Recovery Scams

This guide explains how recovery scams target online traders who have already been defrauded. We unpack how these schemes work, the key warning signs to watch out for, and explain how scammers often use a victim’s personal data, pose as a fake authority, and lean on technical jargon to make their lies seem credible.

We also emphasise that the safest response is to:

- Avoid unsolicited offers to recover funds.

- Protect your personal identity and accounts.

- Only use official channels to report fraud.

How To Spot Them And Protect Your Funds

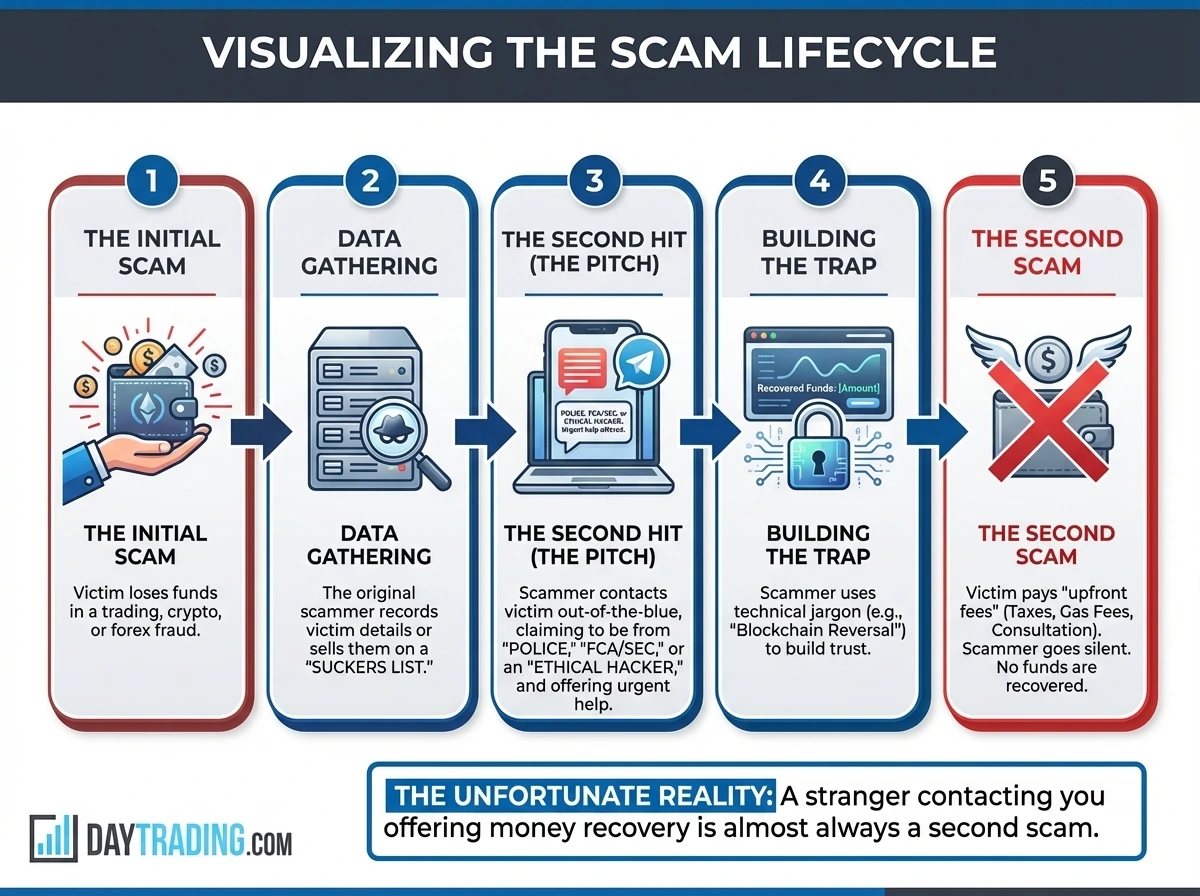

Losing money to a trading or investment scam is bad enough. What catches many people off guard is what comes next. After the first fraud, a second pitch often arrives fast, when the victim is still reeling from the first blow. Someone confidently claims they can trace the funds, reverse the blockchain, pressure the exchange, or use legal contacts to get everything back. They might even be able to make sure the scammers get punished. That second pitch might feel reassuring, but it is just the next fraud.

For years, regulators and consumer advocates around the world have warned about so-called recovery scams, where fraudsters target victims who have already lost money in a scam, and promise to solve the problem. This happens after many different types of scams, and trading and investment scams are no exception.

Recovery scammers have many different pitches in their toolbox, but most of them boil down to the same concept. First, they convince the victim that it is possible for them to get their lost money back, if they just cooperate. Then, they start asking the victim for money under various justifications. Of course, no money is ever recovered. The victim is just bled for more and more, until the jig is up and the fraudster goes silent. The SEC’s investor alert on asset recovery companies, the FCA’s warning on recovery room scams, and the CFTC’s advisory on recovery frauds all describe the same pattern.

