Market Timing: A Risky Gamble or a Calculated Strategy?

Trading is full of ideas about how to improve results. Few of them get argued about as much as market timing.

Market timing means trying to predict the ups and downs of a market.

You buy when you think something is cheap or about to climb, and you sell when you think it’s run far enough or is about to drop. Done well, it sounds close to perfect. You sidestep the declines and you own the rallies.

The pull is obvious. Who wouldn’t want to buy the exact bottom and sell the exact top? For a day trader or a swing trader, that’s the whole dream.

But it’s not so simple. Predicting short-term price moves with enough accuracy to do it over and over is one of the hardest things in finance.

The amount of information and data and number of players moving markets with their own goals and motivations is incomprehensible.

Economic data, earnings, positioning, central bank decisions, politics, war, weather, psychology and human emotion, and various other factors are interacting.

Getting the direction right often enough to beat your costs and the people on the other side of your trades (who are very likely to be sophisticated) is rare. Even full-time professionals with better data, better analysis, faster systems, and bigger research budgets struggle to do it.

Timing isn’t useless, but it’s a high bar.

Here we go through how short-term timing actually works, where the edge comes from when it exists, why most people who try it lose, and how to think about it next to the slower, duller approach.

Key Takeaways – Market Timing

- Market timing is exceptionally difficult – The potential rewards of successful market timing are what draw traders to the strategy. But even professionals struggle to consistently predict short-term market swings accurately. It’s a zero-sum game (negative-sum when factoring in transaction costs).

- Missed opportunities are costly – Trying to time the market often means missing out waiting for the “perfect” entry point.

- Markets are discounting mechanisms – It’s not whether things are “good” or “bad” that influences asset prices but how things transpire relative to what’s already discounted in. This also makes market timing a difficult thing to do.

- From the competing domain of investing – We show that market timing is not nearly as influential as people think. The difference between perfect timing and absolute worst timing is not that large relative to the effect of consistent contributions.

What market timing really is

Timing is a bet about direction and the clock.

You’re saying: this price is going to move this way, within this window, far enough for me to act on it and get paid.

- A day trader does this on a scale of minutes and hours.

- A swing trader works over days or weeks.

- A more tactical-oriented investor might do it over months.

The timeframe changes, but the idea’s the same. You believe you know something about the near future that justifies moving in or out right now.

Compare that to the other camp, the buy-and-hold crowd. They aren’t claiming to know what next week looks like. They’re betting that over years, businesses earn more, economies grow, and prices follow.

They accept every drop along the way because they aren’t trying to dodge any of them in the first place. They’re also generally cost- and tax-conscious, whereas for day traders and shorter-term traders that’s a secondary consideration.

Both groups are trying to make money in their own ways. They just have their own approaches about whether short-term moves can be predicted well enough to be worth chasing.

Most of the evidence sides with the second group, and it’s worth understanding exactly why before you decide which one you want to be.

The first thing to understand: the price already knows what you know

This is the part that trips up most new traders.

Everything that’s known is already discounted into the price.

What a price reflects is how things are turning out – or what’s newly discounted – relative to what was already expected, not simply whether the underlying company or economy is good or bad.

The current price already holds the combined view of everyone trading it, with all the public information baked in. The market is a discounting machine. It prices in the dollar-weighted consensus.

Ben Graham, the famous security analyst and Buffett mentor, called the market a voting machine in the short-term (i.e., what people think) and a weighing machine (i.e., reality) in the long-term.

The discounting process has an important implication. Good news doesn’t make a price go up. Good news that beats what people already expected makes a price go up. If a company is widely loved, and everyone assumes it will crush its earnings, and then it merely does well, the stock can fall on the report. The good result was already in the price. What moves the price is the surprise, the gap between what happens and what was discounted in.

You see this every earnings season. A company posts record profits, the headline looks great, and the stock drops 8% because the number traders quietly expected was even higher and that “even better” result was factored into the price.

New traders find this baffling. It stops being baffling the moment you accept that you’re trading against expectations, not against reality.

So when you decide to buy because the story sounds great, ask yourself a hard question. If the story is obvious to you, it’s obvious to the millions of other participants too, and it’s already in the price.

