Social Media & Finfluencer Red Flags

Finfluencers can now be found on every major social media channel, making investing look easy, exciting, and profitable. But the reality is the opposite. We’ll explain how finfluencers work, the red flags to watch for, and the practical steps users can take when scrolling through social media. We also explain how regulators are tightening their noose on bad actors with examples of lawsuits.

Key Takeaways

- We’ve been tracking the finfluencer problem for some time now. We’ve done separate studies on viral TikToks, trading calls on X, and signals groups on Discord and Telegram.

- On TikTok, we’ve watched videos with combined views of 20.7M+, and graded 80% of videos C or below in 2026, while 60% got an F for risk disclosures (up from 30% in 2025).

- On X, we found 61% of viral trading ideas resulted in losses if followed, with many posts missing basic risk management suggestions or clear timeframes for users to follow.

- When we joined seven signal groups on Discord and Telegram, we documented an array of red flags, from 74% of signals having no stop losses to 54% of losing trades never being acknowledged.

- The pattern on social media is consistent: too much hype, too few risk warnings, and too many inexperienced traders being pushed into risky investments with limited context.

- Keep your wits about you on social media:

- Treat all content from finfluencers as marketing until proven otherwise.

- Always check whether the creator is being paid to promote a broker, prop firm, signals group, course, or something else.

- Do not treat lifestyle content, platform screenshots, or clips from demo accounts as evidence of genuine trading skills.

- Beware of finfluencers who convey a sense of urgency: “act now”, “only a few spots left”, “next trade dropping soon”, and “exclusive group”, these are normally sales tactics

- Verify any brokerage, platform, or investment opportunity on the databases of relevant financial regulators, and don’t trust referral links or social media bios.

- Keep screenshots, chat logs, and payment information so if something looks suspicious, you can report it to the social platform, regulator or police where appropriate.

What Is A Finfluencer?

A finfluencer (short for financial influencer) is a person who shares financial advice, money tips, or investment ideas on social media platforms like TikTok, Instagram, YouTube, or X.

Finfluencers often post content about things like:

- Budgeting and saving money

- Stock market investing, forex trading, or cryptocurrency

- Side hustles and making extra income

- Personal finance strategies

Some finfluencers are trained professionals (like financial advisors or analysts), but many are not formally qualified and instead share opinions or personal experiences. We know this because our team have spent more than 100 hours watching finfluencers on various channels, including TikTok, X (formerly Twitter), and YouTube. We’ve seen some very worrying things, from wild stock picks to a complete lack of risk disclosures.

In many countries, financial regulators have warned consumers that some finfluencer content may be misleading or not properly disclosed as a financial promotion.

Finfluencers are often sponsored in ways that are either clearly disclosed (open) or hidden or unclear (secret or disguised). When sponsorships and paid marketing are unclear, viewers might think they are seeing independent advice or are hearing about true experiences, when they are actually subjected to financially incentivized content.

Finfluencer Risks

The finfluencer industry did not appear out of nowhere. It grew out of a simple gap in the market. Many consumers wanted fast, informal, and easy-to-access and digest guidance served up through social media, while financial authorities and conventional consumer watchdogs and advisors were reluctant to step into this niche and fully embrace social media channels.

It is also worth remembering that conventional players, including brokers, tend to be more heavily scrutinized, and more likely to be penalized if they do not stay within the applicable frameworks for risk disclosures, suitability constraints, risk warnings, and compliance reviews.

Social media personalities stepped into that gap, and with that, some of them started behaving like unofficial distribution agents for high-risk products rather than objective teachers.

There are many finfluencers who should be seen as outright vendors, and the products they are hawking to everyone, including inexperienced traders, are often high-risk, and in some cases even fraudulent.We’ve seen a lot of finfluencers who are more about displaying a desirable lifestyle than actually explaining how a trading or investment path works. This is how consumers get steered toward highly speculative products, offshore platforms in lax jurisdictions, prop firm challenges with horrible terms and conditions, low-quality copy trading, paid signal groups, and so on.

The result is often a sales layer with the reach of a marketer and the accountability of a disappearing Telegram admin.

How To Spot Common Warning Signals

Let’s look at a few examples of common warning signals that you should not ignore:

Lifestyle Over Substance

Does this finfluencer actually give truthful and useful advice and information, or are you just mesmerized by the lifestyle they portray?

