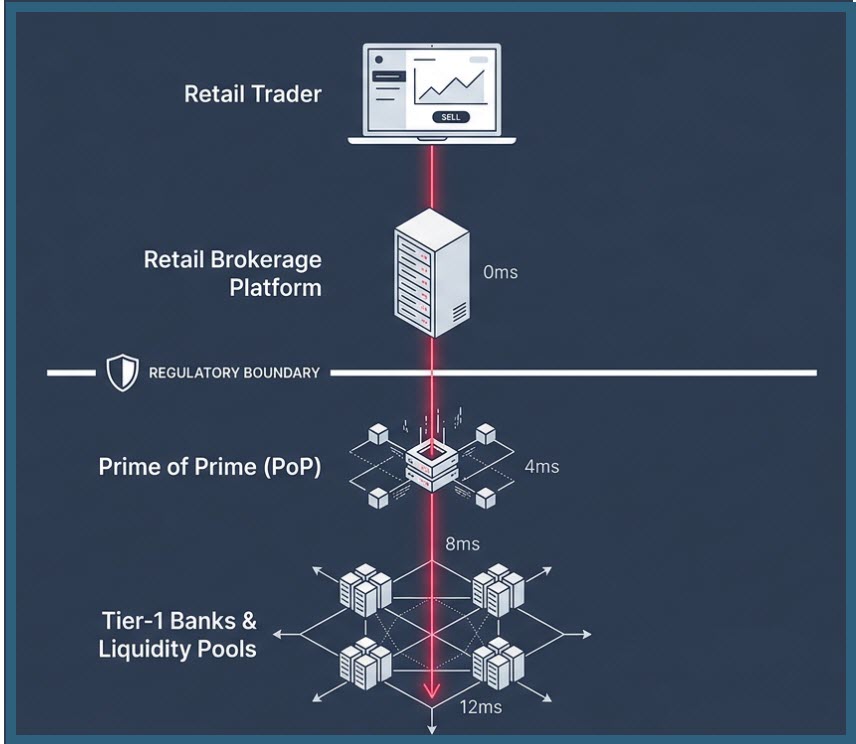

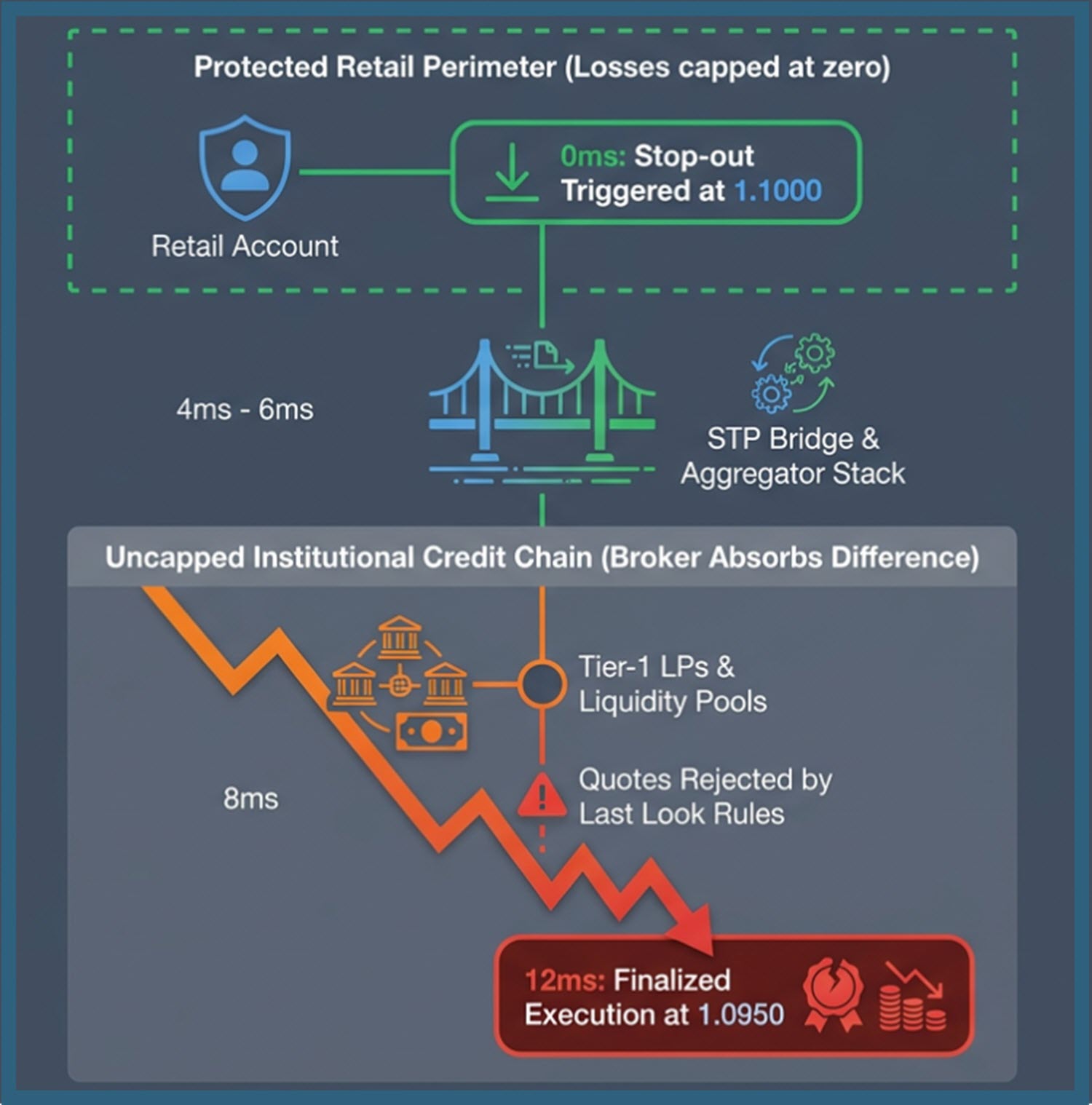

The time window can be absurdly short. A 12-millisecond sequence is enough in a modern OTC FX stack. The account is alive at millisecond zero, breached at millisecond two, routed by millisecond five, rejected or repriced by millisecond eight, and filled by millisecond twelve at a price that no longer resembles the stop trigger.

Slippage Mapping by Execution Model (MM, STP and ECN)

The execution model decides how many links sit between the retail account and the final fill, and each model has different failure points during a margin breach. Examples of common models are the market maker (MM) broker, straight-through processing broker (STP) broker, and electronic communications network (ECN) broker.

Market Maker (MM) Broker

In a market maker model, the broker internalizes client orders and is the counterparty to the client’s trading. When the trader loses, the broker gains, unless the broker has hedged that exposure externally.

During a margin close-out, the broker can usually liquidate the position internally at its quoted price without first routing the order to an external liquidity provider. This can make the close-out process faster and operationally simpler than in models that rely on external execution.

