Theta (Option Greek)

Theta, often referred to as time decay, is one of the most popular “Greeks” in options trading.

It measures the rate at which an option’s value decreases as time passes – assuming all other factors remain constant.

Understanding Theta is important for options traders, as it directly impacts the profit/loss of their positions.

Key Takeaways – Theta

- Theta accelerates as expiration nears, causing options to lose value faster.

- Plan exit strategies accordingly, especially in the final weeks before expiration.

- At-the-money options have the highest Theta, making them attractive for selling strategies but risky for buying.

- Higher implied volatility decreases Theta’s impact.

- Consider this when trading options during volatile market conditions.

The Basics of Theta

Definition

Theta represents the expected daily decrease in an option’s value due to the passage of time.

It’s typically expressed as a negative number, indicating the amount of value an option loses each day as it approaches expiration.

Calculation

Theta is calculated using complex mathematical models, such as the Black-Scholes model.

While the exact formula is beyond the scope of this overview, note that Theta is influenced by various factors, including the option’s strike price, time to expiration, and the underlying asset’s volatility.

Theta’s Impact on Option Types

Call Options

For call options, Theta works against the option buyer and in favor of the option seller.

As time passes, the probability of the underlying asset reaching the strike price decreases, causing the option’s value to decline.

Put Options

Similarly, put options also experience time decay.

The value of a put option decreases as time passes, benefiting the seller and working against the buyer.

Theta Decay (Theta Burn)

Theta decay, also known as theta burn, refers to the reduction in the value of an option as it approaches its expiration date, which reflects the erosion of the option’s time value.

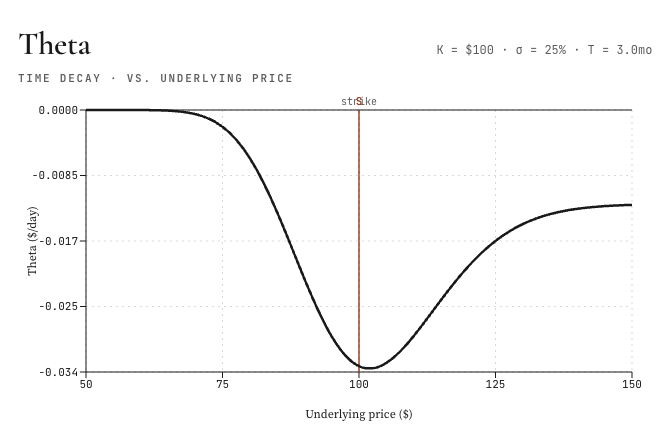

Theta vs. Underlying Price

This chart shows how theta changes as the underlying asset price moves relative to the option’s strike price.

The vertical red line shows the strike price at $100. The option has about 3 months to expiration, with 25% implied volatility.

The y-axis shows theta in dollars per day. This means how much option value is lost each day from time passing, assuming other factors stay constant.

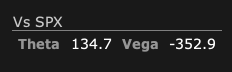

Theta/Vega Ratios

Brokers often also show theta and vega figures.

This shows the position’s Greeks versus SPX.

Theta 134.7 means the position is theoretically earning about $134.70 per day from time decay.

But this assumes price, volatility, and other inputs stay unchanged. Positive theta usually means the position benefits as options lose extrinsic value over time.

Vega -352.9 means the position loses about $352.90 for every 1 percentage point rise in implied volatility. It gains about that much if implied volatility falls.

So this position is short volatility and long time decay. It benefits from calm markets, falling implied vol, and time passing. But it can be hurt by volatility spikes, especially if SPX has sharp moves.

The theta/vega ratio shows how much daily time-decay income a position earns for each dollar of volatility risk. A higher ratio generally means you’re collecting more theta relative to your exposure to changes in implied volatility.

Most traders take a higher ratio as a positive, as it takes less of a change is implied vol to wipe out what theta pays.

Key Ideas

The key point: theta is most negative near the strike price. This happens because an at-the-money option has the most uncertainty and the most extrinsic value. Since extrinsic value is the part that decays with time, theta is largest there.

Far below the strike, around $50 to $70, theta is close to zero because the option is deeply out of the money and has little remaining time value.

Far above the strike, approximately $130 to $150, theta is also less negative because the option is deep in the money and more of its price is intrinsic value.