You don’t get paid for knowing what everyone knows. You get paid for being right about what the crowd has wrong.

To win, you have to bet against the consensus and be right. Betting against the consensus is uncomfortable by definition, because the consensus feels obviously correct in the moment. And being right about the surprise, repeatedly, after costs, against faster competitors, is the actual job.

Most people skip straight to “I have a view” and never ask whether their view is already priced.

Alpha vs. Beta

Alpha – or making money in excess of a representative benchmark – is a zero-sum game. Costs make it negative-sum.

The return of just owning the market is called beta. You get beta by buying a broad index and sitting still.

It’s cheap, it’s passive, and historically the US stock market has handed it out at roughly 7 to 10 percent a year over long stretches, with plenty of volatility and double-digit-percentage falls mixed in along the way.

Every time you try to beat the index by timing or stock picking, you’re chasing alpha. Here’s the catch most people never sit with. Across all active participants combined, alpha is zero-sum.

For every trade where someone buys low and sells high, someone else sold low and bought high. The market’s total return is set by beta. The active players are just rearranging who gets which slice. Before costs, the active crowd as a group earns exactly the market return, no more.

Then costs show up. Commissions, the bid-ask spread, slippage, financing on margin, and taxes. After all of that, the active crowd as a group earns less than the market.

Active trading, in aggregate, is a negative-sum game.

So when you sit down to day trade, you’re voluntarily entering a contest where the average participant loses relative to a person who did nothing.

To come out ahead, you don’t just need to be good.

You need to be good enough to beat the average player, cover your costs, and take money from someone better-resourced sitting on the other side of your trade.

That someone is often a firm with better tech, better data, better and more information, and lower costs.

Why it’s so hard to do consistently

A few forces stack against the short-term timer, and they compound on each other.

The competition is brutal. When you place a trade, you aren’t trading against “the market” in some abstract sense.

You’re trading against whoever took the other side. A lot of the time, that’s a high-frequency trading firm or a professional desk running infrastructure you can’t match.

They see order flow faster, they pay almost nothing per trade, and they’re running models you don’t have.

Brazilian Study

A University of São Paulo study put it bluntly: the researchers concluded it’s virtually impossible for an individual to compete with high-frequency traders, despite what the trading-course sellers promise.

The data on retail timing is grim. That same study, by Fernando Chague, Rodrigo De-Losso, and Bruno Giovannetti, tracked every person who started day trading Brazilian equity futures between 2013 and 2015 and stuck with it for more than 300 days.

Of those who persisted, 97 percent lost money. Only 1.1 percent earned more than the Brazilian minimum wage. Only half a percent earned more than a bank teller’s starting salary. The single best trader in the whole group averaged about $310 a day, but with swings so wild the risk dwarfed the reward. And the researchers found no sign that people got better with practice. The ones who kept trading just kept losing.

Taiwan Study

Taiwan tells the same story over a longer window. Brad Barber, Yi-Tsung Lee, Yu-Jane Liu, and Terrance Odean studied every trade on the Taiwan Stock Exchange from 1992 to 2006.

Fewer than 1 percent of day traders earned reliable, statistically real profits after fees. In a separate and now-famous US study titled “Trading Is Hazardous to Your Wealth,” Barber and Odean found that the most active 20 percent of retail traders underperformed the market by about 6.5 percentage points a year once costs were counted. Over time, that gap compounds into a small fortune left on the table.

Variance can trick you

Variance hides the truth. Markets are noisy enough that you can be wrong and still win for a while, or right and still lose for a while.

A trader can have a genuinely bad process, string together a few profitable weeks by luck, and feel like a genius right before it falls apart. The randomness makes it very hard to tell whether your results come from skill or chance until a long time has passed, and most accounts don’t survive long enough to find out.

You have to be right twice. This one gets underrated. To time a move, you don’t just need to pick the exit. You also have to pick the re-entry.

Sell before a drop and you feel brilliant, but now you’re sitting in cash and you have to decide when to get back in.

Get that wrong and you miss the bounce, which is often sharper and faster than the fall that scared you out. Two correct calls, back to back, and then again, and again. The odds of doing that consistently are slim.