However, internalization does not eliminate slippage or market risk. The broker still controls its quote stream, spread, execution policies, and overall risk book. During periods of volatility or market gaps, the broker may reprice its internal book to reflect available external liquidity, hedging costs, or its own risk management framework. If the broker has hedged the client’s exposure externally, that hedge position must still be managed or unwound in the broader market. If the broker has not hedged the exposure, a client’s negative balance may remain primarily an internal receivable owed to the broker rather than an upstream liquidity loss. In either case, unless NBP applies to the trader’s account, the broker may treat the deficit as a collectible debt under the client agreement.

STP Broker

In an STP model, the broker routes the order straight through to external liquidity providers (LPs) or a prime broker arrangement. The broker may aggregate prices from banks and non-bank LPs, apply a markup, and then send client orders through a bridge. The bridge connects the retail platform, such as MetaTrader 5 or cTrader, to the broker’s liquidity stack. During calm markets this can feel instant, but during stress, every extra handoff matters.

That order passes through the broker’s bridge or order management system, where symbol mapping, execution logic, risk controls, position size limits, and routing rules are checked before the order is forwarded to a prime broker, liquidity hub, liquidity aggregator, or other external execution venue. If the execution path involves multiple liquidity providers, the receiving system may aggregate available quotes and route the order across one or more LPs depending on available depth, pricing, and execution logic. One or more LPs accept, reject, partially fill, or requote the order. The result travels back through the same chain. The platform updates the position and account balance.

Each step may take microseconds or milliseconds. That sounds tiny until the market is moving faster than the stack can complete the loop. A retail trader does not need a long delay to suffer serious slippage. On leveraged exposure, a few milliseconds during a price vacuum can be more than enough.

ECN Broker

An ECN model is usually presented as direct access to a network of participants. In practice, retail ECN trading still normally involves a broker, bridge, aggregator, and credit relationship. The client does not personally face a Tier 1 bank with a Bloomberg terminal. Retail traders do not directly trade as institutional counterparties with major banks. The retail broker provides the account, margin system, platform connection, and credit wrapper. The ECN or liquidity pool provides executable bids and offers from multiple participants.

During a breach, ECN-style execution can produce market depth benefits if real liquidity is available. It can also expose the trader to thin book slippage if depth disappears. A stop-out order that consumes the top of book may sweep several levels. If there are no bids near the trigger price for a long liquidation, the fill may print far lower. Transparent depth is useful, but transparent emptiness is still emptiness.

In other words, the ECN model system tries to match your trade with real buyers and sellers in the market. When everything is normal and there is enough activity, this can be good because you get access to real prices from many participants. But during an unusual market event, things can behave very differently because the market may be “thin,” meaning there aren’t many suitable orders sitting at each price level.

Imagine you are trying to sell something quickly, but there are only a few buyers. The first few buyers might be willing to buy at $100. If your forced sell order is large enough, it keeps going down the list of buyers, and each time it fills a level, the next available buyer is offering a lower price. So instead of selling all at one price, your order “walks down” the price ladder until it has been completed. Your order consumes all the available bids at each price level until it is fully filled. If the market is very thin or suddenly drops, there may be almost no buyers near your stop-out level. In that case, your liquidation can happen at much worse prices than you expected because the system can only match you with whatever liquidity is actually there at that moment.

ECN execution can give you very fair pricing in normal markets, but in fast-moving or stressed markets, it can lead to worse fills if liquidity disappears.

Prime Brokers, Tier 1 LPs, and Last Look

A prime broker is a large financial institution (usually an investment bank) that provides infrastructure so smaller brokers, hedge funds, and trading firms can access the financial markets more easily. In simple terms, a prime broker is a “middle-layer” that lets clients trade with big liquidity providers and exchanges without needing to set up those relationships themselves.

A prime broker typically provides market access, credit, settlement and clearing, securities lending (for shorting), and risk and reporting infrastructure. It gives the client, e.g. a retail broker, access to liquidity providers (e.g. major banks) and trading venues, and it extends credit so the retail broker can trade larger positions than their own cash balance would allow. This is what enables margin trading at scale.

After a trade happens, the prime broker handles the back-end process of making sure cash and positions are properly recorded and settled. For short-selling, the prime broker can lend the required asset. Through its risk and reporting infrastructure, the prime broker also keeps track of positions, exposure, and margin requirements, and provides consolidated reporting. Without a prime broker, most small retail brokers wouldn’t be able to access deep institutional liquidity or offer leverage at scale.

While this structure gives the retail broker access to deep institutional liquidity, it also adds credit controls, margin requirements, and execution protocols set by the prime broker. Prime brokers sit above the retail brokers in the liquidity chain, and when a retail trader breaches margin, the broker’s close order may be mirrored by hedge adjustment at the prime broker level. If the broker is A booking the trade, the external hedge may need to be closed into the same stressed market. The prime broker and LPs do not care that the original loss came from a retail client with $2,000 left. They care about the retail broker’s credit and settlement obligations.

Tier 1 liquidity providers stream prices under rules that may include a concept known as “last look”. Last look gives an LP a short window to accept or reject an incoming trade request after seeing it. The LP may, for instance, reject because the price is stale, the market has moved, the requested size is too large, credit limits are tight, or the trade fails internal risk checks. In ordinary markets, last look may be invisible or nearly invisible to the retail trader. During a margin breach, it can matter a lot. Suppose a close order is sent to an LP at 1.1000. In the milliseconds before acceptance, the real market shifts to 1.0975. The LP may reject the order at 1.1000. The broker then re-routes or accepts the next available price. The trader’s margin system did its job. The execution venue did not fill at the stale level. The fill may arrive several pips, dozens of pips, or in extreme cases, hundreds of pips away.

It is very important to remember that a margin close-out trigger is not a fill. A stop loss is not a fill. A platform quote is not a fill. A risk engine instruction is not a fill. The only thing that matters for realized profits and losses is the execution price confirmed back to the retail broker and booked to the account.

Another thing to consider is the use of Prime-of-Primes. You can find more information about this in “The Mechanics of Broker Risk Internalization” section of this article. Many retail brokers are not large enough to connect directly with a Prime Broker. Instead, they connect to a Prime of Prime (PoP) and get indirect access to a Prime Broker that way. This adds another layer to the stack.

A 12 Millisecond Deficit Sequence

This example of a 12 millisecond breach shows how quickly a positive balance can become a debt.

- At 0 ms, the trading account has $2,000 equity remaining. The trader holds 24 lots in a USD-quoted FX pair, giving a pip value of roughly $240 per pip. The stop-out level is reached at 1.1000. The platform marks the account for liquidation.

- At 2 ms, the broker’s risk engine sends a market close order. The platform display may still show a price near 1.1000, but the executable bid is already falling.

- At 4 ms, the order reaches the bridge. The bridge converts the retail platform order into the format required by the broker’s liquidity aggregator or prime of prime.