A lot of finfluencer content relies on the old formula of letting status symbols do the talking. Luxury cars, business or 1st class flying, private jets, fancy hotel suites, watches and jewelry, and even stacks of cash, are mingled with screenshots of improbable PnLs. The idea is to promote a certain lifestyle and let it be “proof” of how successful the financial products are.

None of this proves fraud by itself. It does, however, tell you what the sales argument is. The offer is not “here is a repeatable process with independently verifiable risk-adjusted returns”. The offer is “look at the life this can buy”. Regulators have been warning for years that investment fraud often starts by appealing to greed and aspiration rather than evidence and a deeper understanding of markets.

This matters because lifestyle marketing is known to change how risk is interpreted. An inexperienced trader stops asking whether the strategy is credible and starts asking how quickly the strategy can deliver a visible upgrade in lifestyle. That is when sensible questions disappear:

- What is the drawdown?

- What is the sample size?

- Where is the independently verified record?

- What product is actually being traded?

- Which regulated entity is involved?

Those questions do not create dopamine on TikTok, so they usually get crowded out by images of sports cars and orange shopping bags.

It is important to remember that different lifestyles appeal to different people, and finfluencers are very much aware of this. It might be easy for you to laugh at the over-the-top 22-year-old guy who makes trading videos from a rented Lamborghini. But what about the account where a seemingly down-to-earth mother in her 30s is showing how trading from home has given her the opportunity to be more present around her children and move them into a charming cottage in the countryside?

With the latter, pushing for whatever financial product she is being paid to hawk will take the backseat to images of homegrown heirloom tomatoes and reels of adorable toddlers playing with chickens in the backyard, but that does not make the underlying mechanics of her getting paid to promote certain products any less real.

Likewise, it is important to remember that many finfluencers are not actually living the life they portray online. Some of them are really making a lot of money, but it is from the paid promotions, not from actual trading. There are also many who simply put on a show for the audience, showcasing a lifestyle that is very far from their own.

This is not unique to finfluencers, and the market segment for “rent-a-lifestyle” products that can be displayed online is larger than we want to believe. One well-known example is FD Photo Studio in Los Angeles, which offers a full set designed to look like the inside of a luxury private jet. The setup includes aeroplane seats, windows with “sky” lighting, and realistic cabin details. Controlled lighting helps make the photos especially appealing. Instead of forking out on actual plane tickets, influencers can rent the space, with prices starting at $35–$55/hr off-peak.

Urgency Dressed As Exclusivity

The second behavioral red flag is urgency dressed as exclusivity. Social media funnels for trading scams and aggressive affiliate promotions often rely on countdowns, closing doors, time-limited VIP access, disappearing offers, and “today only” scripts.

The UK FCA’s protect yourself from scams page says pressure to act quickly and claims that an opportunity is available only for a short time are classic warning signs. When a finfluencer says, “only five places left in the VIP Telegram,” the correct reaction is not excitement. It is to ask why a genuinely profitable market method needs a nightclub rope outside it. Scarcity in these cases usually attaches to the funnel, not to the edge.

Exclusivity also creates a useful psychological trap for the promoter. Once the follower feels admitted into something private, criticism becomes harder. Losses are reinterpreted as a test of discipline. Failed trades become proof that the student “didn’t follow the rules”. Account blowups become evidence that the trader lacked the right mindset, not that the system was poor. The guru keeps status. The follower feels the blame.

Pushing Prop Firms Without Showing The Full Picture

A third red flag is the way some influencers push low-tier prop firms. We’ve watched prop trading firms pop up in troves in recent years. Now, not every prop firm promotion is dishonest, and some firms are legitimate businesses with clear evaluation rules.

The problem is that the economics of affiliate promotion can distort what is being recommended. If a finfluencer is paid when followers buy challenge accounts, then follower failure is not necessarily bad for the promoter. The promoter is being paid when you sign up and deposit, and has no incentive to care if you become profitable or not. This would not be as sinister if the finfluencer clearly disclosed that you are seeing a paid promotion. But many finfluencers talk like mentors and educators, while serving as a for-profit customer acquisition channel.