The advantages of market timing

Despite what we’ve covered so far, there are real and potentially viable reasons people choose to time the market.

Higher returns when it works. This is the whole draw. Buy low, sell high, repeat, and you can outrun a buy-and-hold investor by a wide margin.

The math of a good timer compounding faster than the index is genuinely attractive. The word doing all the heavy lifting in that sentence is “good,” and good is rare.

The chance to dodge drawdowns. A timer who actually reads a downturn coming can move to cash or bonds, or short the move, and protect capital while everyone else rides it down.

Sitting out a 30% decline and buying back lower is worth a lot. Whether you can reliably see the decline coming and act on it is the open question, but the value of doing so is real and large.

Short-term opportunities do exist. Markets throw off temporary mispricings, momentum runs, and patterns that a sharp, well-prepared trader can sometimes catch.

Volatility creates openings. A trader watching closely can occasionally turn a fast move into a quick, large gain in a way a passive holder never will.

These reasons are perfectly viable. They’re just hard to harvest after costs and competition take their cut.

The disadvantages of market timing

Set against those advantages are problems that hit almost everyone who tries.

Difficulty, first and always

This is the big one. The accuracy you need to consistently buy low and sell high is enormous, and the system you’re trying to predict is shaped by countless economic, political, and other forces interacting in real time.

Even pros with every advantage find it difficult. The base rate of success is low, and it stays low.

Missed time in the market

Every time you step out, you risk being absent for the best days. And the best days have a nasty habit of showing up right next to the worst ones. A JP Morgan analysis makes this concrete.

Picture putting $10,000 into the S&P 500 at the start of 2005 and leaving it alone through the end of 2024. You’d have ended up with about $71,750, a 10.4% annual return. Miss just the 10 best days over those two decades, the kind of days you’d likely sit out if you’d panicked and sold, and you’d be left with about $32,871. Less than half. Miss the 60 best days and your return turns negative, leaving you with less than you put in.

Why does stepping out cost so much? Because the best days cluster around the worst ones. In JP Morgan’s data, seven of the 10 best days over those 20 years happened within two weeks of the 10 worst days.

In March 2020, at the start of the COVID crash, the market had its second-worst day of the year on the 12th, and then its second-best day of the year on the very next session. If fear pushed you out on the worst day, you very likely missed the snapback right behind it. That’s the trap.

The moments that scare you out and the moments that make your decade are neighbors.

Trading costs add up fast

Every buy and sell (commonly called a round trip) carries a cost, even in a zero-commission account, because you pay the spread and you lose a little to slippage.

The more you trade, the more these bleed your returns.

Picture a trader doing 10 round-trip trades a day, roughly 2,500 a year. If each round trip costs just 0.05% of the position to spread and slippage, and the position is around $20,000, that’s $10 a trade and $25,000 a year in friction alone, before a single dollar of profit.

Then there’s tax. In the US, gains on positions held a year or less are short-term, and they get taxed as ordinary income, which can run as high as 37% for top earners. Long-term gains are taxed at lower rates.

A frequent trader hands a bigger share of every win to costs and the tax authority than a buy-and-hold investor does, which means the trader has to be right by a wider margin just to break even with the person sitting still.

The emotional toll is real and it costs money

Short-term trading is stressful. Watching every tick, holding losing positions, deciding in seconds, it grinds people down.

Stress drives bad decisions, and the bad decisions follow a predictable shape. People hold losers too long because selling feels like admitting they were wrong, and they sell winners too early to lock in the small relief of a gain.

Odean’s research on thousands of brokerage accounts found exactly this, traders realizing gains far more often than losses, which is backwards from what makes money.

The strategies traders actually use

People time markets in a few recognizable ways. None of them is a cheat code, and each of these approaches have a built-in weakness worth knowing before you lean on it.

Technical analysis

Technical traders read price action.

They study charts, trends, volume, and indicators like moving averages, support and resistance, RSI, and MACD, looking for signals to buy or sell. The bet is that past patterns hint at future moves, because human behavior repeats.

There’s something to it. Levels where lots of orders sit genuinely can matter, and momentum is a real, documented effect.