- At 6 ms, the order is routed to external liquidity. Available bids near 1.1000 disappear. The first LP rejects the request under the last look because the price is stale.

- At 8 ms, the aggregator attempts the next available pool. The market is now 30 pips lower. Depth is thin. The broker’s system continues seeking execution because the account must be flattened.

- At 10 ms, the order sweeps available liquidity. Partial fills occur across worse levels.

- At 12 ms, the final average fill price is 1.0950, 50 pips below the stop trigger.

The extra loss from slippage is:

50 pips×$240/pip=$12,000

The account had only $2,000 equity when liquidation triggered. This means:

Realized Deficit=$12,000−$2,000=$10,000

Without negative balance protection (NBP), that $10,000 becomes the legal obligation of the trader. With NBP, the broker absorbs the shortfall for the protected retail account, subject to the rules and product coverage. The market event is the same in both cases. The fill is the same. The legal destination of the shortfall is not.

That is the core mechanic traders need to understand. A leveraged account can move from solvent to negative in less time than it takes a trading app to redraw the price ladder. A stop-out system always needs an executable market to work as intended.

The following structural diagram maps the order execution path across the retail and institutional boundaries detailed above:

Examples of Historical Catalysts for Mandated Negative Balance Protection

The legislative push for mandated Negative Balance Protection (NBP) that we have seen in many countries, especially for retail accounts, did not come out of nowhere. It was largely a reaction to a series of financial crises, market shocks, and high-profile retail trading losses that exposed the dramatic consequences of retail traders using leveraged trading products during extreme market events.

The 2008 global financial crisis, the 2015 Swiss franc shock, and several other periods of extreme market volatility clearly demonstrated how quickly traders could accumulate losses exceeding their account balances, even when stop loss orders were in place. Regulators increasingly viewed these incidents as evidence that existing risk disclosures and margin requirements were insufficient to protect consumers. As retail participation in leveraged trading expanded, policymakers faced mounting pressure to introduce safeguards that would limit catastrophic losses and restore confidence in financial markets.

Below, we will take a look at a few of the events in the 21st century that contributed to political concern regarding non-professional traders’ ability to instantly rack up serious debt with their broker. Of course, events like these happened in previous centuries as well, but leveraged retail trading did not become widespread until the advent of online retail trading in the 21st century. For most of the 20th century, leveraged trading was largely confined to professional traders, institutional investors, and wealthy individuals who had access to brokerage services that offered leverage.

Examples of factors that contributed to increased retail access to leverage in the late 1990s and early 2000s were financial deregulation, globalization of capital markets, and the rise of electronic trading platforms online that accepted hobby traders. A major shift occurred when a growing number of online trading platforms began making highly leveraged products, including contracts for difference (CFDs), accessible to ordinary retail traders.

The 2015 Swiss Franc Event

The Swiss franc event of January 15, 2015, is one of the cleanest modern examples of how a leveraged retail account can dive below zero extremely quickly. This was not a normal volatility event, it was a policy floor disappearing under a market that had built trades, risk models, hedges, and client leverage around the belief that the floor would hold.

Since September 2011, the Swiss National Bank (SNB) had maintained a minimum exchange rate of 1.20 Swiss francs (CHF) per euro. The policy was widely understood as a defense against excessive CHF appreciation. Traders did not need to believe the floor was eternal to become exposed, they only needed to believe the Swiss National Bank would either keep defending the floor or remove it by phasing it out gradually and predictably. That assumption aged badly.

At about 10:30 a.m. Central European Time on January 15, 2015, the Swiss National Bank announced that it was discontinuing the EUR/CHF minimum exchange rate. It also cut the interest rate on sight deposit account balances further into negative territory. Within minutes, EUR/CHF fell through 1.20, then through levels where stop losses, margin close-out engines, and broker hedge systems expected liquidity. The market was not repricing in a smooth line, it was jumping through empty air.

The immediate price action broke the common retail trading misunderstanding that a stop-out level equals an exit level. Many traders were long EUR/CHF because the 1.20 floor appeared to offer an asymmetric setup: downside seemed politically limited, while upside remained open if the euro recovered. Once the floor was removed, that perceived limited downside vanished. Worse, the market did not trade continuously enough for standard liquidation systems to close client positions near the margin breach.

A rough timeline is useful to understand the dynamic better:

- Before 10:30 CET, EUR/CHF traded close to the 1.20 floor. Liquidity appeared stable largely because the SNB’s policy had compressed volatility, reinforced confidence in the floor, and encouraged heavy positioning near 1.20.

- At 10:30 CET, the SNB released the policy change. In the first minute after the announcement, liquidity providers widened prices, withdrew quotes, and/or reduced size. Stop losses and margin liquidation orders began hitting the market.

- Between roughly 10:31 and 10:40 CET, EUR/CHF printed extreme levels across venues, with inconsistent prices and poor executable depth.

The ICP EBS Issue

The ICAP EBS issue emerged during the extreme volatility that followed the Swiss National Bank’s decision on January 15, 2015, to abandon the EUR/CHF exchange rate floor. ICAP was one of the world’s largest interdealer brokers, and it owned EBS, a major electronic trading venue used by banks and institutional participants in the foreign exchange market. EBS was especially important in core currency pairs such as EUR/USD, USD/JPY, and EUR/CHF because it helped establish reference prices during periods of heavy institutional trading.

After the SNB announcement triggered a violent collapse in EUR/CHF liquidity, questions emerged about where the market had actually traded at the height of the panic. Some data feeds and brokers showed extreme prints, including quotes near 0.0015, implying an almost total collapse of the euro against the Swiss franc. EBS later stated that 0.8500 was the legitimate market low on its platform and described the 0.0015 quote as a “miss-hit,” meaning an erroneous or invalid trade indication rather than a true executable market price. ICAP also acknowledged that EBS Market had experienced “significant volatility” following the SNB decision.

The ICAP EBS issue matters because EBS was one of the major interbank FX venues for CHF trading. In a stressed OTC FX market, platforms like EBS do not merely report prices, they help define where bank and institutional participants believe the market actually traded.

During the volatility of January 15, EBS did not “fail” in the crude sense of going dark, but it failed at handling price discovery in a market where liquidity had effectively disappeared. On the same platform, EBS could confirm a legitimate market low near 0.8500 while also registering a “miss-hit” quote at 0.0015. For brokers downstream, this created brutal questions. Which prices are executable, which are erroneous, and which prices should be used for client stop-outs, hedges, and post-trade balance calculations? It became very difficult to distinguish real tradable prices from erroneous prints in a fragmented and chaotic market.