Regrettably, recovery scams have become increasingly advanced and convincing, and AI-powered deepfakes are taking it another step further. Many scammers are also well versed in the language of compliance, on-chain tracing, exchange operations, legal process, etc. They use terms and explain processes that sound real, because they know how the real thing works.

Exchanges do respond to valid law enforcement requests. Banks and payment processors can sometimes reverse or recall transfers. Police do investigate fraud and sometimes manage to seize assets when they bust fraud rings. What is fake is the stranger in your inbox, who is just a simple scammer and not connected to any of the real things.

The second hit works so well because it arrives when the victim is still trying to make sense of the first loss. In market terms, this is forced trading after a large drawdown. Judgment is impaired. The victim is angry, embarrassed, maybe in financial stress, maybe even sleep deprived, and looking for a fast path back to flat.

Recovery scammers know what they are doing because they know that the victim has been scammed, and they exploit it. Recovery scams work because they sell hope. For victims of trading fraud, the safest rule is still the simplest one: unsolicited recovery offers are almost always a second scam. The real path is slower, less dramatic and (regrettably) often futile. Contact the bank. File the report. Notify the exchange. Preserve records. Use official channels. Ignore anyone who asks for upfront money to “release” funds that are supposedly already waiting.

Suckers Lists

So, how can the recovery scammers know that you have recently been scammed? Because they are the original scammers, or working with them. Or, they have bought your name and information from a detailed “suckers list”, which includes information about the scam, when it happened, how much you lost, and so on. Suckers lists are also known as lead lists or target lists.

Being on one of these lists will not only increase the risk of a recovery scam, but also of any type of scam. Scammers know that the people on the list have been scammed in the past. If the list is detailed enough (modern suckers lists are often a bundle of detailed case files rather than a simple list of names and contact info), the scammer will know what type of scam you fell for, what type of trading you are interested in, and so on.

Yes, some of the victims on a suckers list are now more difficult to scam than the average person, since they have learned from the past. But suckers lists would not exist if that were the norm. The sad truth is that whatever vulnerability that was exploited by the first fraudster will probably still be there. Also, recovery scammers are banking on how you might not be an easy victim for a classic trading scam anymore, but very much primed for a sophisticated recovery scam, hitting your from another angle.

Fraud investigators and consumer agencies have repeatedly warned that scam victims are ending up on these lists and being contacted for more scam attempts. Whether the list comes from the original scam, a data broker, a fake support channel, or social media scraping, the effect is the same. The person who already sent funds or shared sensitive data with a scammer is now marked as more likely to respond again.

Fraudsters do not throw away data. Once you engage with a scam, your contact information may be circulated, resold, or reused as part of a fresh targeting cycle. If you fall for both scam #1 and a recovery scam, you become an even warmer lead. That helps explain why many victims of recovery scams see a surge in phishing emails, fraudulent text messages, fake compliance calls, and supposed legal follow-ups. The post-recovery scam approach may come from someone claiming to represent a “police anti-fraud unit”, “financial authority recovery desk”, “VISA chargeback team”, or “crypto exchange fraud verification department”. The branding can shift, but the aim stays the same.

Scammers Responding To Posts About Being Scammed

Sometimes, the info that leads a recovery scam operation to you doesn’t come from the previous scammer. Public posts saying “I got scammed by broker X” often attract replies from supposed recovery experts within hours. The same is true if you share your experience in a trader chat group or similar. The approach is not random; it is targeted prospecting aimed at recent victims.

Public posts about being scammed often attract immediate replies from strangers offering help. Those replies are not acts of charity. They are prospecting. Once your number, email, Telegram handle, or account name has been linked to a prior fraud, you should assume it may circulate again, and contact attempts should be treated with great suspicion.

Search Results Can Be Part Of The Scam

Another problem is search engine poisoning. Fraudsters build pages targeting searches such as “[Broker Name] review,” “[Broker Name] scam,” or “how to recover money from forex scam.” The aim is simple: catch victims who are already looking for help and collect the next round of data through contact forms, WhatsApp conversations, or similar. A polished website that ranks well in Google is not proof of legitimacy.

In this niche, it can just mean the scammer understands basic SEO or paid someone who does. If you entered details into a “contact us” form on an unverified site after the first scam, assume that information is in the hands of recovery scammers.

The safest route is still the dull one: use official reporting portals, verified regulator sites, and known institutional contact pages. It might not feel as satisfying as finding a specialist with a dramatic homepage and a promise to act within the hour, but it is the safer move.

How Recovery Scams Work

1. Fake Identity

Recovery scams usually start with a mask. The person might for instance pose as a lawyer, a cyber investigator, a blockchain analyst, an exchange insider, a compliance consultant, a tracing expert, or an ethical hacker.