When finfluencers are being paid to push a particular prop firm, they are also more likely to avoid bringing attention to the downsides of prop trading, the widespread issues that exist within the prop firms industry, and how many scammers simply use the prop firm promise as a lure for short-term fraud.

A prop firm (proprietary trading firm) is a company that trades financial markets using its own money and give traders access to a part of that capital under certain rules. The typical path looks like this:

- You apply to the prop firm. Sometimes, there is an application fee.

- You must pass a challenge or evaluation, e.g. hit a profit target over a predefined timeline while avoiding big losses (strict drawdown limits). You might be required to make a deposit to be allowed to participate in the challenge/evaluation and prove yourself.

- If you pass, you get a funded account and start trading using company money. The appeal is that you get to keep a share of the profits.

Prop firm promotions are especially appealing to prospective traders who do not have enough money to fund their own account, or traders who want to “level up” quickly rather than gradually build their bankroll over time. These traders tend to be fairly easy prey for prop firms, where the business model is actually to extract application fees and deposits from individuals eager to prove themselves.

There are also prop firms where you do get access to company money for trading, but the terms and conditions are horrible for the trader, who rarely gets to see any share of the profits.

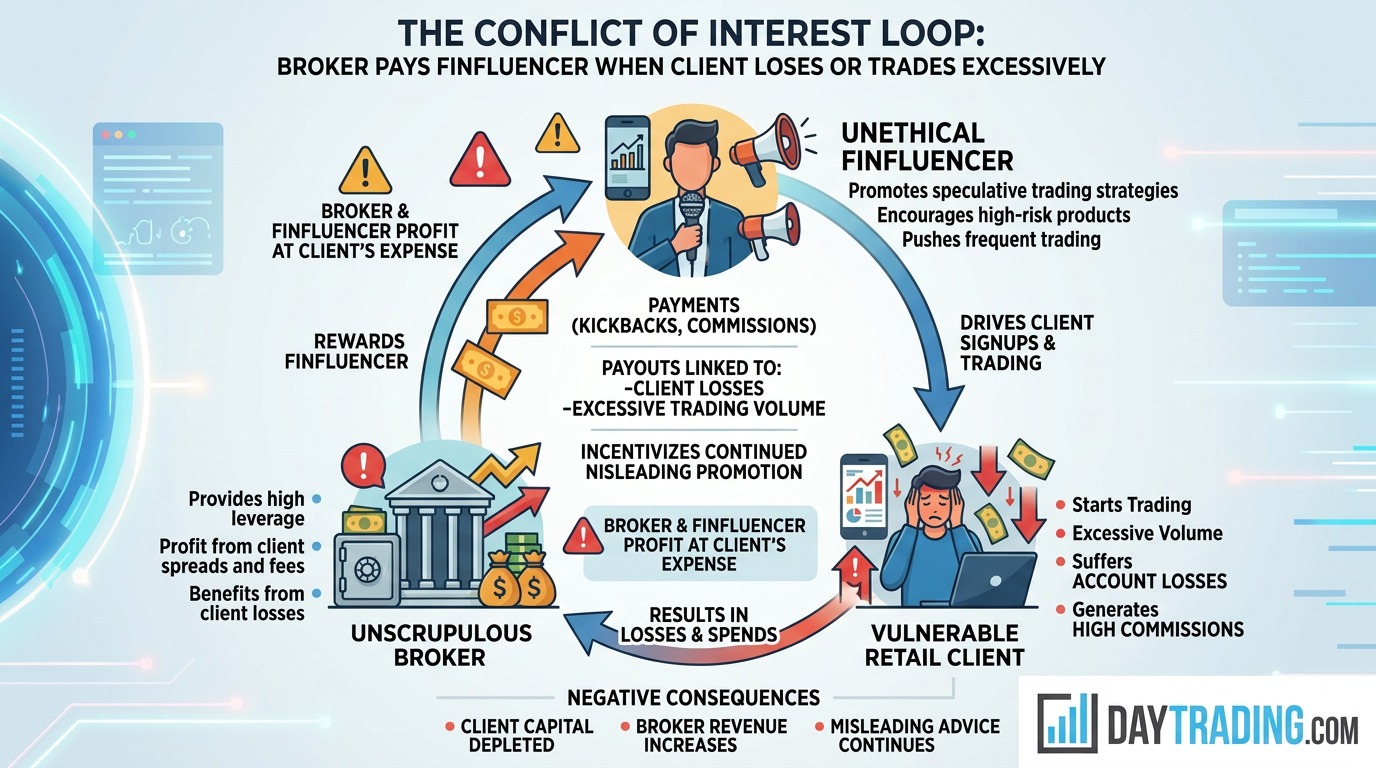

Secretly Paid-For Brokerage Referrals

Just like finfluencers can get paid to promote prop firms, they can get paid to promote standard retail brokers. And just as with prop firms, this is typically legal as long as paid promotions are disclosed correctly, and the finfluencer also adheres to other applicable rules that apply to the retail financial advice sector.

Many finfluencers have zero incentive to actually help make you a long-term profitable trader, since the payment model (the kickbacks they get from the broker) is designed differently. The CFTC’s advisory on what customers should know before trading forex explains how the broker can make money when the customer trades more often, loses money, or pays fees, spreads, or commissions.

That point is critical because it maps neatly onto many finfluencer arrangements, and it is not unique to forex. If the promoter is paid by an introducing broker or affiliate structure linked to client turnover, then follower activity matters more than follower profitability. The faster the audience trades, the better the kickbacks, since they are generating more profit for the broker.

An educator wants the follower to actually learn and become a long-term profitable trader or investor. An affiliate finfluencer account tied to turnover wants the follower to deposit quickly and engage in very frequent trading.

If a finfluencer insists that followers use one exact broker, one exact prop firm, or one exact challenge provider, the natural question is not whether the choice is “good”. The first question is whether the promoter is being paid to send flow there.