Retail platforms were several steps removed from the institutional market stress and had to absorb the fallout as it flowed down the chain. Brokers were pulling in prices from liquidity providers that themselves aggregated feeds from venues like EBS, bank pricing streams, and prime-of-prime sources. What showed up on the retail side was just a simplified interface: charts, order buttons, and stop-loss levels. Underneath that, brokers were dealing with rejected trades, liquidity disappearing mid-quote, “last look” rejections, and rapidly shifting reference prices. Once volatility settled, some retail accounts ended up in negative equity because execution had slipped far beyond their stop-loss orders.

Alpari UK Becomes a Headline Case

Alpari UK quickly became one of the headline cases. Just one day after the SNB announcement, the firm said it had entered insolvency because of the Swiss franc move. Alpari UK was the London-based arm of the Alpari brokerage group, offering retail foreign exchange and CFDs to individual clients and small institutions. It operated as a “retail FX broker,” meaning it sat between end-users and the interbank FX market, routing client orders to liquidity providers and managing margin, leverage, and execution.

On January 19, KPMG restructuring specialists were appointed as special administrators for Alpari UK, and the firm formally entered the Special Administration Regime. This action was taken under the UK’s financial services insolvency framework overseen by the Financial Conduct Authority (FCA), which is specifically designed for investment firms where client money and positions must be handled separately from the firm’s own assets.

Alpari UK became symbolic of retail broker fragility during the January 2015 Swiss franc shock because it was one of the most visible firms to collapse directly as a result of that event. For Alpari UK, the key issue was not just client losses but counterparty exposure and margin breakdown. In fast-moving forex markets, retail brokers typically rely on liquidity providers and internal risk controls to offset client positions. During the CHF shock, those hedges became unreliable or impossible to execute at expected prices. As a result, client losses exceeded account balances at scale, and the broker itself was left exposed to uncollectable negative balances.

The core insolvency mechanism was not mysterious. Clients had lost more than the money in their accounts and those negative client balances became receivables owed to Alpari UK. But a receivable is only useful if it can be collected, and it can be hard or difficult to collect due to a variety of reasons. Some clients simply do not have the money, some are in other jurisdictions which adds complexity, and some will dispute execution which drags out the process. Some may owe amounts large enough to ruin them personally but small enough that litigation is uneconomic for the firm.

Alpari UK illustrated a structural vulnerability in retail brokerage: firms could appear well-capitalized in normal conditions, yet still fail when markets gapped violently, liquidity vanished, and risk-transfer mechanisms broke down. Its insolvency and entry into the UK Special Administration Regime on January 19, 2015, marked one of the clearest cases where the retail forex infrastructure itself (and not just traders) was overwhelmed by extreme forex dislocation. The broker’s clients were insolvent at the account level. Their account level insolvency then became the broker’s balance sheet problem, and the broker became insolvent at the corporate level. After rescue talks failed, Alpari went into administration.

This is a point retail traders often miss. A broker is not automatically protected by the fact that clients owe money. A broker’s upstream obligations to prime brokers, liquidity providers, and hedging counterparties may be immediate, while collecting retail debts can be a slow, uncertain, and costly process. The mismatch can kill the firm.

KPMG’s administration process had to validate client money, client positions, negative balances, creditor claims, and possible recoveries. The FCA noted that the initial view in the early stages confirmed that client money had been held in segregated accounts and where safe, while the firm itself had reached the assessment that it was no longer solvent. That is the cleanest distinction between segregated client money and broker capital. Client money can be intact while the brokerage operating company is insolvent.

The 2020 Negative WTI Crude Event

The April 2020 WTI event was different from the Swiss franc shock, but just as useful for understanding negative balance risk. On April 20, 2020, the May 2020 NYMEX WTI crude oil futures contract settled at minus $37.63 per barrel. The Commodity Futures Trading Commission (CFTC) later described the event as the first time the West Texas Intermediate (WTI) contract had traded at negative prices since its listing. The CFTC report also pointed to the physical delivery terms at Cushing, Oklahoma, reduced crude demand, and storage stress as central conditions leading into the event.

The Lead Up

The April 20 event did not come out of nowhere, and the CME had already prepared the market for the possibility that certain energy contracts could trade or settle at zero or negative values. (The CME Group, through its NYMEX exchange, is the dominant and most influential marketplace for WTI crude oil futures.)

On April 3, CME announced operational changes to its systems so certain energy products could be flagged as “negative price eligible” and “negative strike eligible”. That notice also mentioned testing and system readiness in CME environments before actual live support for negative pricing.

On April 8, CME Clearing issued Advisory 20-152, stating that it had a tested plan to support negative underlying prices in major energy options and that it could switch pricing and margining options models from existing models to the Bachelier model. (The Bachelier model can handle negative underlying values without the log-based constraint that makes Black Scholes-style models unsuitable below zero.) The notice explained that Bachelier was already used in spread options where negative underlyings and strikes are regular. It also stated that CME message and file formats already supported negative futures and strike prices without modification.

So, not only was the market aware of the risk, but the CME was also preparing for the possibility of negative prices. On April 13, CME announced that firms could test negative and zero trade, settlement, and strike prices. On April 20, before WTI went negative, the CME Global Command Center notified NYMEX members that certain energy futures contracts, including WTI, would have no low limits and could trade at negative prices.

April, 20, 2020

On April 20, 2020, the May 2020 NYMEX WTI crude oil futures contract settled at minus $37.63 per barrel. The scale of the collapse shocked the market, but CME and its members had already been preparing for the possibility of negative prices. A futures price can be negative if the cost of accepting the deliverable commodity exceeds the value of owning it. A long holder near expiry is holding a contract that can require taking delivery. If storage is scarce and delivery obligations are real, the holder may have to pay someone else to take the contract away.

Consequences For Retail CFD Traders and Platforms

Many retail brokers offer cash-settled CFDs referencing WTI futures prices. These contracts are cash-settled, and no one is going to Cushing, Oklahoma, to deliver or receive barrels of oil. For years prior to April 2020, many CFD retail systems, risk screens, educational pages, and individual traders treated zero as the natural lower boundary for crude oil. April 2020 proved that the reference market could go below zero, and for many retail traders, this lesson got costly.

When the reference price for WTI futures dropped below zero, it exposed a product design vacuum. If a CFD references a futures contract that trades at minus $37.63, does the CFD price also become negative? If the platform’s terms say the CFD tracks the underlying reference market, the mathematical answer may be yes. But if the platform interface, risk disclosure, or product schedule had never clearly addressed negative prices, the client may argue that the contract economics were not properly specified.

This is where the phrase “cash-settled” can mislead. Cash settlement removes physical delivery, but it does not remove reference price risk. A trader who is long in CFDs referencing WTI does not need to take delivery of barrels of oil to lose money when the futures price turns negative. The broker calculates cash PnL from the reference price, and if the platform allows the reference price to pass below zero, a long client can suffer losses beyond the intuitive “price went to zero” boundary. For leveraged accounts without NBP, this can create a deficit.