So the chart’s main message is: time decay hurts at-the-money options the most and affects deep in-the-money or deep out-of-the-money options less.

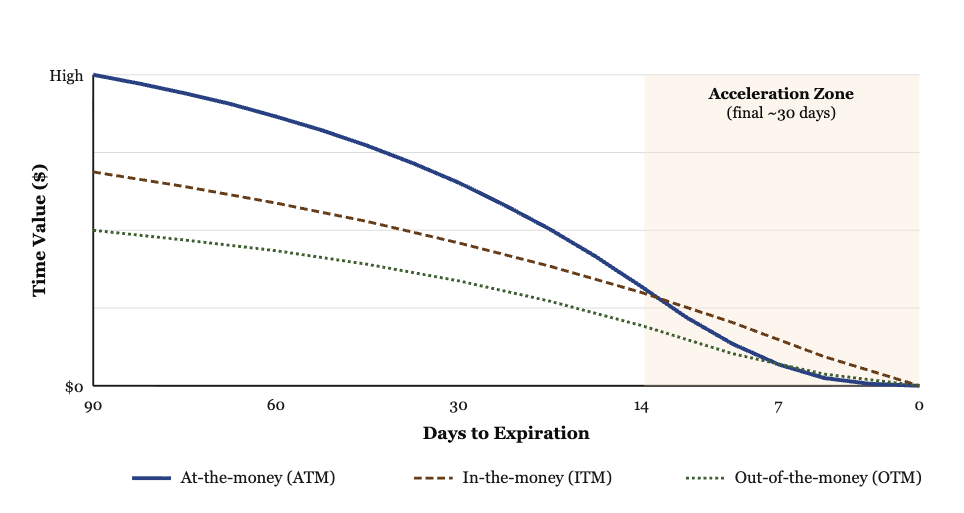

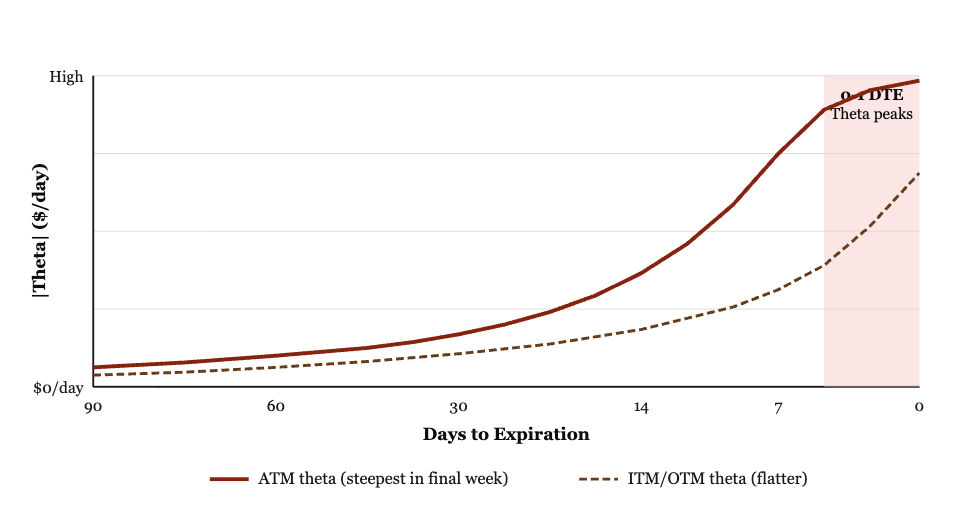

Theta’s Time Value

Let’s look at some other aspects of theta:

Time Value Over the Life of an Option

Time value bleeds out slowly at first, then collapses in the final weeks. The ATM curve loses value fastest in the home stretch because it has the most extrinsic value left to lose.

Theta Itself: The Daily Rate of Decay

Theta is the daily dollar amount the option loses to time.

It’s small far from expiration and explodes upward in the final days.

ATM options have the steepest theta because they hold the most extrinsic value.