The U.S. Securities and Exchange Commission (SEC) has published public alerts about asset recovery scams and warnings regarding entities that are using recovery-themed names and false claims about being registered, licensed, or based in the United States. The UK FCA has also warned consumers about recovery room scams and unauthorized firms presenting themselves as recovery operations.

The label changes, the playbook does not. Recovery scammers like to use titles such as “fund recovery specialist,” “asset recovery consultant,” “cyber intelligence expert,” “blockchain forensics analyst,” “ethical hacker,” “wallet recovery agent,” and “AML release officer.” The exact title does not matter much.

Authority

With some scams, the mask will be the authority. The fraudster is claiming to be a police officer, a financial authority operative, an appointed lawyer at a fraud case, or similar. If the scammer has obtained information about the previous scam, they can be very convincing, since they will seemingly know “everything” about your case, including your name and info, the name of the fake brokerage company, exactly how much money you lost, even when your transactions were made and which method you used. It all seems very legit. When the scammer claims that the funds have already been located, that frozen assets are waiting to be released, or that a court order is ready but needs a processing payment, it is very easy to believe them.

Cryptocurrency Recovery And Ethical Hackers

In cases that involve cryptocurrency, the recovery scammer often pose as an ethical hacker or someone specializing in blockchain asset recovery. The pitch often includes screenshots from a block explorer to make the story look technical. That is easy to fake because blockchain activity is public. Showing a transaction hash proves that a transaction happened. It does not prove the sender can reverse it, seize it, or return it. A scammer can paste your own transaction history back to you and call it “forensic work”. When you start asking questions, you are met with a huge wave of technical lingo.

The “ethical hacker” pitch is pretty easy to see through if you pause, step away, and look at it from a distance. A person who can actually “hack” a legitimate exchange, wallet, or smart contract and pull out funds, and is also willing to break the law, does not need to desperately sell their $250 recovery service to you. Sure, they can claim to be some type of vigilante, looking out for fraud victims, but you need to look beyond that lie. Also, even if the story were actually true, are you sure you want to be the one who pays someone to break the law?

Foreign Entity To Muddle The Waters

Scammers know that if they call a British fraud victim claiming to be from the UK FCA, that person will not find it overly complicated to get in touch directly with the UK FCA to verify the claims. Therefore, some of them create a more complex story by claiming to be a foreign entity. You might for instance be contacted by an alleged police officer in the Seychelles, who explains that the local authorities have clamped down on a group of fraudsters. If you just comply with how things are processed in the Seychelles, your money will soon be returned to you, the rightful owner.

Now, how do you verify this with the appropriate authority in the Seychelles? And maybe the police officer is telling you the truth when he explains that he is a part of a top-level secret anti-fraud task force, that is operating completely separate from the main police force to sidestep the rampant corruption on the Seychelles, and the official channels know nothing about their work? The water gets muddy and lies become more convincing when they are placed in an environment you know very little about and can not navigate with ease.

2. Capability

Whichever role the fraudster decides to play, it comes with very special capabilities. They are working for the police or justice department, and assets can only be unfrozen and released through them. Or they are ethical hackers or business insiders with backdoor access to exchanges or accounts. Sometimes, the capability is linked to very special technical solutions, such as private recovery software, MEV bots that can intercept funds, or a program that can hack a smart contract to reverse transfers on the Ethereum blockchain.

The fraudster will convince you that they are the key to recovering your funds, and that working with them is the path forward.

3. Asking For Money From You

At some point, the fraudster will ask for a payment. The justification will vary, depending on how the scam is tailored. It can be called a consultation fee, retainer, software deployment cost, anti money laundering certificate, wallet activation fee, release tax, insurance bond, exchange handling charge, or something else. The fee is a fraction of the money you lost, and paying it seems like the smart thing to do.

The victim pays, but no recovery happens. The excuses continue. More fees appear. A tax authority must be paid. A wallet must be verified. A smart contract needs gas. A regulator requires a compliance certificate. The victim is gradually bled for more and more money, and sunken cost fallacy will kick in. When you have already paid three times, it is difficult to cut your losses and refuse the fourth payment. Refusing means relinquishing all hopes of recovery and accepting that you have been scammed again, and this hurts.

A variation worth noting is the fake positive result propped up by a screenshot or official documents. The scammer claims recovery has already succeeded and can for instance show a dashboard with a large balance ready for release. This is meant to make the next fee feel rational. In trading terms, it is anchoring. If you think $80,000 is waiting behind a $2,000 fee, making the deposit is tempting. But balance is fictional, the portal is fake, and no money will be returned to you. The recovery service is just the wrapper for a scam.