Retail CFD brokers responded to April 2020 in various ways, and there are examples of brokers altering product specifications, switching references, closing positions, setting prices to zero, suspending trading, and/or applying special settlement rules. Those responses, predictably, created their own disputes. If a broker caps a product at zero while the underlying traded negatively, shorts will complain. If it passes through negative prices, longs will complain. If it closes positions preemptively, both sides will file complaints.

The deeper problem was model and infrastructure risk. Many trading and risk systems had been built around the assumption that commodity prices could not fall below zero. Margin engines, exposure calculations, stop-loss systems, charting software, and order management tools often behaved unpredictably near or below zero. Options models based on lognormal assumptions, such as Black-Scholes variants, also became unsuitable because they could not properly handle negative underlying prices. CME’s preparation to use the Bachelier model addressed this issue at the clearing level, but many retail CFD brokers and trading platforms discovered that their own systems were far less prepared.

For our discussion about negative balance protection, the lesson is clear. A famous benchmark can cross a boundary that retail traders think is impossible. If the product is leveraged and the account has no NBP, that account can drop far below zero. The April 2020 WTI event was not impossible, it only required the right combination of expiry mechanics, storage scarcity, financial holders unable or unwilling to take delivery, and a contract architecture that allowed prices below zero.

The August 2024 Volatility Spike and Yen Appreciation Episode

The August 2024 volatility spike and yen appreciation episode refers to a short period in early August 2024 when global financial markets experienced a rapid shift toward risk-off positioning, accompanied by a sharp strengthening of the Japanese yen (JPY). The move was not driven by a single event, but by a combination of macroeconomic data, shifting interest rate expectations, and crowded positioning in global assets. As volatility rose, leveraged investors and systematic strategies reduced exposure, contributing to declines in equities and other risk-sensitive assets. At the same time, the yen appreciated as carry trades (positions funded in low-yielding yen and invested in higher-yielding assets abroad) came under pressure.

This created feedback effects, where falling asset prices and rising volatility reinforced further deleveraging. Market liquidity was also thinner than usual due to seasonal August trading conditions, which amplified price moves across equities, rates, and foreign exchange markets. The August 2024 volatility spike and yen appreciation episode is best understood as a coordinated re-pricing of risk across multiple asset classes, where positioning, volatility dynamics, and funding currencies interacted simultaneously.

The trigger sequence began before August 5. The Bank of Japan had tightened policy, the JPY had started to strengthen, and weak US employment data increased concern about US growth. A stronger yen hurts yen-funded carry trades because the liability currency rises. Traders who had borrowed yen to buy higher-yielding or higher-beta assets suddenly faced losses on both sides: funding currency appreciation and falling risk assets.

On August 5, Japanese equities crashed. Reuters reported that the Nikkei 225 fell 12.4%, its worst percentage decline since the October 1987 crash, that the Nikkei 225 had wiped out 113 trillion yen in market value from its July peak, and that the yen had risen sharply versus the dollar.

Just as with the Swiss franc event and the WTI event, the lack of market depth on August 5 meant that having stop-loss orders in place was not enough to protect traders, as there were not enough opposing orders at each price level to absorb forced selling or buying. During calm periods, a large leveraged community can appear diversified. One fund holds Japanese equities, another holds US technology shares, a third is long in AUD/JPY or MXN/JPY, a fourth runs volatility controlled index exposure, and a fifth runs risk parity. The positions look different, but funding and volatility assumptions have a lot in common.

When the yen rose and the Nikkei fell, risk systems began cutting exposure. Volatility-targeting strategies reduce positions when realized volatility rises, and risk parity strategies reduce positions when asset volatility rises or correlations move against the portfolio. CTAs and macro funds respond to trend and stop levels, prime brokers issue margin calls and/or reduce financing appetite, and retail brokers widen spreads or raise margin. Every participant is doing something that makes sense on its own risk model or business rule. None of these actors are “panic selling” or being irrational, they are just following pre-set risk rules.

Volatility-targeting funds reduce exposure because volatility is rising and they must keep risk constant, risk parity funds rebalance because higher volatility or changing correlations increases portfolio risk and they mechanically de-risk, CTAs and macro funds cut positions because trends break or stop levels are hit, prime brokers reduce leverage and issue margin calls because client risk is increasing and they must protect themselves, and retail brokers widen spreads or raise margin for the same reasons. Together, however, they produce something that looks like a very powerful and coordinated selloff, even though no actual coordination or decision-making meeting has taken place between the various participants. Even though every participant is acting rationally and independently, their risk systems are similar enough that they all react to the same market stress at the same time, and this creates a sudden, synchronized sell-off.

At the account level, the Nikkei crash fed into cross-collateral liquidation because many leveraged accounts treat collateral at the portfolio level. A fund or active trader may not be forced to sell the losing instrument only. They may be forced to sell whatever is liquid, whatever position the model penalizes most, or whatever the broker demands. Losses in Japanese equities can therefore force reductions in pretty much anything else, including forex positions, US equity futures, index CFDs, and gold.

In this context, it is easy to understand how seemingly unrelated currency pairs can suddenly become related through margin. A trader long in AUD/JPY, long in NASDAQ CFDs, and short in USD/CHF might believe each trade has separate logic, but during a deleveraging shock, the broker sees one account, one equity figure, and several open exposures. If the Nikkei fall drives global risk aversion and yen strength, AUD/JPY can gap lower, NASDAQ can sell off, spreads can widen, and the account can breach margin across all positions at once.

Reuters quoted analysts saying that the meltdown in world equity markets was more reflective of a wind-down of carry trades used by investors to juice their bets than a hard and fast shift in the U.S. economic outlook. One Asian-based investor, who asked not to be identified, said that some of the biggest systematic hedge funds that trade in and out of stocks based on signals from algorithms, started selling equities when the previous week’s surprise Bank of Japan rate hike sparked expectations for further tightening. Mark Dowding, chief investment officer at BlueBay Asset Management, added that a number of macro funds had been caught the wrong way around on a trade and stops had been triggered, initially starting with FX and the Japanese yen.

Markets stabilized quickly after the August turbulence and outright dysfunction was avoided, but the event was severe, and pro-cyclical deleveraging and margin increases were strong amplifiers. That is exactly why the episode belongs in an NBP discussion. A market does not need to fully break to create retail deficits, it only needs to move fast enough, across enough correlated positions, while liquidity is thin enough, for stop outs to execute far from their trigger levels.

August 5, 2024, was therefore a stress test for the current retail trading stack, as it pushed every layer of retail trading infrastructure to its limits at the same time. It showed how a funding currency reversal can hit equities, forex, volatility, and leveraged portfolios at once, while also reminding retail traders that global market depth is not a constant; it vanishes when everyone needs the same exit. The event also showed why brokers with mandatory NBP must manage risk before the event, not after it.