Paid promotions and conflicts of interest should be disclosed clearly. In social media trading culture, disclosure is often buried, absent, or disguised as a casual “partner link”. That is not a trivial omission, since it changes the meaning of the recommendation.

The problem gets worse when the promoted entity is located in a foreign country with lax trader protection. The FCA’s Warning List exists precisely because unauthorized firms and individuals keep trying to target users in countries where they can not legally operate. When a finfluencer pushes an obscure platform with an affiliate link and no real explanation of authorization, compensation, custody, or complaint rights, the user is not receiving fair guidance.

In really severe cases, finfluencers have even been paid to post links to clones of a real firm. Clone sites are created by fraudsters who simply copy the entire website of a well-known, reputable and licensed firm, and bring in traders who think they are dealing with the real thing. The website content is placed on a correct-sounding domain (e.g. ABCD-Trading.com or ABCDGlobalTrading.com instead of ABCDtrading.com) and minute changes are made to ensure the trader will deposit their money into an account controlled by the fraudster instead of opening an account with the true firm. When inexperienced traders trust a finfluencer and click referral links without double-checking them, it spells disaster.

One reason this type of marketing works so well online is that social platforms compress judgment into very short windows. A trader looking for quick dopamine by scrolling through reels is probably not super interested in running deep due diligence on a suggested broker. The person is reacting to pace, confidence, symbols of wealth, and the illusion that you are losing money by not getting into the room right now.

That is why the behavioral patterns matter when we evaluate finfluencers who are handing out “advice”. These patterns are not random branding choices; they are recurring mechanisms for suppressing normal skepticism. Once you see that, the whole performance starts to look less like mentoring and more like funneling. The deeper issue is that all of this fits a broader pattern already visible in trading marketing as a whole.

Our article on marketing versus statistical reality makes the central point well: marketing is built around emotion, while actual financial trading is built around probabilities and risk management. That mismatch is exactly what finfluencers exploit.

How Successful Trading Can Be Faked

The technical side of deception is where many otherwise critical followers get deceived. They understand that marketing can exaggerate, and they don’t really care much for the Lfambo pics, but they still assume the screenshots and trading platform clips are true. And often, these clips are anchored to something real, but not in the way the viewer assumes.

This is where independent sense checks can be helpful. Social media stories are almost always smoother than actual PnL curves.

Demo Accounts

The demo account illusion is the classic example. A social media clip shows one of the trading platforms MT4 or MT5, a sequence of winning trades, a growing balance, and a confident voice over. The viewer assumes this is live trading because the speaker is acting as if real money is on the line. That deceitful acting is exactly the problem.