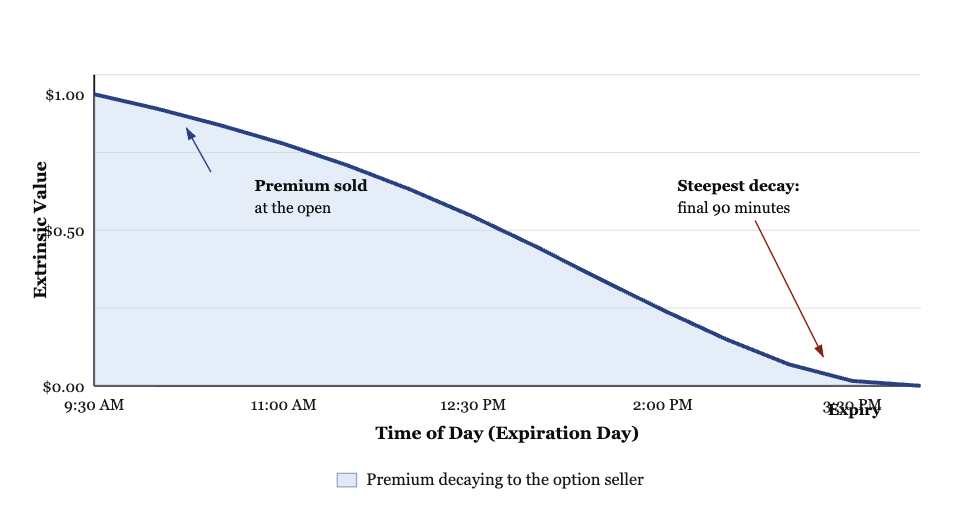

The Final Trading Session: Intraday Decay on Expiration Day

On expiration day, an ATM option’s extrinsic value collapses across a single trading session.

The seller harvests the entire shaded area, provided the underlying does not move enough to overwhelm the decay.

Theta Decay (“Theta Burn”)

For the day trader and the short-term trader, theta is a particularly important variable, as it’s highly relevant on their timeframes.

It’s a paycheck or a tax, depending on which side of the contract you’re sitting on. For every batch of time that goes by, extrinsic value bleeds out of the option.

Here is how the machine works. An option’s price is intrinsic value plus extrinsic value. Intrinsic is the “real” part, the amount the option is in the money. Extrinsic is the rest, the premium you pay for time and uncertainty.

Theta is the rate at which that extrinsic part rots away – i.e., through the effect of time. As expiration approaches, the rot accelerates. In the final session of a same-day expiration (0DTE) or weekly contract, what was a modest daily drip starts becoming a flood.

So who benefits? The seller. Always the seller, provided the underlying doesn’t move enough to overwhelm the decay.

This is the entire premise of theta-harvesting strategies. Sell the extrinsic value, let time do the work, buy it back cheaper or let it expire worthless.

As an options seller, you’re not betting on direction. You are betting that nothing big happens fast enough to matter. That’s a fundamentally different game from buying calls and hoping they rip.

Why day traders and short-term traders care

Day traders and swing traders operate on a time horizon where theta does most of its damage.

A 30-day option has gentle daily decay. A 3-day option is a melting ice cube.

Selling weekly or 0DTE options puts the trader on the harvesting side of the steepest part of the decay curve.

The catch: short-dated options also have the highest gamma. Gamma is the rate at which delta changes. High gamma means a small move in the underlying produces a big swing in the option’s value.

Put another way: when you sell short-dated options, you collect theta quickly but you also take on convex risk. One sharp move and the day’s theta is gone, plus more.

Therein lies the trade-off. A skilled short-term seller isn’t chasing premium for its own sake. They’re sizing the position so that the daily theta is meaningful, but the worst-case gamma move doesn’t blow a hole in their account.

The covered call and the core position

One of the most useful applications, especially for traders sitting on a long-term core position, is selling short-term out-of-the-money calls against it.

The idea is straightforward. You own the stock/index/commodity. You believe in it over months and years. In the meantime, you sell weekly calls struck above the current price.

What does this do? Three things.

- It pays you theta every day the stock does nothing or drifts up modestly.

- It lowers your effective cost basis.

- It only “hurts” you if the stock rips through the strike, in which case you’ve still made money on the underlying and kept the premium up to that strike.

- You’ve given up the tail. But you’ve been paid to do so.

Said differently: while the direction is still working in your favor, the clock is also working in your favor. You are getting paid twice for the same view.