The Bank for International Settlements (BIS) has discussed episodes of market turbulence, including those in 2024, in the context of tighter global financial conditions and the amplification of market moves through leveraged positioning, including FX-related leverage and other volatility-sensitive strategies in derivatives markets during periods of weaker US macroeconomic data and shifting interest rate expectations. The BIS emphasizes that FX positioning and carry trade exposure are not directly observable and must be inferred from proxy indicators, making their scale uncertain.

For more information and analysis:

- BIS Quarterly Review – “Carry off, carry on” (analysis of unwind dynamics). This is an earlier BIS Quarterly Review analysis on carry trade mechanics and unwinding dynamics, and it predates the August 2024-specific bulletin.

- BIS Bulletin 90: The market turbulence and carry trade unwind of August 2024. This bulletin is focused on the August 2024 episode and its market dynamics.

- BIS Quarterly Review (September 2024) – carry trades and cross-asset volatility amplification. This follow-up Quarterly Review analysis incorporates and expands on the August 2024 volatility episode.

Regulatory Frameworks and Jurisdictional Divergence

Why Jurisdiction Impacts the Real Maximum Loss For the Trader

The same trade can have different legal consequences depending on where the client is onboarded, how the client is classified, which entity holds the account, and which product is traded. A UK retail CFD account is not the same as a US retail forex account. An Australian retail CFD account is not the same as a Seychelles retail CFD account. In many jurisdictions, an account that is classified as a professional account falls under different trader protection rules than a retail account, even if both are large accounts doing leveraged trades.

Knowing who your contract partner is (the actual company, not just the brand name) and which jurisdiction that governs your trading account is very important, but many inexperienced traders treat it as unimportant paperwork until something goes wrong. Contract partner, client classification, and governing law set the real perimeter of risk when it comes to the possibility of a negative account balance. Platform branding is not enough. A broker group may operate one entity under the UK FCA, another under CySEC in Cyprus, another under ASIC in Australia, and another under the Vanuatu Financial Services Commission (VFSC). The website may look similar across entities, but the legal protection between offshore brokers and onshore branches can differ a lot.

Choosing your contracting jurisdiction dictates the baseline safety architecture of your account. Tier-1 regulatory frameworks operate on a principle of regulatory paternalism—they actively restrict client autonomy (such as enforcing strict leverage caps and mandatory NBP) to protect retail accounts from extreme market hazards. Conversely, lower-tier or offshore jurisdictions lean heavily toward a caveat emptor model, granting maximum operational liberty but shifting the entire structural and credit risk onto the trader.This divergence is the defining factor in how negative balances are handled globally. Both models present distinct structural trade-offs: experienced participants must choose between the secure, liability-capped framework of top-tier regimes and the superior capital efficiency—but asymmetric risk profile—of offshore jurisdictions.

Brief Regulatory NBP Comparison

Across jurisdictions, negative balance protection exists on a spectrum rather than as a universal rule. Some of the strongest and most standardized protections are found in the UK and EU retail CFD frameworks, followed by Australia’s product intervention-based system. The United States does not provide negative balance protection for retail leveraged trading, while Canada sits somewhere between the EU/UK model and the US model, but in a less uniform way because regulation is provincial (plus IIROC/CIRO rules for investment dealers) rather than a single federal retail regime.

| Jurisdiction / Regulator | NBP Status for Retail CFDs | Core Regulatory Mechanism / Source | Professional Account Opt-Out? |

|---|---|---|---|

| United Kingdom (FCA) | Mandatory | PS19/18, COBS 22.5 | Yes (Loss of NBP protection) |

| European Union (ESMA / National) | Mandatory | National measures (BaFin, CySEC) via MiFIR | Yes (Elective Professional) |

| Australia (ASIC) | Mandatory | Product Intervention Order (Extended to 2027) | Yes (Wholesale Client classification) |

| United States (CFTC / NFA) | Prohibited | 17 CFR § 5.16 (Explicitly bans loss guarantees) | N/A (Standard margin collection applies) |

| Canada (CIRO / Provincial) | Conditional / Varied | Risk control framework (No federal baseline) | Varies by provincial registration |

- United Kingdom / FCA

In the United Kingdom, negative balance protection for retail CFD clients is effectively mandatory under the Financial Conduct Authority’s (FCA) product intervention regime introduced following PS19/18. This framework aligns with earlier ESMA-style restrictions and is implemented through FCA conduct and product rules rather than a single standalone “NBP statute”.

Retail clients trading CFDs and similar leveraged derivatives are protected from losing more than the funds in their account under normal market conditions, while elective professional clients may opt out of these protections in exchange for broader market access and higher leverage. Enforcement is carried out through FCA supervisory powers, and retail clients may also have access to the Financial Ombudsman Service for eligible disputes.

- European Union / ESMA and National Regulators Under MiFID II

In the European Union, negative balance protection for retail CFD clients originates from ESMA product intervention measures first introduced in 2018 and later adopted and maintained by national competent authorities such as BaFin, AMF, CySEC, and others. These rules apply primarily to CFDs and certain other leveraged retail derivatives, imposing leverage limits and requiring negative balance protection for retail clients.

Professional clients under MiFID II classification do not benefit from these retail protections, as they are deemed to have sufficient experience and risk tolerance to operate without them. Enforcement and dispute resolution occur at the national regulator level rather than through a single EU-wide complaints body.

It is important to note that MiFID II itself is the framework legislation, while negative balance protection is implemented through ESMA and national regulatory interventions rather than being explicitly defined as a core MiFID II provision.

- Australia / ASIC

In Australia, the Australian Securities and Investments Commission (ASIC) enforces CFD product intervention measures that significantly restrict leverage for retail clients and impose risk controls that reduce the likelihood of retail traders losing more than their account balance in normal market conditions. These rules apply to retail over-the-counter (OTC) CFDs as a product class, including FX CFDs, and are implemented through leverage caps, margining requirements, and mandatory margin close-out mechanisms rather than a standalone statutory NBP rule.

Dispute resolution is available through the Australian Financial Complaints Authority (AFCA), which handles eligible retail client complaints involving licensed financial service providers.

- United States / CFTC and NFA

In the United States, there is no regulatory requirement for negative balance protection for retail forex or futures trading. Instead, retail clients trading leveraged products such as forex and futures are subject to margin rules that allow for losses beyond deposited funds under certain market conditions.

While brokers operate under strict regulatory oversight by the CFTC and NFA, there is no guarantee of limiting losses to the account balance. Negative balances, where they occur, are typically recoverable by brokers under account agreements, and disputes may be handled through arbitration or litigation, depending on the contract terms and regulatory venue.

- Canada / CIRO and Provincial Securities Regulators

In Canada, NBP is not implemented as a single, explicit nationwide statutory rule for all retail leveraged trading products. Instead, protections for retail clients arise through a combination of securities regulation, investment dealer obligations, and risk controls imposed on firms regulated by the Canadian Investment Regulatory Organization (CIRO, formerly IIROC) and overseen by provincial securities regulators such as the Ontario Securities Commission (OSC) and other provincial authorities.