Demo environments can (and should) look very similar to live accounts, especially in short video clips where account type, server name, and terminal details are cropped, blurred, or covered. Some promoters simply hide the “demo” label. Others use white-label servers or account names that look official enough to casual viewers. The point is not that every profitable-looking clip is fake. The point is that the platform view, by itself, proves very little.

That is why independently verified records matter so much more than native screenshots. If somebody claims serious, repeatable returns, the natural response is to ask for a verified third-party track record or at least consistent broker statements that can be reviewed over a meaningful period. The due diligence standard should be much closer to “show the audited trail” than “post another screenshot”.

Cherry Picking

Cherry picking is another common trick. A promoter posts one week of perfect results, one dramatic runner, or a streak of winning challenge accounts, while the losing periods vanish into silence. Instead of outright faking results, they are merely selective about what they publish. They are technically not lying about results, but they are not showing you the full picture either.

While this distinction might matter morally and in some cases legally, it does not benefit the follower financially. As a viewer, you are still being shown a distorted sample, even though it is not demo trading or Photoshop results.

A strategy with a 100 percent hit rate over five trades means almost nothing without context:

- What happened over six months?

- How many accounts were reset?

- How large were the losses?

- How much of the result came from abnormal size?

Without answers to important questions, the published record is really just advertising.

Selective publication misstates returns and survivorship. The finfluencer who posts a winning funded account today may have blown several smaller accounts before that. The channel that shows only one profitable week may have deleted months of poor calls.

The polished reel gives the impression of consistency when the underlying process may be volatile and with huge drawdowns. That matters because retail traders believe this cherry-picked picture of what normal looks like and then get checked when their reality does not match the fantasy.

Deleted Social Media Content

Social media accounts can purge old posts, hide videos that aged badly, make discreet edits, and generally curate their content to match the current narrative. That angry post published in haste that showed a not-so-rosy side of trading will be gone in 24 hours, as if it never existed.

This is where tools such as SocialBlade or cached page histories can sometimes (but not always) help as a rough sense check, because they can reveal sudden content deletions and reputation management patterns. SocialBlade is not a regulator and should not be treated as hard proof of wrongdoing, but it can still show how an account is curating its image over time.

Comment Moderation

Comment moderation is a necessary job for most social media accounts because, without it, comment sections easily turn into cesspits and may also violate the rules of the platform. With that said, some finfluencers also take the opportunity to make sure that critical voices do not show up in the comment section, or that certain topics are off limits.

A channel having thousands of positive comments does not mean much if critical responses are suppressed. For some accounts, a social media manager will read all comments before they are approved and become visible. On other accounts, critical comments will show up immediately, but then be removed again quickly, especially if they garner responses from other followers.

There are also accounts that will purchase positive comments, sometimes in an effort to boost general engagement for a budding account, and sometimes to drown out the critical comments posted by actual netizens.

The Trading Group Funnel

The trading group funnel has become such a common sight among questionable finfluencers that we decided to give it its very own section in this article. On the surface, the model is simple. A trader is convinced to join a Telegram, Discord, WhatsApp, or private app channel. Once inside, they receive trade ideas, account screenshots, broker links, and motivational material. In practice, the group is usually the middle of a funnel, not the end of it.

While this type of group can be benign, the field is overcrowded with signal groups that pretend to be helpful and objective while actually existing for different reasons, e.g. to facilitate market manipulation (pump-and-dump schemes) or to funnel traders to certain brokers or signal service subscriptions that gives the group owner a kickback.

From a legal perspective, the devil is in the details, and whether a particular group crosses from education into regulated promotion or advice will depend on the jurisdiction, what is being said, how specific it is, whether products or firms are being promoted, if the communicator is authorized or approved, how promotions are disclosed, and so on. The point for the reader is not to become a lawyer. It is to notice how “this is just education” or “this is just traders exchanging ideas” is often used as a blanket excuse for something very different.

The commercial conflict is usually easier to spot than the legal one. Free groups commonly make money through broker links, affiliate commissions, revenue share on client turnover, signal service subscriptions, or paid upgrades to VIP rooms. If the group provider is tied to some type of affiliate arrangement, they may be rewarded for trade frequency rather than trade quality.