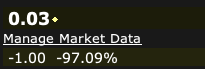

The attached option: a textbook theta burn

Now look at the option in the screenshot.

It’s currently priced at $0.03. It is down $1.00 on the session, a 97% loss. That tells you almost everything. This contract started the day with roughly $1.03 of value, almost all of it extrinsic. The underlying didn’t cooperate, time kept ticking, and the entire premium evaporated into 3 cents of lottery-ticket residual.

The buyer of that contract lost in a single session. The seller has harvested essentially the full premium. That’s theta burn in its purest form: the late-stage collapse of extrinsic value, compressed into one trading day.

Theta decay is why buying short-dated options for direction is one of the hardest ways to make money in the trading business, and why selling them, when done with disciplined sizing, can be valuable but also dangerous due to shorting convexity.

Factors Affecting Theta

Time to Expiration

Theta’s effect is most pronounced as an option approaches its expiration date.

The rate of time decay accelerates in the final weeks and days before expiration.

Those who want to minimize theta decay use longer-term options.

Moneyness

At-the-money options typically have the highest Theta values, while deep in-the-money and far out-of-the-money options have lower Theta values.

Volatility

Higher implied volatility generally results in lower Theta values, as increased volatility suggests a greater likelihood of price movement in the underlying asset.

Trading Strategies Involving Theta

Theta Decay Strategies

Experienced traders often employ strategies that take advantage of Theta decay.

These may include:

- Selling options (writing calls or puts)

- Credit spreads

- Iron condors and multi-leg options strategies

- Calendar spreads

Long-Term Options

Traders holding long-term options (LEAPs) may be less affected by Theta in the short term but should still consider its impact over the life of the option.

Managing Theta Risk

Rolling Positions

To reduce Theta risk, traders may choose to roll their positions forward.

They exchange near-term options for those with later expiration dates.

Adjusting Strike Prices

Traders can also manage Theta risk by adjusting strike prices, moving to options that are further in-the-money or out-of-the-money, depending on their strategy.

Theta and Other Greeks

Relationship with Delta

Theta and Delta are closely related.

As an option’s Delta increases (becomes more sensitive to price changes in the underlying asset), its Theta typically increases as well.

Interaction with Gamma

Gamma, which measures the rate of change in Delta, also influences Theta.

Higher Gamma values often correspond to higher Theta values, particularly for at-the-money options.

Secondary Greeks of Theta

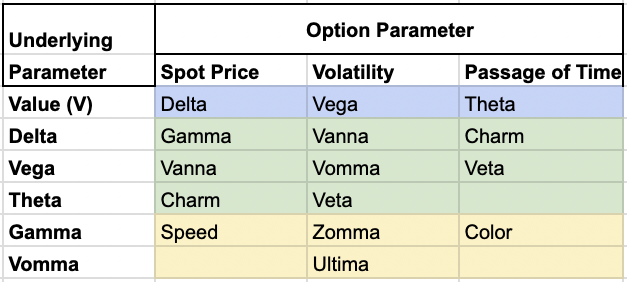

Secondary Greeks of Theta, such as Charm and Veta, provide deeper insights into how the passage of time impacts options pricing and help in managing the complexities of an options portfolio.

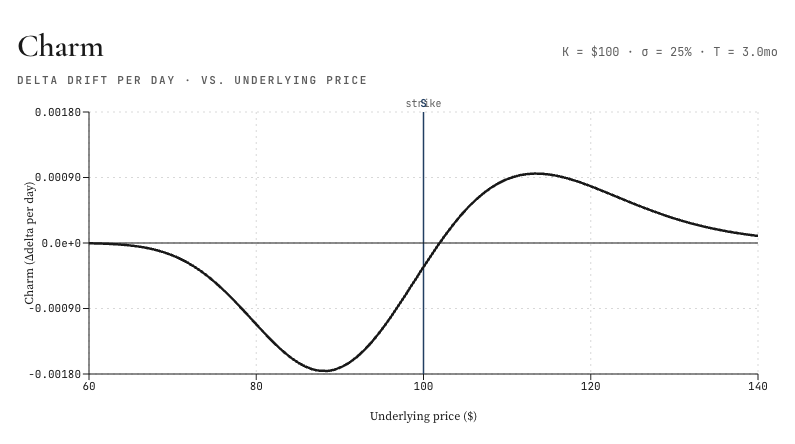

Charm

Charm measures the rate of change of Delta with respect to the passage of time.