Dispute resolution for investment dealer clients is generally available through CIRO complaint processes and may also involve escalation to provincial securities regulators or ombud services where applicable.

European Union: ESMA, MiFID II, and National-Level Regulation in the Membership Countries

ESMA’s 2018 CFD Product Intervention Measures

ESMA’s 2018 CFD product intervention measures brought NBP into the European retail CFD rule set. ESMA said the measures would ensure, for the first time, that investors could not lose more money than they put in, while also restricting leverage and incentives. ESMA’s technical Q&A clarified that NBP limits the retail client’s aggregate liability for all CFDs connected to a CFD trading account to the funds in that CFD trading account.

ESMA’s reference to the “CFD trading account” is important because it suggests that the protected CFD account, rather than the client’s entire relationship with the broker group, is the primary unit of risk for the purpose of the ESMA negative balance protection framework. However, the practical application can become more complex depending on the account structure and contractual arrangements involved.

There is currently limited publicly available case law providing definitive judicial interpretation of how these account-level boundaries should operate in all situations under the ESMA framework. As a result, traders should not automatically assume that all accounts held within the same broker group are completely insulated from one another in every possible scenario involving a negative CFD account balance. Depending on the jurisdiction, contractual terms, account setup, and whether accounts are legally linked through cross-collateralization or set-off provisions, there may be circumstances in which a broker can transfer or offset funds from another account held by the same client. This can become particularly relevant where a client holds multiple products, wallets, or account types with the same broker or affiliated entities. Future court decisions, regulatory guidance, or enforcement actions may provide a clearer interpretation of how account segregation and liability allocation should operate under the ESMA retail CFD protection framework.

National Measures

After ESMA’s temporary intervention, national competent authorities across the EU moved to national measures. The details of these laws and regulations can vary, but the core retail CFD pattern is familiar: leverage caps, margin close-out rules, standardized risk warnings, incentive restrictions, and NBP.

The wording of the ESMA intervention remains highly relevant because the current national rules in EU member states are not entirely independent creations. They are largely derived from, modeled on, or intended to preserve the substance of the original temporary intervention measures adopted by ESMA under the MiFIR product intervention framework. The temporary ESMA intervention expired formally, but the national regulators subsequently implemented substantially similar permanent measures at the domestic level. As a result, the original ESMA wording, rationale, and interpretive approach still matter for several reasons, including the custom of interpretative continuity and the underlying policy.

MiFID II Passporting and National Enforcement Across the EEA

Within the EU and in the wider European Economic Area (EEA), retail trading regulation is complicated by passporting. An investment firm properly regulated in one of the EEA countries can provide investment services across the entire EEA under MiFID II once it has completed the correct passport notification process.

Example: Broker XYZ is based in Cyprus and licensed by the Cyprus Securities and Exchange Commission (CySEC). Broker XYZ can legally provide investment services across the entire EEA under MiFID II once it has completed the correct passport notification process. The firm’s home regulator remains CySEC, but the firm can serve clients in states such as Germany, France, Spain, Italy, Norway, and others without obtaining a separate full licence in each country. These countries, which are not the broker’s home countries, are called host countries.

Under MiFID II, passporting is not automatic and it requires a formal notification process. An investment firm must inform its home competent authority of the specific investment services and activities it intends to provide, the financial instruments involved, and the EEA host states where it plans to operate. While the notification is submitted through the home regulator, it is structured so that each intended host state and service profile is clearly identified. In practice, this means firms cannot rely on a vague or undifferentiated “all-EEA” notification. Instead, passporting permissions are recorded and processed on a per-host-state and per-service basis, ensuring that cross-border activity is properly scoped and supervised.

The home state and host state split creates the real compliance nuance. CySEC supervises the Cyprus firm as the home regulator. But host national competent authorities, such as BaFin in Germany or the AMF in France, still have powers over marketing, consumer protection, local product intervention measures, and enforcement where services are directed into their territory.

ESMA’s 2018 temporary intervention created the baseline retail CFD package with leverage caps, margin close-out on a per-account basis, negative balance protection on a per-account basis, incentive bans, and standardized risk warnings. ESMA stated that the measures would ensure that retail investors could not lose more money than they had in the account.

When ESMA’s temporary measures expired, national competent authorities adopted their own permanent or semi-permanent local measures. BaFin issued a General Administrative Act restricting CFDs marketed, distributed, or sold to retail clients in Germany. The AMF in France adopted its own decision, restricting the marketing, distribution, or sale of CFDs in France or from France to retail investors. Each member of the EEA adopted its own similar, but not identical, regulation concerning retail CFDs.

The result is not pure uniformity. The core protections are harmonized because most national measures reflect ESMA’s model. But local authorities can enforce their own product intervention wording, advertising restrictions, language requirements, warnings, and perimeter views.

For a trader, the practical issue is the onboarding entity (broker home country), plus the target country (broker host country). A German resident onboarded by a CySEC firm may still be covered by German product intervention rules if the product is marketed or distributed into Germany. A French resident may encounter AMF rules layered on top of the broker’s CySEC status. The legal entity remains Cyprus-based, but the host market is not a legal vacuum.

United Kingdom: FCA Rules

The UK made permanent restrictions on CFDs and CFD-like options sold to retail clients through the FCA Policy Statement PS19/18, published on July 1, 2019. The FCA stated that it finalized rules restricting how CFDs and CFD-like options are sold, marketed, and distributed to retail consumers, with PS19/18. Notably, the FCA’s policy materials include mandatory NBP as part of the retail CFD framework.

Just as within the EEA, the UK model is based on client classification, where retail clients receive a much higher level of protection than professional clients. A trader who goes through the process of changing their classification from retail to professional is not just changing leverage caps and margin ratios, they are losing their mandatory NBP. In practical terms, they are changing who eats the loss if their account drops below zero due to a tail event.

The FCA approach also draws a line around covered products. NBP is not a universal promise across every possible financial activity. It applies through the relevant conduct and product intervention rules. A trader should check the exact product, account type, and entity.

FCA PS19/18 Analysis: How the UK Made Retail CFD Protections Permanent

The FCA used its rule-making and product intervention powers under the Financial Services and Markets Act 2000 (FSMA) to make the UK’s negative balance protection regime for retail CFDs permanent.

The legal base for the mandatory NBP starts with FSMA section 137A, which gives the FCA power to make general rules applying to authorised persons. Section 137D then confirms that the FCA’s general rule-making power includes product intervention rules. Those rules may prohibit authorised firms from doing specified things, or from doing them unless conditions are met, in relation to specified products or product features. FSMA therefore gives the FCA a route to move beyond firm-by-firm supervision and impose a market-wide restriction on how a product is sold, distributed, and structured.