But two things cut against pure chart-reading.

First, the more popular a pattern gets, the more it gets traded away, because everyone sees the same lines and the edge erodes.

Second, a pattern that “works” 55 percent of the time still loses 45 percent of the time, and after costs that thin edge can vanish. Technicals can tilt the odds slightly in some cases. But there’s no certainty.

Fundamental analysis

Fundamental traders look at the underlying value.

They study earnings, balance sheets, growth, and the wider economy, then compare that estimate of worth to the current price.

If the price looks low against the value, they buy. If it looks high, they sell or stay away.

A simple version shows how personal this gets.

Say a stock earns $4 a share a year. A trader who needs a 10% annual return would pay up to about $40 for it before factoring for growth, because 4 divided by 0.10 is 40.

A trader who’s happy with 7% would pay around $57 (also not accounting for growth), because 4 divided by 0.07 is roughly 57.

Same company, same earnings, two very different “fair” prices, depending entirely on what return the buyer demands.

That’s part of why two smart people can study the same stock and disagree completely. Value is ultimately a judgment, not a fact, and the market’s judgment can stay different from yours longer than your account can stand it.

Contrarian trading

Contrarians do the opposite of the crowd. When everyone’s euphoric and buying, they sell. When everyone’s terrified and dumping, they buy. The idea is that crowds overshoot in both directions, and the extremes eventually get corrected.

This lines up with the discounting logic from earlier. The crowd’s view is already in the price, so the money is in betting against it when it’s stretched too far.

But there’s a catch, and it’s a big one. Knowing the crowd is wrong is not the same as knowing when it’ll stop being wrong. For example, Tesla stock has been very overvalued for many, many years, but a correction never came.

Things that look insanely overpriced can get more overpriced for a long time, and falling assets can keep falling well past the point of reason.

Buying when everything is red, while every voice/pundit screams that it’ll get worse, is one of the hardest things to actually do. Most people can’t pull the trigger, and the ones who do often do it too early and bleed out before they’re proven right.

Sector rotation

This one moves money between parts of the economy depending on where you think the cycle is heading.

The classic move: lean into defensive sectors like consumer staples and utilities when you expect a slowdown, then rotate into growth areas like technology when you expect an expansion, since easier money and lower rates tend to help longer-duration, higher-growth companies more.

It’s a reasonable framework, and the cyclical patterns behind it are real. The trouble is timing the rotation.

The market usually starts pricing the next phase of the cycle before the data confirms it. As we covered, markets are always discounting ahead.

So by the time a slowdown is obvious in the numbers, the defensive trade is often already crowded and the next rotation is forming. You’re back to the same problem. To win, you have to move ahead of the consensus, not alongside it.

Market timing versus time in the market

This is the old debate, and it’s worth framing honestly rather than as a bumper sticker.

Timing, as we’ve covered, tries to add return by getting in and out at the right moments. Time in the market does the opposite.

It says don’t try to predict the wiggles, just stay invested and let the long-term climb do the work. You ride the drops because you’re not trying to dodge any of them, and you collect the recoveries because you were there for them.