Red Flags: Spotting A Fraudulent Recovery Agent

The easiest way to cut through the noise is to compare how legitimate entities behave against how recovery scammers behave. Police, banks, regulators, and authorized firms have processes. Scammers have urgency and a bunch of excuses as to why they are not following the normal process.

| Feature | Legitimate entity | Recovery scammer |

|---|---|---|

| Initial contact | You usually contact them through an official website, branch office, phone number, or email address. | They DM you, email you from nowhere, or reply under a post about being scammed. They suddenly show up on Telegram or WhatsApp. |

| Upfront fees | Reporting and basic investigation do not start with a payment request. | They ask for a consultation fee, software fee, retainer, tax payment, blockchain gas fee, and similar charges. |

| Guarantees | They do not promise 100% recovery. | They guarantee success, fast recovery, or claim that your funds are already located and ready for release. |

| Communication | Official domains, documented case references, and formal intake steps. | Gmail, ProtonMail, Telegram, WhatsApp, Signal, or changing usernames. |

| Pressure | They may stress speed for practical reasons, but not with emotional coercion. They are not likely to desperately need your cooperation. | They say the funds will be lost in hours unless you pay now. They use high-pressure sales tactics and can even become threatening. |

Initial Contact

If someone contacts you first and claims they can recover your money, it is almost certainly a scam, especially if they eventually ask for a payment. Legitimate banks, police, regulators, and licensed professionals do not cold message victims on Telegram, WhatsApp, X, Instagram, or YouTube comments promising urgent recovery. They do not ask for “activation fees,” “wallet synchronization,” “gas top ups,” or taxes before funds can be released. They do not guarantee success. The moment the contact begins with an unsolicited promise of recovery, the base rate shifts heavily against legitimacy.

Some sophisticated scammers are aware of this, and will use your email address (which is included in the suckers list) to contact you, which always feels more serious than a random message on Telegram. The rouse becomes even more believable if you have already used that email address to report the scam to the police and the financial authority, because suddenly you are getting “a response” from the entity you reported to.

The contact method matters more than most victims think. The FCA warns consumers about fake communications and clone firm tactics. A genuine authority does not need to find you in a comment thread. A genuine regulator does not ask you to transfer money to unlock a frozen wallet.

Always stop talking to anyone telling you:

- “I can reverse the transaction on the node.”

- “The funds are in a ‘holding’ wallet and just need a ‘gas fee’ to release.”

- “I have a contact at the FBI/SEC who is handling this privately.”

- “Our proprietary software can ‘force-ping’ the smart contract.

Guarantees

The guarantee is another clean tell. Legitimate recovery depends on facts that no outsider controls, such as where the money went, whether it passed through a bank or exchange with identifiable counter-parties, how much time has passed, whether law enforcement can get cooperation across borders, whether the receiving institution still holds anything, and so on.

That is why governmental agencies tell victims to report quickly, preserve records, and contact financial institutions at once. None of them promises a certain outcome. The scammer does, because certainty sells better.

Website Watch-Outs

To seem more trustworthy, the scammer may copy the website of a real entity, such as a financial authority or a well-known law firm. With the help of AI, cloning is a site has become very quick and easy. The cloned site is then put on a believable domain, and a few small details are changes, such as contact information and payment information.

This is where checking the exact domain name and contact information matters. Verify through official channels and not through a link they sent you. If they claim to work with the SEC or FBI, pause there. Agencies do not outsource recovery to random inbox warriors. The story usually falls apart once you compare the pitch to the real institution’s stated process.

Due diligence and being nosy are good things. Investigate the domain name and the website. If a supposed recovery firm or governmental agency appeared on this domain three months ago, hides ownership, and has no verifiable history, that is not a good start.

A firm claiming 10 years of recoveries should not be operating from a domain first registered six weeks ago. Of course, a savvy scammer will give you all kinds of excuses if you pressure them on this. There has been a major reorganization within the government. They are assigned to a special task force who keep a separate website. You are being onboarded through a special VIP site for improved service.

Fake Testimonials

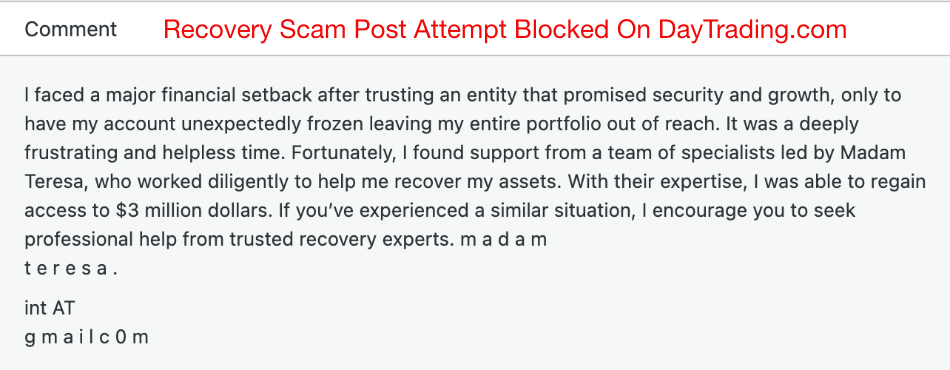

For recovery scammers pretending to be a paid service provider rather than a governmental entity, the fake testimonial is a standard move. You will see comments under YouTube videos, Reddit threads, X posts, and scam victim forums saying “Agent Mark got my 5 BTC back” or “message Dr Sarah Recovery on Telegram.” It does not cost much to pay a service to place comments like these online. As you might have noticed, they often arrive in clusters. The same provider that sold the original scam kit can help manufacture social proof for the recovery layer.

