Yield Cap Policy

In macroeconomics, a bond yield cap policy is a monetary policy tool used by a central bank, such as the Bank of Japan (BOJ), to influence the level of interest rates in the economy. It is a form of yield curve control (YCC).

A bond yield cap policy involves the central bank setting a cap on the maximum yield that can be paid on a particular type of bond, such as government bonds.

This policy can be used to help stabilize financial markets and maintain low interest rates, which can stimulate economic growth.

The BOJ has used a bond yield cap policy as part of its efforts to stimulate economic growth and combat deflation in Japan.

Under this policy, the BOJ sets a target yield for certain government bonds, and then uses its monetary policy tools to ensure that the yield on these bonds remains within a certain range around the target.

This can involve buying large quantities of government bonds in order to keep their yields from rising above the target, or using other tools such as negative interest rates to influence the level of interest rates in the economy.

Overall, a bond yield cap policy can be an effective tool for central banks to influence the level of interest rates and support economic growth, but it can also have potential drawbacks and limitations, such as potentially distorting financial markets or limiting the central bank’s flexibility in implementing monetary policy.

Key Takeaways – Yield Cap Policy

- A yield cap is a monetary policy tool used by central banks to maintain stability in the bond market and control long-term interest rates.

- It involves setting a target range for the yield on a specific government bond, such as the 10-year bond, and actively buying and selling bonds in the market to keep the yield within the target range.

- A yield cap can be used to support the economy by encouraging borrowing and investment, which can stimulate economic activity and potentially lead to higher inflation.

- It can have implications for traders and investors, as it can affect the supply and demand for government bonds and influence their prices and yields.

- Central banks may use yield caps in conjunction with other monetary policy tools, such as quantitative easing, to achieve their policy objectives. Traders and investors should be aware of the potential impact of these policies on financial markets.

Defending Yield Caps

Central banks can defend yield caps, which are limits on the interest rates that can be paid on certain financial instruments, in a number of ways.

One way is through the use of monetary policy tools, such as setting the target interest rate or engaging in open market operations.

For example, if a central bank wants to defend a yield cap on government bonds, it can raise the target interest rate to reduce demand for the bonds and keep the yield from rising above the cap.

Alternatively, the central bank could buy government bonds in the open market to increase demand for the bonds and push the yield down towards the cap.

Another way that central banks can defend yield caps is through the use of regulatory tools, such as setting limits on the amount of certain types of bonds that banks and other financial institutions are required to hold.

This can reduce the supply of the bonds in the market and help to keep the yield from rising above the cap.

It is worth noting that defending yield caps can be challenging and may not always be effective, particularly in the face of strong market forces.

Central banks must carefully consider the potential trade-offs and unintended consequences of their actions.

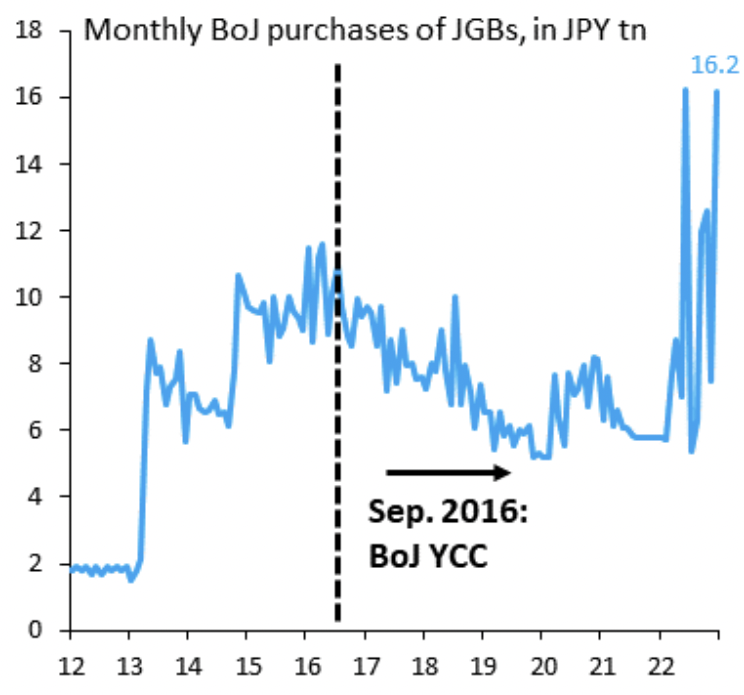

Example: BOJ in December 2022

BoJ lifted the ceiling for 10-year JGB yield from 0.25 to 0.50% in December 2022.