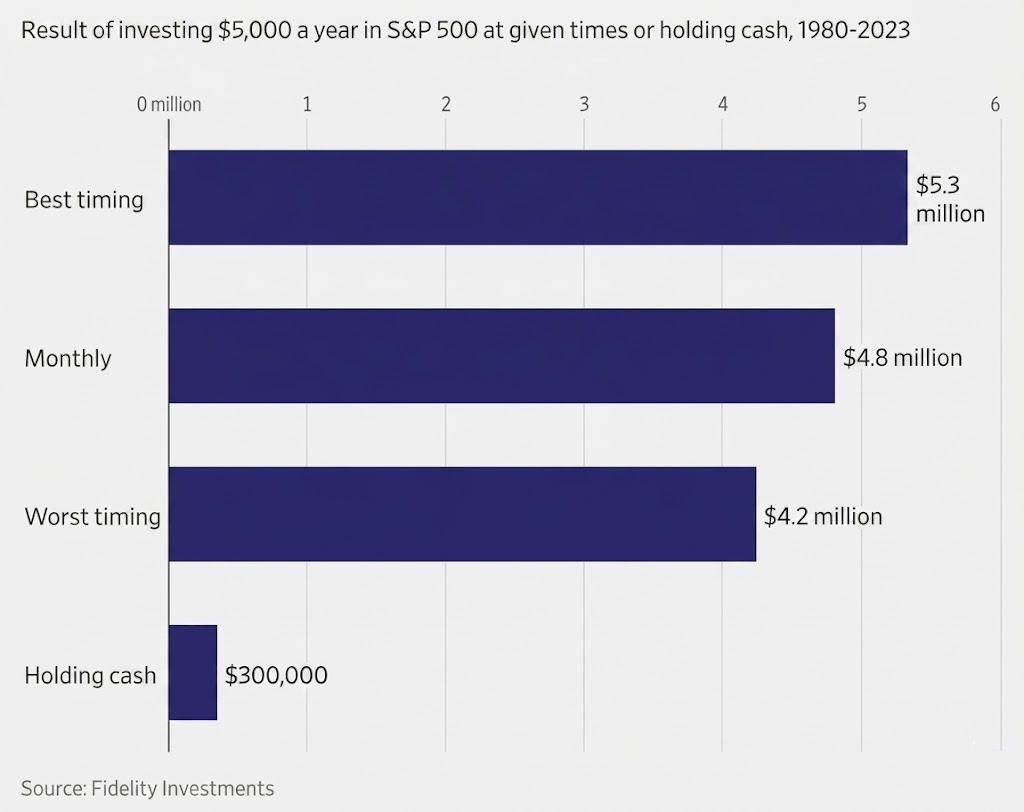

Historical data for the 1980-2023 period, if investing $5,000 per year into an S&P 500 fund, show that even under the “worst timing” for market entry, an investor could reach $4.2 million, whereas “monthly” contributions could result in $4.8 million, and “best timing” could reach $5.3 million. Simply holding cash yields only $300,000.

For some, the most surprising statistic would be the cash lagging the stock markets.

But for our purpose here, it shows just how more or less unimportant market timing was here.

Overall, it shows that the primary risk to wealth over decades is not market fluctuation, but rather the failure to capture market growth.

Middle path

There’s also a middle path that a lot of thoughtful traders actually use, and it’s probably the most sensible setup for most people who want to trade.

Keep the large majority of your money in a boring, diversified core that you don’t touch, then trade a small slice.

Something like 80%-90% in a steady mix of index funds and bonds, and 10%-20% that you actively trade. This is a barbell.

The big, safe end carries your long-term wealth and compounds quietly. The small, active end is where you express your views and scratch the trading itch, and if you blow it up, you haven’t blown up your future.

The idea behind the barbell is that it separates two jobs that shouldn’t be mixed. Your long-term financial security should never depend on you being right about next month.

And your trading should be sized so that a bad run is survivable rather than life-changing.

Most people who get hurt unfortunately do the opposite. They trade with money they can’t afford to lose, and a single bad stretch sets them back years.

Why “time in the market” wins for most people

The reason buy-and-hold tends to beat timing for the average person comes down to a few mechanical facts.

Markets grow over long periods

Despite every crash, recession, and panic, major stock indices have trended up over the decades, because companies as a whole earn more over time as productivity rises and economies expand.

If you’re invested for the long climb, you don’t have to be clever. You just have to be in it.

Compounding does the heavy lifting

Stay invested and your returns earn returns of their own.

Reinvested dividends buy more shares, which pay more dividends, which buy more shares. Contributions, plus returns, plus reinvestment, left alone for years, is a strong combination, and it only works if you stop interrupting it by jumping out and back in.

Staying put averages out the risk of bad timing

This circles back to the best-days problem.

Because nobody can reliably catch the handful of explosive days that drive most of the long-term return, the surest way to own them is to never leave. In general, market returns come in cycles and bursts that are unpredictable even to most professional investors.

A buy-and-hold investor catches every best day automatically, by doing nothing at all.

A timer has to earn each one, and the evidence says most don’t.