We’ve seen this in action firsthand. Users can leave comments on our broker reviews to share their feedback about their own trading experiences. However, recovery scammers sometimes try to seize these as opportunities to get their attention with their own comments. We never let these get published on the site. In fact, we have manually caught, reviewed and trashed over 1,650 such comments from recovery scammers before they could go live on DayTrading.com. We’ve read all these scammers’ posts, and they often sound convincing. Below is one such example (do not email the address below – we are sharing this for example and warning purposes).

The Hidden Risk: Secondary Data Exposure

When contacted by someone who might be a recovery scammer, it can be very appealing to believe the story. Even if you hesitate, you might think that risking the fee (e.g. paying $1,000 to hopefully get $10,000 back) is worth it. It begins feeling like a legitimate risk/reward situation.

The problem with this thinking is that if this turns out to be a recovery scam, you can end up losing much more than the fee. The scammers already have information about you since the first scam, and they can now use the recovery scam to fill out any blanks, making you a prime target for identity theft.

With many trading scams, cash loss is only the first layer of the damage, since many trading scams are also data harvesting operations. If you uploaded KYC documents during scam #1, handed over your phone number, shared bank details, or similar, scammers already have the foundation for identify theft in their hands. If anything is missing, the recovery scam is a great opportunity for them to make sure they get those missing pieces of the puzzle, all under the guise of helping you prove you are the rightful owner of recovered funds.

This point matters because many victims focus on the lost deposit and miss the wider problem. The stolen deposit is gone, and it hurts. But stolen identity data can cause problems for years. It can be used in fresh scams, credit applications, account takeover attempts, fake support calls, and more. It can even be used in scams targeting other victims, which means your identity can begin to pop up in fraud cases around the world.

Once your documents are in criminal hands, they can travel further than the money did. A victim may spend months worrying about the lost deposit while the more durable problem sits in the background, waiting for a later credit application, exchange account reset, or impersonation attempt.

If you have parted with sensitive information during scam #1 or during the recovery scam, treat that as a data breach. Examples of sensitive documents are copies of passport pages, driving license, national ID card, selfie, utility bill, and proof of address. Such documents can be used to support impersonation, open accounts, attempt credit applications, help bypass checks on legitimate platforms, or defraud other victims.

Many regulators around the world are now publishing guides about what to do after a data breach, including fraud alerts and temporary credit freezing. While there are no guarantees, there are steps you can take to reduce the risks. Ideally, try to find one that pertains specifically to the country you live in, since the exact steps will vary. Here is an example of a guide published by the Federal Trade Commission in the United States: https://www.identitytheft.gov/Info-Lost-or-Stolen. In the UK, Cifas Protective Registration exists for people worried their details may be misused.

There are reasons why authorities are taking this seriously. A lost deposit is often a one-off hit. A compromised identity, exposed inbox, or remotely accessed device can create repeated losses for the individual long after the first scam fades from memory, and it also reduces overall trust in the documentation and systems we use to prove our identity.

Your post scam response should always include identity protection, password resets, account review, and device security steps, not just a search for the money trail. In many cases, the smartest financial move after a scam is not the fantasy of full recovery. It is preventing more losses and friction before it happens.

Remote Access Means You Should Assume Device Compromise

Many recovery scammers push victims to install remote access tools so they can “set up a secure wallet,” “verify the chain in real time,” or “help process the refund”. That pitch is not new. The FTC’s guidance on tech support scams warns that scammers use remote access to steal financial information, capture credentials, install malware, and more. The FTC has also stated plainly that it will never ask for remote access to your device in order to deliver a refund, and any caller who does is a scammer. See the FTC warning.

If you gave a suspicious party access (e.g. through AnyDesk, TeamViewer, Chrome Remote Desktop, or similar software), work from the assumption that the device is now compromised. That does not mean every machine has a persistent backdoor installed. It means you cannot safely assume the opposite. Your device needs to be purged. Consider a full reset or professional malware review.

You also need to access relevant accounts from a clean device and carry out safety steps such as changing passwords and reviewing sessions.

Why “Blockchain Reversal” Is A Myth

The phrase “we can reverse the blockchain” should end the conversation. Public blockchains are built so confirmed transactions become extremely hard (in practical terms impossible) for an outside recovery agent to reverse. Blockchains rely on network consensus and transaction finality rather than a central payment administrator who can simply unwind entries because a third party requested it.