It indicates how Delta will evolve as the option approaches expiration.

This Greek is important for traders managing the time decay of options, as it helps them anticipate changes in Delta, allowing for more precise hedging strategies.

For instance, an option with a high Charm value will see its Delta change significantly as time progresses (requiring frequent adjustments to maintain a neutral Delta position).

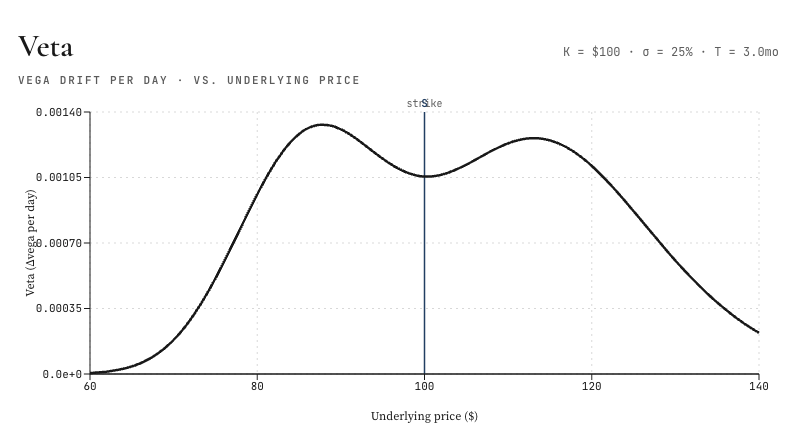

Veta

Veta measures the rate of change of Vega with respect to the passage of time, showing how the option’s sensitivity to volatility changes as expiration nears.

This is for volatility traders who need to understand how their Vega exposure will diminish as the option’s time to expiration decreases.

A high Veta value suggests that the option’s Vega will decay rapidly, impacting the effectiveness of volatility-based strategies.

Traders can use Veta to fine-tune their portfolios, so they’re not overly exposed to volatility risks that diminish as the option’s expiration date approaches.

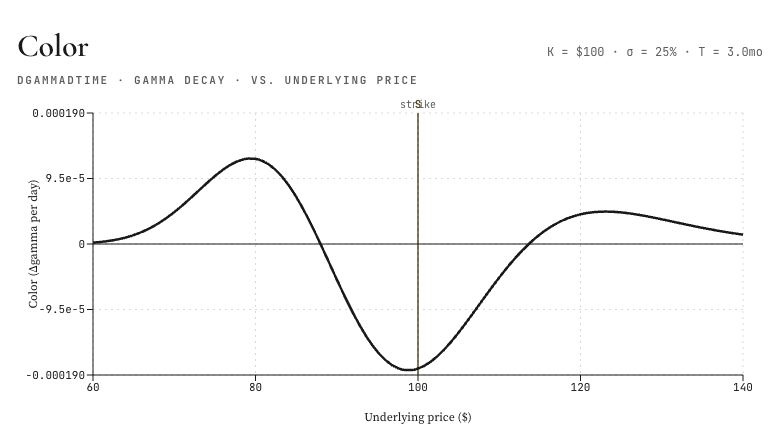

Color

Color, also known as Gamma decay, measures the rate of change of Gamma with respect to the passage of time.

Color helps traders understand how an option’s convexity will evolve as it approaches expiration.

This Greek helps traders understand the acceleration of Delta changes due to time decay, important for managing the risks associated with options nearing their expiration dates.

Overall

By incorporating Charm and Veta into their analysis, traders gain a more nuanced understanding of how time decay affects their positions beyond the primary Theta.

This allows for more sophisticated risk management and optimization of options strategies, especially in markets where time decay and volatility are important in options pricing.

Conclusion

Understanding Theta is important for options traders, as it directly impacts the profitability of their positions.

Consider Theta alongside other Greeks and market factors. They can help you make better decisions about entering, managing, and exiting their options trades.

While Theta generally works against option buyers and in favor of option sellers, its effects can be reduced or leveraged through various strategies and careful position management.