Dollar-cost averaging and the boring core

Dollar-cost averaging, or DCA, pairs naturally with the time-in-the-market approach, and it’s worth understanding even if you mostly trade.

The idea is simple. Instead of dropping a lump sum in all at once, you invest a fixed amount on a regular schedule, say every week or every month, no matter what the price is doing.

When prices are low, your fixed amount buys more shares. When prices are high, it buys fewer.

Over time, that naturally averages out your purchase price and takes the pressure off trying to nail a single perfect entry.

DCA’s real value is that it removes a decision you’re likely to get wrong and takes up time to try to get right. You aren’t staring at the screen trying to guess whether today is the day to buy.

You just buy, on schedule, and let consistency do the work.

It also keeps you from the worst behavioral mistake, which is freezing up and buying nothing when prices are falling, exactly when shares are cheapest.

Even active traders can run DCA on their long-term core while they trade the satellite.

Is short-term timing right for you?

This is a personal decision, and it shouldn’t be made on the basis of a few good weeks or a confident feeling. A few honest questions help.

How much risk can you actually stomach?

Not in theory, in practice.

Even a strong strategy loses, sometimes for long stretches, because of plain variance. If a string of losses would wreck your finances or your sleep, short-term timing is the wrong path.

There’s no shame in that. It’s just self-knowledge, and it’s cheaper than learning the same lesson with real money.

How much time and effort can you really give it?

Timing markets well is more or less a full-time job. It takes constant research, monitoring, and discipline.

And remember who you’re up against: people who do exactly that, all day, with better budgets, technology, information, and analysis than you have.

If you’ve got a day job and a life, you’re bringing a part-time effort to a full-time fight. For most people who don’t do markets for a living, that isn’t a winning setup, and being honest about it saves a lot of money and time.

Can you accept losing as part of the deal?

Losses are a reality for everyone. Timing can amplify them.

You have to be genuinely prepared, emotionally and financially, for the real chance that your approach won’t work, and to walk away or size down when it isn’t working rather than doubling down to get even.

Who actually makes money trading short term

It’s worth naming who the consistent short-term winners tend to be, because it clarifies what an edge really looks like.

The traders who reliably profit usually have a structural advantage that you probably don’t.

- Speed, in the case of high-frequency firms that act in microseconds.

- Information, in the case of desks with better data and research.

- Flow, in the case of market makers who get paid to provide liquidity and see order flow before the rest of us.

- Or a genuine, tested analytical edge that’s been proven across thousands of trades and/or many years, not a hot streak that hasn’t broken yet.

Most retail traders have none of these in a durable form. What they have is a brokerage app, a set of indicators everyone else also has, and the same news everyone else is reading.

That’s the consensus, and we’ve already covered what the price does with the consensus. It’s already in there.

This isn’t meant to crush anyone’s interest. Some people do develop real skill, and a small slice of active traders genuinely win over time.

But they’re rare, they usually hold an advantage most people lack, and they got there through a long, disciplined, often painful process.

If you want to be one of them, go in clear-eyed about the odds and the work, and size your bets so that finding out the answer doesn’t cost you.

Conclusion

The dream of beating the market by timing it is alluring, and it’s easy to see why.

The reality is that very few people do it consistently, and the deck is stacked against the ones who try.

Markets are very complex, the price already reflects what you know, alpha is zero-sum before costs and negative-sum after, and the competition includes players you can’t outgun on speed or information.

The data from Brazil, Taiwan, and the US all point the same way. Most people who time markets short-term lose, and they don’t get better with practice.

For the large majority of people, the higher-probability path is the boring one. Build a diversified core, stay invested through the ups and downs, let compounding work, and if you want to trade, do it with a small, survivable slice rather than the money your future depends on.

Time in the market has beaten timing the market for most people, across most periods, and the reasons it does are mechanical, not lucky.

Market timing isn’t worthless.

In specific situations, with real skill, real preparation, and money you can afford to lose, some traders find a degree of success with it.

I do it in some part as well, though within a structure.

But it’s far more of a trading concept than an investing one, and so much of the outcome depends on things outside your control. Know which game you’re playing.

Most people are better served, and a lot less stressed, by spending more time in the market and less time trying to outguess it.