In doing so, it had to buy ¥16.2 trillion in JGBs to defend the new cap.

Exiting any peg – in this case a yield cap – can be extremely costly and is a warning for policymakers considering such a tool.

Yield Cap vs. Currency Devaluation vs. Changing Inflation Target

A yield cap, currency devaluation, and changing an inflation target are all tools that policymakers and central banks can use to influence economic conditions and achieve their policy objectives.

Here are some differences and similarities between these three tools:

Yield cap

A yield cap is typically used as a way to protect against rising interest rates in certain parts of its yield curve, and can be implemented by central banks as a monetary policy tool.

This is done by buying bonds at a certain yield threshold to prevent them going above.

A yield cap policy can help stabilize financial markets and maintain low interest rates when they are needed, which can help stimulate economic growth and achieve target inflation.

However, it can also distort market signals and eventually cause too much inflation or currency devaluation.

Currency devaluation

Currency devaluation refers to the act of lowering the value of a country’s currency in relation to other currencies.

This can be done through a variety of means, such as selling the country’s currency in foreign exchange markets, lowering interest rates, or changing the exchange rate regime.

Currency devaluation can be used as a tool to boost exports and stimulate economic growth, as it makes a country’s goods and services more competitive in the global market.

However, it can also lead to higher inflation and potentially create economic imbalances within a country.

Changing an inflation target

An inflation target is a specific level of inflation that a central bank aims to achieve through its monetary policy.

Central banks often use inflation targeting as a way to anchor expectations and provide a more predictable policy environment.

Changing an inflation target involves adjusting the target level of inflation that the central bank aims to achieve.

This can be done to reflect changes in economic conditions or to achieve other policy objectives, such as helping spur more economic growth or stronger financial markets.

Changing an inflation target can have implications for the central bank’s monetary policy stance and the level of interest rates in the economy.

Similarities between a yield cap, currency devaluation, and changing an inflation target

Some similarities between these three tools include that they can all be used to influence economic conditions and achieve policy objectives, and that they can all have potential implications for the level of interest rates in the economy.

However, they differ in terms of their specific mechanisms and the specific economic conditions and policy objectives they are intended to address.

Costs of Defending Yield Cap Policies

Managing a yield cap can be costly for a number of reasons.

One reason is that it can involve the central bank buying large quantities of bonds in order to keep their yields from rising above the target, which can be a significant financial commitment.

We saw this in the case of the BOJ’s defense of its interest rate peg.

This is because it’s holding interest rates at artificially low levels and private sector participants don’t want the bonds because of poor real returns (i.e., inflation is high relative to the rate of return on the bond).

If the central bank buys a large amount of bonds and then interest rates rise above the target yield, the value of the bonds declines, resulting in a loss for the central bank.

Additionally, managing a yield cap will require the central bank to have a deep expertise of financial markets and the underlying mechanics involved. It will need to be able to anticipate market movements in order to effectively implement the policy.

Defending a yield cap is costly for similar reasons to devaluing a currency

Managing a currency devaluation can also be costly for similar reasons.

Devaluing a currency can involve the central bank selling large quantities of its own currency in foreign exchange markets in order to lower its value.

Additionally, currency devaluation can have implications for a country’s balance of payments and exchange rate stability, which can be costly to manage.

Overall, both yield cap management and currency devaluation can be costly because they can involve significant financial commitments.

They can also have potential implications for the economy and financial markets, which can require careful management and potentially involve additional costs.

Suspension of a Yield Cap Policy

There are a number of factors that central banks may consider when deciding whether to suspend a yield cap policy.

Some possible reasons for suspending a yield cap policy include:

The policy is no longer needed to achieve the central bank’s policy objectives

If the policy has achieved its intended effects and is no longer needed to support the central bank’s policy objectives, the central bank may decide to suspend the policy.

This effectively allows yields to achieve their natural levels.

The policy is having unintended consequences

If the policy is having unintended consequences that are detrimental to the economy or financial markets, the central bank may decide to suspend the policy.

For example, the policy may be distorting financial market signals, creating inflation, asset bubbles, or currency devaluation.

The policy is becoming too costly

If the policy is becoming too costly to maintain, the central bank may decide to suspend it.

This could be due to the central bank incurring losses on its bond purchases or other costs associated with implementing the policy.

Overall, whether it is wise for a central bank to suspend a yield cap policy will depend on the specific economic conditions and policy objectives of the central bank, as well as the potential implications of suspending the policy.