That distinction matters. In the UK, a normal supervisory letter tells firms what the regulator expects. A Handbook rule changes the legal operating conditions for all firms in scope. PS19/18 was the policy statement through which the FCA finalized permanent restrictions on CFDs and CFD-like options sold to retail clients. The FCA published PS19/18 on July 1, 2019, stating that it had finalized rules restricting how CFDs and CFD-like options are sold, marketed, and distributed to retail consumers.

The mechanism sits in the FCA Handbook, mainly in COBS 22.5. The rules require retail CFD providers to limit leverage by asset class, use close-out orders for positions when funds fall to the prescribed margin close-out level, provide negative balance protection, stop offering monetary or non-monetary incentives to encourage trading (e.g. welcome bonuses), and deliver standardized risk warnings. PS19/18 made the UK regime broadly consistent with ESMA’s temporary intervention, but it also widened the UK perimeter to capture CFD-like options, including products with similar economic exposure.

The negative balance protection part is not a soft suggestion; it is embedded as a conduct rule for firms dealing with retail clients in covered products. In practical terms, the firm must ensure that a retail client cannot lose more than the total funds in the relevant CFD account. That creates an account level liability cap. It does not guarantee a stop price, and it does not stop slippage, but it allocates the shortfall to the firm once the account is exhausted.

In the FCA’s cost benefit discussion for PS19/18, the FCA estimated that negative balance protection would save retail consumers about £6 million per year. The larger expected consumer savings came from leverage restrictions, but NBP addressed the more severe tail event, which is a loss greater than the account balance. In total, the FCA estimated that the overall consumer benefit from its CFD restrictions would be roughly £267 million to £451 million annually, with leverage restrictions accounting for the overwhelming majority of those savings.

Australia: ASIC Product Intervention

The Australian Securities and Investments Commission (ASIC) has introduced retail CFD product intervention measures that include leverage limits, margin close-out standardization, and protection against negative account balances. The formal production intervention order was issued in October 2020 and the measures took effect on 29 March, 2021.

ASIC intervention measures are not permanent, and in October, 2021, ASIC proposed an extension of the order. As a part of their proposal, the commission showed that NBP had actually prevented negative liability outcomes for retail traders, which moved NBP from theory to observed protection. In Consultation Paper 348 (CP 348), released on 18 October 2021, ASIC reported that during the early operation of the order, the NBP had prevented at least 1,311 retail client accounts from incurring a liability greater than the funds in the account.

ASIC’s argument makes the connection between leverage restriction, margin close-out rules, and NBP clear. Leverage limits reduce the probability and size of a deficit before it appears. NBP protects the client after a deficit. Margin close-out rules sit between those two layers. That three-part structure is more dependable than a broker saying “we’ll protect you” while offering extreme leverage and no NBP.

ASIC eventually extended the CFD product intervention order for five years, and the currently active extension runs until May 23, 2027.

United States

Forex and the CFTC Environment

The United States legal environment is very different from the solutions used in the EEA, UK, and Australia. Under 17 CFR § 5.16, retail forex dealers, futures commission merchants, and introducing brokers may not represent that they will guarantee a customer against loss, limit the customer’s loss, or not call for or attempt to collect required margin or deposits in covered retail forex accounts. 17 CFR § 5.16 is part of the Commodity Futures Trading Commission (CFTC) retail forex regulations under the Code of Federal Regulations.

For US traders, the implication is blunt. These margin systems are designed to reduce risk, not to cap it at account balance level. If an account goes negative during a gap, the firm may pursue collection according to the account documents and applicable dispute process.

This is not just absence of mandatory NBP, 17 CFR § 5.16 is a prohibition on making any kind of guarantee that is or resembles NBP in covered retail forex. US policy makers do not want firms using guarantees against loss as a sales tool or as a way to distort customer understanding of margin obligations. In an enforcement context, the CFTC has repeatedly alleged that guarantees or limits on customer loss are violations of 17 CFR § 5.16.

CFTC policy and the 17 CFR § 5.16 rule are often quoted when NBP is discussed in a U.S. context, but it is important to keep in mind that 17 CFR § 5.16 is specifically a retail forex regulation, not a general rule covering all retail trading in the U.S. The rule is part of the CFTC retail forex framework in Part 5 of Title 17 of the Code of Federal Regulations, and it applies to retail foreign exchange transactions and entities participating in that market, including retail foreign exchange dealers (RFEDs), futures commission merchants (FCMs), introducing brokers (IBs), and certain affiliated persons.

Importantly, the fact that an entity is an IB does not mean the rule automatically extends to all products that the broker may touch. The scope of § 5.16 is tied to covered retail forex accounts and transactions. It covers forex trading and commodity/derivatives-related retail forex activity under CFTC jurisdiction.

Commodities and the CFTC Environment

For retail leveraged commodity speculation in the U.S. (CFTC-regulated futures and commodity options), NBP is not mandatory but it is not explicitly banned either. There is no rule requiring brokers to offer it, and no rule broadly prohibiting it across all commodity trading. Instead, the system is built so that NBP is generally not expected or structurally embedded. For leveraged retail commodity speculation in the U.S., losses beyond account balance are legally possible, structurally expected, and enforceable.

Standard marketing rules apply, of course, and brokers are not allowed to guarantee protection from losses in a fraudulent or misleading way, as that would violate the CFTC anti-fraud and anti-misrepresentation provisions.

Equity Trading

Equity trading in the U.S. is primarily regulated under the Securities and Exchange Commission (SEC) framework, the Financial Industry Regulatory Authority (FINRA) rules, and Federal Reserve margin rules such as Regulation T. The short answer is that there is no U.S. rule that mandates NBP for retail equity trading, and retail equity traders in the U.S. are fully liable for deficits in their trading accounts, in accordance with the account agreement. Margin trading is governed by Regulation T (initial margin rules) and by FINRA (margin maintenance rules). Retail accounts can go negative and brokers have legal tools to collect deficits.

A marketing promise or contractual promise of “no losses beyond account balance” could conflict with a broker’s risk obligations, capital requirements, and the margin lending structure rules. True NBP is not offered as a standard retail feature in securities margin trading in the U.S.

Sometimes brokers absorb losses due to system errors, execution failures, or discretionary loss forgiveness, but that is not NBP.

Canada

In Canada, protections for retail traders arise through a combination of securities regulation, investment dealer obligations, and risk controls imposed on firms regulated by CIRO (formerly IIROC) and overseen by provincial securities regulators.

For leveraged products offered by CIRO-regulated investment dealers, risk is primarily managed through margin requirements, real-time risk monitoring, and forced liquidation mechanisms. These systems are designed to reduce the likelihood of clients owing more than their account equity, but there is no universal NBP comparable to the explicit retail CFD frameworks seen in the UK and EU/EEA.

Where leveraged OTC products such as CFDs are offered in Canada, they are typically subject to strict regulatory constraints, and in practice may include broker-level protections that function similarly to NBP. However, the presence and scope of such protections can vary depending on factors such as product type, the regulatory status of the firm, and whether the account is held with a CIRO-regulated dealer or another type of registered entity.