Example: Ethereum’s documentation explains finality as the point where a transaction is in a block that cannot change without a very high economic cost. Educational guides from public institutions and standards bodies describe the same property as immutability. Once recorded, transactions are not erased or edited out of the ledger.

A standard card payment (e.g. VISA or MasterCard) can be disputed because there is an issuer, an acquirer, and a rules framework above the transaction. A public blockchain transfer has no built-in chargeback desk. Once assets move from your wallet to another address and the network finalizes the transfer, there is no admin panel where someone can click “reverse”. There may still be ways to identify where the assets moved next, and there may be points where those assets hit a centralized exchange or service provider. But tracing is not reversing. Those are different verbs, and scammers blur them on purpose.

Tracing the money is not enough to be able to reverse a transaction. This often requires a police-led seizure at a centralized exchange.

A brief note on Layer 1 (L1) and Layer 2 (L2) finality helps clear up another common misunderstanding. L1 and L2 stand for different “layers” in blockchain architecture. L1 (Layer 1) is the base blockchain itself, e.g. the Ethereum blockchain or the Bitcoin blockchain. It handles consensus (how the network agrees on transactions), security, and final settlement of transactions.

L2 (Layer 2) is a secondary system built on top of an L1 to improve speed and reduce costs. Examples include rollups and sidechains. L2s can process transactions off the main chain and then post results back to the L1 for final settlement. They rely (to varying degrees) on the L1 for security. In other words, the L1 is the main highway (secure but can be slower and more expensive). The L2 is an express lane built on top of the L1. It is faster and/or cheaper, but still ultimately connects back to the highway.

On an L1 such as Ethereum, transaction finality is tied to the base chain’s consensus rules. Ethereum’s current proof of stake model uses checkpoints and validator votes to reach finality. On L2 systems, transaction handling may look fast to the user, but final settlement still depends on the rollup or bridge design and, in many cases, the underlying L1. That can affect when a transaction is considered safely settled. It does not create a consumer-style reversal button. Faster UX is not the same as reversible settlement.

So what is real in crypto recovery? Tracing can be real. Preservation requests can be real. Exchange compliance review can be real. Court orders can be real. Law enforcement cooperation can be real. But a stranger with “special software” claiming they can unwind a finalized on chain transfer after you pay a release fee is selling fiction.

The immutability reality:

Layer 1 (The Highway): Transactions on Bitcoin or Ethereum are settled by thousands of global computers. No single person has the “admin password” to delete a transaction.

Layer 2 (The Express Lane): While these are faster, they eventually “settle” on the Highway. Once that happens, the transaction is permanent. Speed Reversibility

The Real Steps To Recovery

None of the steps outlined here can guarantee that you will get your money back or that the fraudsters will be punished. And that is another reason why recovery scams work so well. Many of us have reported fraud, theft or other crimes to the relevant authorities in the past, with no to meagre results. We stumble upon someone who seems super confident in their ability to actually do something, and we are eager to believe it.

Still, the boring (and often futile) steps required to report fraud through official pathways are the way to go. Any shortcut greatly increases the risk of ending up the victim of a recovery scam.

Contact Your Bank, Card Issuer Or Other Payment Processor First

The first priority is to stop money that has not left yet, and (when possible) reverse the transaction for any money that has already left. This step will also involve putting safety measures in place to shut down additional transaction attempts.

If any part of the loss involved a credit card, debit card, bank transfer, or wire, contact the service provider immediately through the provider’s emergency number or 24/7 live chat. A meek email that might be read next week is not enough. Tell the service provider the transaction was fraudulent and ask them to block or reverse it where possible. Contact both your bank and any receiving bank, and request a recall. Timing matters and any delay means the money becomes more difficult to retrieve. You are also more likely to be held responsible for fraudulent credit card transactions if you do not react immediately.

Be factual and have all relevant information ready. Give dates, amounts, account references, wire confirmations, card statements, wallet addresses, exchange account IDs, screenshots of chats, and every invoice or payment instruction you received. Do not bury the bank in a 12-page story about your feelings toward “Lisa from compliance”. Give them a clean record they can use. The help desk staff are looking for transaction data and fraud indicators. Do not waste precious time trying to make them your personal grief counseling team instead of going after your money.

File A Police Report And Preserve The Paper Trail

A police report does not guarantee recovery, but it creates a formal record which can be important down the line. That record matters when you speak to banks, exchanges, insurers, and regulators. Each country has their own reporting path. In some countries, you contact the police through the standard channels, while other countries have dedicated points of contact specifically for frauds or online crimes.

Here are examples from the UK and the USA.

- For the UK: https://www.reportfraud.police.uk

- For the USA: The Internet Crime Complaint Center (IC3)

USA.gov also maintains a reporting guide that helps route complaints to the right agency.