That is a classic churning incentive. It does not matter that the group is called “free”. You, the member, are actually the product that is being sold, and that is the proper way to view the group funnel. The free education is the lead magnet. The urgency is the conversion tactic. The signup link or the VIP up-sell is the revenue engine. These groups often look informal and grassroots because informality reduces skepticism.

It is also worth noting that once traders are burned by one social media scheme, such as a group funnel scam, they often become targets for fake recovery agents, bogus investigators, or “fund retrieval” operators using legal-sounding language. A recent DayTrading.com article on recovery scams is shedding light on this nasty second layer and explains how traders can protect themselves.

It is important for traders to understand that the social media scam cycle often does not end with the first loss. Bad actors know that a defrauded trader is emotionally vulnerable and may respond well to follow-up attempts focused on money recovery. A person who trusted one fake mentor can be sold a fake recovery service next. Different costume, same bottom line.

Reporting Questionable Finfluencers

If a finfluencer appears to be running an investment scam, pushing unlawful promotions, impersonating a regulated firm, or channeling users into suspect platforms, you can report it to the platform, to the applicable financial authority, and to the police (if the case involves a crime, e.g. fraud).

Typically, only reporting the finfluencer to the platform will not make much of a difference, because even if the platform decides to take action and close the account, the finfluencer will just pop up again somewhere else.

How To Report On Major Social Media Platforms

Below, we will look at accounts, posts, and videos/reels, but you can also report other things, such as DMs, ads, comments, and groups.

TikTok

Report an account:

- Go to profile → tap ⋯ or Share arrow → Report

- Choose: Fraud or scam

Report a video:

- Open video → Share → Report

- Select Scam / misleading content

Report an account:

- Profile → ⋯ → Report

- Choose: Scam or fraud

Report posts/reels:

- Tap ⋯ → Report → Scam or fraud

Report a profile/page:

- Go to page → ⋯ → Find support or report

- Choose: Scam, fraud, or fake investment

Report posts:

- Tap ⋯ → Report post → Scam

X

Report an account:

- Profile → ⋯ → Report

- Choose: It’s suspicious or spam → Scam

Report a post:

- Tap ⋯ on tweet → Report post

YouTube

Report a video:

- Under video → … → Report

- Choose:

- Scams or fraud

- Misleading content

Report a channel:

- Channel page → Report user

Report a profile:

- Profile → More → Report/Block

- Choose Scam or fraud

Report messages:

- Open chat → Report

Extras:

- Especially important for job/investment hybrid scams

Snapchat

Report an account:

- Profile → ⋯ → Report

- Select Scam

Report a snap/story:

- Press and hold → Report

How To Make Your Report Stronger

- Save screenshots (promises, balances, testimonials)

- Keep chat logs, when applicable (especially payment instructions)

- Note payment methods (crypto wallets, PayPal, etc.)

- Capture external links (Telegram, WhatsApp, websites)

The Response From Regulators

Regulators are no longer treating this field as harmless hype, and many have stepped up to enforce consumer protection and market integrity in various ways. A notable example is the UK’s FCA. The authority’s finalised guidance on financial promotions on social media clearly states how financial promotions on social media must be fair, clear and not misleading, and that firms working with affiliates such as finfluencers should take proactive responsibility for how those promotions are communicated.

- In October 2024, the FCA said 20 finfluencers were being interviewed under caution, and 38 alerts had been issued against social media accounts that may have contained unlawful promotions.

- In June 2025, the authority led an international crackdown on unlawful finfluencers.

- In February 2026, the FCA announced that influencers had been fined for unauthorized financial promotions.

The FCA’s social media guidance clearly states that financial promotions rules are technology-neutral and apply across social media. A person cannot escape the regime simply by posting on Instagram rather than in a brochure.

The UK’s FCA is not an isolated example, as financial authorities and wider legal systems are currently stepping up in many different parts of the world. We are also seeing a strong trend where regulators from different jurisdictions are increasingly coordinating cross-border crackdowns on finfluencers.

Across countries, enforcement against rule-breaking finfluencers tends to fall into three main categories:

- Undisclosed paid promotions. Regulators are going after finfluencers for violating disclosure rules when they promote securities and other financial products without letting the followers know it is a paid promotion.