The central bank will need to carefully weigh the costs and benefits of suspending the policy in order to make an informed decision.

How Can Traders Know When a Yield Cap Policy is Unsustainable?

There are a number of signs that traders can look for to determine whether a yield cap policy is unsustainable.

Some possible indicators that a yield cap policy may be unsustainable include:

The policy is having unintended consequences

If the policy is having unintended consequences that are detrimental to the economy or financial markets, it may be unsustainable.

For example, the policy may be distorting financial markets (e.g., asset bubbles) or limiting the central bank’s flexibility in implementing effective monetary policy (e.g., due to too-high inflation).

The policy is too costly

If the policy is becoming too costly to maintain, it may be unsustainable.

This could be due to the central bank incurring losses on its bond purchases or other costs associated with implementing the policy (e.g., inflation from buying the bonds to hold interest rates artificially low).

Market participants are no longer responding to the policy

If market participants are no longer responding to the policy as intended, it may be unsustainable.

For example, if the policy is no longer having the desired effect on interest rates or financial markets, it may be at risk of being broken up.

There are alternative policies available

If there are alternative policies available that may be more effective at achieving the central bank’s policy objectives, the yield cap policy may be unsustainable.

Traders can monitor economic and financial market conditions and look for changes in the effectiveness of the yield cap policy in order to determine whether it may not be sustainable.

It is important for traders to stay informed about the central bank’s policy objectives and any changes to the policy in order to make informed decisions about their portfolio positions.

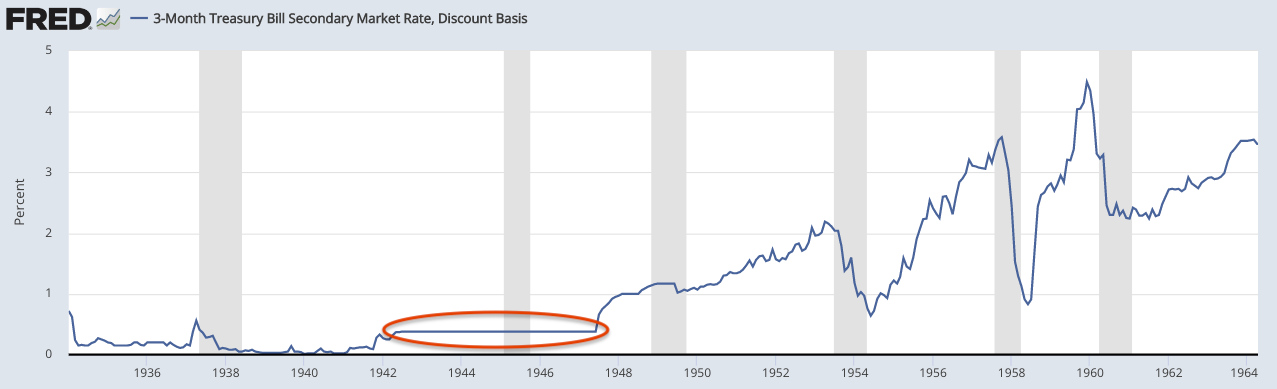

US Yield Cap Policy on Treasuries during World War II

During World War II, the US government implemented a policy known as a “yield cap” on Treasury bonds in order to finance the war effort.

Yield caps were a type of price control that regulated the maximum yield that could be paid on certain types of government securities, including Treasury bonds.

The purpose of yield caps was to keep the cost of borrowing for the government low, by preventing investors from demanding higher yields in order to compensate for the increased risk associated with lending to the government during a time of war. (There is normally high inflation during war periods because of all the extra spending.)

The yield caps were set at levels that were below the market rate of return, which meant that investors who purchased Treasury bonds during this time were effectively giving up some of the potential returns they could have earned in a more normal market environment.

Yield caps were used extensively during World War II, and were in place for a number of years after the war ended.

They were eventually phased out in July 1947 as the US economy returned to a more normal state.

The effect of yield caps in the 1942-1947 period can be seen below.

Yield Caps During War Periods or Times of National Emergency

Yield caps can be a useful policy tool for governments in certain circumstances, such as when a country is facing a major national emergency or crisis that requires significant public resources to be directed toward a particular goal.

For example, during times of war, governments may need to borrow large sums of money in order to finance military operations and other war-related expenses.

In such cases, yield caps can help keep the cost of borrowing low by preventing investors from demanding higher yields due to increased risk.

In a free market system, the allocation of resources is generally determined by the forces of supply and demand.

However, in certain situations, the free market may not allocate resources in the most efficient or desirable way.