Properly reporting the crime supports investigative and intelligence purposes, can help with fund recovery, and moves a loss from “bad story on the internet” to “documented incident with reference numbers”.

Use the relevant national or local reporting route. Preserve originals. Do not edit screenshots. Export emails with headers included. Save wallet addresses, hashes, timestamps, and exchange deposit memos.

Important: You Can Do The Reports Yourself

Recovery scammers often claim they will contact relevant banks, file with the SEC, open an FBI recovery case, or similar on your behalf. Do not agree to this. Do not pay for this service or share any information. You do not need a stranger in Telegram to contact your bank or submit a basic police report on your behalf. You can do that yourself through official channels. If you absolutely need help and are willing to pay, reach out to a lawyer instead, through official channels. You should do the reaching out. Do not trust a lawyer who suddenly pops up in your inbox.

Note: Scammers often claim foreign connections to muddy the water

As discussed further up in this article, scammers often fake a foreign connection to make the scam more believable. If they notice that you have no problem dealing with local authorities on your own, they step things up by claiming a foreign report is necessary for recovery. If you are outside the United States, they can claim you need to file a report with the FBI / SEC / CFTC / FTC or some other U.S. agency, and that you can only do this through them.

If you are in the United States, they claim to represent the authorities of the Seychelles, Vanuatu or similar, and going through your new friend on Telegram is the only way for these authorities to take your case seriously. Scammers might even claim that corruption is so rampant in that location or specific agency that you need them and their “special contacts” to recover your funds.

Regardless of the details of the scam, the main point is that they want you to feel helpless, as if you can not move forward without their very special help. Do not fall for this.

Notify The Cryptocurrency Exchange, But Keep Expectations Realistic

If the funds moved to a known centralized cryptocurrency exchange, contact that exchange through official support or security channels immediately. Provide them with the relevant information, including your police report reference number. This is one of the few points in crypto where a human institution may be able to act.

Typically, reporting the case to the exchange is not enough. Instead, your local law enforcement also needs to reach out to the exchange through the appropriate channels. Coinbase states that it can freeze or block assets when required by law or court order, and says it fully cooperates with law enforcement investigations. Binance provides a law enforcement request system for government agencies and requires supporting documents. That means an exchange may preserve records or restrict movement in response to a valid legal process. It does not mean a private recovery agent can call the exchange and bounce your coins back by lunch.

When you contact an exchange, give them the transaction hash, sending address, receiving address, amount, date and time, any related user ID, and your police or case reference if you have one. Be precise. Exchanges handle abuse, security, and legal requests in large volume. A message saying “please help I got robbed by this evil genius” may be emotionally true, but it is operationally weak.

Accept The Hard Truth About Odds And Timelines

Some recoveries happen. Many do not. International fraud, cross border shell companies, mixers, mule accounts, and rapid onward transfers make recovery difficult even when the victim does everything right. Keep your expectations realistic.

The useful move is not to buy hope from the next person offering certainty. It is to improve the only variables you still control: speed of reporting, quality of records, scope of notifications, and protection against further loss.

The FBI, FTC, OCC, and FCA guidance all point in that same direction, even when they use different language. Recovery is never guaranteed, but you can increase your odds by acting quickly and correctly.

FAQs

Can The Police Actually Get My Crypto Back?

Sometimes, yes. Often, no. The outcome depends on many things, including your speed, the speed of the investigation, applicable jurisdiction or jurisdictions, whether the assets can be traced to a service provider that keeps records, whether the receiving platform will cooperate or can be forced to cooperate, and whether the assets are still there when legal process arrives.

Police and federal reporting channels are still worth using because they create the record needed for subpoenas, production orders, exchange requests, and intelligence matching across cases. But no honest authority will promise recovery or make it sound simple.

Why Are There So Many Recovery Ads On Google And Facebook?

Because ad review is imperfect and fraud economics are good enough to fund constant re-entry. Platforms remove bad actors, but scammers can rotate domains and account identities quickly. Regulators have spent years warning consumers. A sponsored result, a polished landing page, or a verified-looking profile is not proof of trustworthiness. That sounds obvious until someone has just lost $40,000 and sees a sponsored ad promising “98% recovery success”. At that point, we really want to believe this is a possible path.

Is This Recovery Company A Scam?

If the promise is more than what is logically possible, the answer is most likely YES.

If you still want to give them the benefit of the doubt, do your due diligence first. Check whether the firm is on a regulator warning list. (But scammers are known to frequently change names.) Check if the company is actually registered somewhere and how long it has been active. Search the domain in the ICANN lookup tool. Review the contact details, company records, and whether the website domain age matches the story being told. If the firm claims regulatory standing in the U.S. or UK, verify that through official regulator tools and contact channels, not links they supplied.

Review sites are not evidence and are frequently compromised. A one-month-old “recovery company” with 300 perfect reviews is cause for suspicion.