- Unlicensed financial advice. In many jurisdictions, financial advisors must be properly licensed.

- Market manipulation and fraud. Financial regulators are working together with the wider justice system to prosecute finfluencers who engage in pump-and-dump schemes and other forms of market manipulation and fraud. These cases have a tendency to become especially serious and the accused are risking hefty prison sentences if convicted.

₹546 Crore (65+ Million USD) Seized In India

In India, the Securities and Exchange Board of India (SEBI) ordered the seizure of ₹546 crore from a finfluencer-linked operation in December 2025. Back then, the Indian rupee was trading roughly around ₹82–₹84 per US dollar, so the amount equaled circa 65.8 million USD. The high-profile crackdown targeted networks associated with well-known Indian influencers such as Ravindra Bharti and educators such as Baijnath Yadav.

The network was active on a variety of Telegram and YouTube channels, and what particularly caught the attention of the SEBI was how those pulling the strings would benefit financially from stock price movements generated by stock picking advice distributed within the network. SEBI has become known for its capacity to issue interim (temporary) orders quickly, including immediate trading bans and the instant freezing of accounts associated with someone being investigated. This reduces the ability of suspected rule-breakers to continue activity during the investigation and move money to safe havens.

SEBI has clearly moved away from the stage where a regulator just issues warnings and has moved into an era where they are carrying out large-scale asset seizures, imposing market bans, and working to hold finfluencers legally accountable for unlawful actions. This signals a shift where rule-breaking finfluencers active on the Indian market are no longer seen as just a problem for individual consumers, but as potential systemic risks to market integrity.

The SEC Does Not Shy Away From Going After Well-Heeled U.S. Celebrities

Another example of a regulator that does not fear taking on even the most high-profile cases is the U.S. Securities and Exchange Commission (SEC).

In 2022, reality TV-star Kim Kardashian was fined $1.26 million by the SEC for promoting cryptocurrency token EthereumMax (EMAX) without disclosing she was paid $250,000. The following year, former professional basketball player Paul Pierce was fined over $1.4 million for similar undisclosed crypto promotion.

SEC And DOJ Push For Prison Sentences In Alleged Pump-And-Dump Scheme

In 2022, eight individuals, of whom several were finfluencers on Twitter/Discord, were accused of running pump-and-dump schemes. Working together, the SEC and the U.S. Department of Justice pushed a case that resulted in not only fines but also civil charges and criminal prosecution. At the time of writing, the case is still ongoing.

The eight individuals allegedly promoted stocks to followers and earned money from pump-and-dump schemes. According to the authorities, they generated over 100 million USD in illicit gains from this type of market manipulation and fraud. The DOJ charged them with securities fraud conspiracy and wire fraud, crimes which carry potential prison sentences. Several defendants have pleaded guilty or entered plea negotiations, but others have contested the charges, and the case has not yet been wrapped up.

ASIC Initiates Civil Proceedings Against Australian Finfluencer ASX Wolf

The case of Tyson Scholz, widely known online as the finfluencer ASX Wolf, is one of the most prominent examples of regulatory action against a finfluencer in Australia. Scholz built a large following on Instagram by sharing stock market content, trading strategies, and promoting access to paid groups where followers could receive investment tips. Among other things, he ran the private Discord group “Black Wolf Pit”.

In December 2021, the Australian Securities and Investments Commission (ASIC) initiated civil proceedings, alleging that he was operating a financial services business without holding the required license (AFSL) under Australian law. See Section 911A of the Corporations Act 2001 (Cth). It is important to note that this was civil regulatory action, not criminal.

In December 2022, the Federal Court found that his activities constituted unlicensed financial advice, rejecting the argument that his content was merely educational. The court found that Scholz had been providing financial product advice (stock tips) and running a systematic profit-making business, which amounted to a breach of s911A since he did this without the required license.

The court subsequently imposed a permanent injunction in 2023, effectively banning Scholz from operating any financial services business. The court warned that breaching this order could lead to imprisonment.

Scholz was ordered to pay 456,296.64 AUD in ASIC legal costs. This was not a fine, but a court-ordered cost recovery.

After failing to pay substantial legal costs, Scholz was declared bankrupt in February 2024.