For example, if a country is facing a major national emergency or crisis, the demand for certain goods or services may increase dramatically, while the supply may not be able to meet that demand.

In these cases, the government may need to intervene in order to ensure that the necessary resources are directed toward addressing the crisis.

Yield caps can be one way for governments to achieve this goal, by regulating the cost of borrowing and ensuring that funds are available to finance the necessary activities.

It is worth noting, however, that yield caps can also have some negative consequences.

For example, by artificially suppressing the market rate of return on certain types of securities, yield caps may discourage investors from purchasing those securities, which can reduce the overall supply of capital available for investment.

Additionally, yield caps may create an unfair advantage for some investors, who are able to earn higher returns on other types of investments that are not subject to yield caps.

As a result, yield caps are generally only used in limited circumstances, and are typically only implemented for a temporary period of time.

Yield Cap Policy vs. Yield Curve Control

Yield caps and yield curve control are two related but distinct policy tools that can be used by governments and central banks to influence the level of interest rates in an economy.

Yield caps are a type of price control that regulate the maximum yield that can be paid out on certain types of government securities, such as Treasury bonds.

Yield caps are sometimes used in times of crisis or emergency, when the government needs to borrow large sums of money in order to finance its spending needs.

Yield curve control, on the other hand, is a monetary policy tool that is used by central banks to influence the shape of the yield curve, which is a graphical representation of the relationship between the yields on bonds of different maturities.

Central banks can use yield curve control to target specific levels of interest rates for different maturities of government securities, in order to achieve specific policy objectives.

For example, a central bank might use yield curve control to try to keep short-term and mid-curve interest rates low in order to stimulate economic growth, while simultaneously keeping long-term interest rates higher (by letting them float) in order to curb inflation and financial excesses.

While yield caps and yield curve control are both designed to influence the level of interest rates in an economy, they work in different ways and are used for different purposes.

Yield caps are a type of price control that regulate the maximum yield that can be paid on certain types of securities, while yield curve control is a monetary policy tool that is used by central banks to target specific levels of interest rates across the yield curve.

FAQs – Yield Cap Policy

Why is Japan doing yield curve control?

Japan implments a policy known as “yield curve control” (YCC), under which it aims to keep the yield on certain government bonds within a specified target range.

More specifically it is a yield cap policy, targeting a specific bond duration. But it is a form of YCC, so the term has stuck in describing Japan’s situation.

The Bank of Japan (BOJ), the country’s central bank, has been implementing YCC since September 2016 as part of its monetary policy.

Under YCC, the BOJ sets a target for the yield on the 10-year Japanese government bond (JGB) and actively buys and sells JGBs in the market to keep the yield within the target range.

The goal of YCC is to maintain stability in the bond market and control long-term interest rates, which can affect the cost of borrowing for households and businesses.

The BOJ introduced YCC as a way to support the Japanese economy, which has been struggling with low inflation and slow growth for many years.

By keeping long-term interest rates low, YCC is intended to encourage borrowing and investment, which can help stimulate economic activity.

Why has the BOJ’s yield cap policy not caused inflation?

Japan has experienced very low inflation in recent years, which is a phenomenon known as “deflation.”

Deflation is a sustained decrease in the general price level of goods and services, which can occur when the supply of money is not growing as fast as the demand for goods and services.

There are several reasons why Japan has not suffered from high inflation in recent years.

One reason is that the Japanese economy has been facing a number of structural challenges, such as an aging population, low productivity growth, and a high level of public debt.

These factors have tended to hold back economic growth and limit the demand for goods and services, which can put downward pressure on prices.

Another reason is that Japan has implemented a number of monetary policy measures, such as quantitative easing and yield curve control, which have helped to keep long-term interest rates low. Low interest rates can encourage borrowing and investment, which can help boost economic activity and potentially lead to higher prices.

However, in Japan’s case, these measures have not been successful in generating sustained inflation.

There could be other factors as well, such as changes in global economic conditions and the impact of technological advances on prices.

Conclusion – Yield Cap Policy

Yield cap policy is a form of yield curve control that is used by central banks to target specific levels of interest rates across the yield curve.

It is implemented in order to maintain stability in the bond market and control long-term interest rates, which can affect the cost of borrowing for households and businesses.

Japan has been using yield cap policy since September 2016 as part of its monetary policy, but it has not yet resulted in sustained inflation due to a variety of structural factors and other economic conditions.

Yield caps are often done away with when inflation rises, when they distort financial markets, or cause a currency to depreciate more than what’s appropriate.