Are Lawyers Legitimate In Recovery Cases?

Yes, sometimes. But a real lawyer does not need to promise guaranteed recovery, fake a regulator relationship, or ask for crypto to “unlock” the case. The useful test is ordinary due diligence. Look for verified firm identity, bar registration or similar where applicable, documented engagement terms, clear jurisdiction, and no fantasy claims about reversing the blockchain. Legal action can help in cases involving known defendants, banks, exchanges, injunctions, or discovery. It does not rewrite transaction finality.

Also, reputable and successful law firms are typically not chasing down clients on Telegram, looking for “gas money” to recover a blockchain transaction. If you need a lawyer, you should be the one to initiate contact.

Recovery Scams Are Not Limited To The World Of Online Financial Trading

If we zoom out and look at this field from a distance, we see that recovery scams are actually not limited to trading platform frauds and similar 21st century problems. They are actually much older than the advent of online trading and they are not even limited to financial trading. When we look at it from this perspective, it becomes easier to notice the overall pattern; one that is not hidden in technical jargon about blockchain reversals and Remove Device Access.

One notable example is the timeshare fraud and the follow-up recovery scam. Timeshare fraud is a long-running type of scam where high-pressure sales tactics are used to convince victims to sign a timeshare agreement for a property, typically in a popular tourist location. The terms and conditions of the contract are horrible, and getting out of the contract proves to be very difficult. The victim is now stuck. Not only have they paid a lot of money for the timeshare, but they are also contractually bound to pay a plethora of fees associated with the property.

This is when the recovery scam steps in; someone who promises a way out. The timeshare recovery scams typically fall into a few common patterns:

- Exit scams: A company promises to legally cancel your timeshare contract. They can for instance claim to represent a specialized law firm that knows how to navigate certain legal loopholes. Or claim to have useful contacts in the local government that will help expedite the case. They charge upfront fees and then do little or nothing. Typically, they milk the victim for more and more fees and costs until the jig is up. If you have dealt with trading platform recovery scams, you will quickly notice a pattern here. The original scams are very different, but the recovery scams follow an eerily similar pattern.

- Rental scams: Fraudsters claim they can rent out your unused timeshare weeks for profit, but require listing marketing fees first. They charge fees but no rental money will ever materialize.

- Fake resale offers: Fraudsters contact the timeshare holder claiming they already have a buyer ready for the timeshare (often at a surprisingly high price), but step-by-step require upfront payments for processing, inspection, transaction taxes, closing costs, money transfers, escrow fees, and more. Once the contract holder has paid one or two fees, the famous sunk cost fallacy will kick in and it feels very difficult to pull the plug. This pattern is very common in trading platform recovery scams, where the fraudster claims that your money has already been recovered and is waiting for you, but you have to act fast and pay a fee (which then turns into many fees) to have the money released into your account. In both cases, the resolution will feel so close, and giving up hope becomes more and more difficult.

The trading platform recovery fraudsters did not invent the concept of using high-pressure tactics, official-looking documents, and impersonation of legitimate organizations in their recovery scams. We only have to take a look at reported timeshare scams from the 1900s to see how all these pieces of the puzzle were already in place. Time-share recovery frauds frequently involved people posing as government agents, licensed investigators, lawyers, or representatives for consumer protection organizations.

And the timeshare scammers also had access to suckers lists, and were sometimes even the same organization as the one who sold the timeshare in the first place. They also exploited existing networks, e.g. expat groups, to find suitable victims, just like trading platform recovery scammers hang around trader forums and Telegram groups to find out when someone has been scammed and is eager to do something about it.

The underlying psychology is also the same. Victims are more likely to engage with recovery fraudsters when they feel stupid and embarrassed, desperate to recover their money, or angry and looking for justice. When officials working within the law system prove to be useless, the situation heats up even more. It does not matter if scam #1 involved Bitcoin trading or a beach house in Marbella; the underlying human emotions are the same.

The recovery scam involving more than one jurisdiction was also common. You typically do not buy a timeshare in your local community. Instead, the typical victims for timeshare scams in Southern Europe would come from Northern Europe, the victims buying timeshare in Mexico lived in the United States and Canada, and so on. Few of them felt confident navigating the foreign legal system, and plenty of them did not even speak the language. When they were told that “special contacts in the government” were needed to resolve the situation, they understandably found that believable.

Examples of common warning signs for both timeshare recovery scams and online trading recovery scams:

- Being contacted out of the blue by someone who already knows about your situation

- Claimed authority, e.g. governmental agent, law firm, specialist

- Claims of special access, e.g. governmental contacts, a secret buyer list (for timeshares) or special tech (for Bitcoin recovery)

- Pressure to act quickly

- Requests for upfront fees before any service is performed

- The initial fee can feel reasonable in size (considering the situation), but new fees keep popping up

- Claims of a guaranteed success

- Being told to keep things confidential