How Hedge Funds Work: Structure, Technology, and Managing Risk

This guide covers three core parts of hedge funds: how they are structured, the technology they rely on, and how they manage risk. We’ll look at the legal setup, service providers, data systems, trading infrastructure, and risk controls that support hedge fund operations.

Use the links below to jump straight to the section you’re most interested in:

Hedge Fund Structure

A hedge fund is a type of investment vehicle that pools together money from a group of investors and uses that money to speculate on a variety of assets, such as stocks, bonds, commodities, and derivatives.

Hedge funds are typically structured as limited partnerships or limited liability companies, and are largely unregulated compared to traditional mutual funds.

In a limited partnership structure, the hedge fund has one or more general partners who manage the fund and make investment decisions on behalf of the investors, known as limited partners.

The general partners are responsible for the day-to-day operation of the hedge fund and are typically compensated based on a percentage of the fund’s profits.

The limited partners, on the other hand, are passive investors who provide capital to the fund and share in the profits and losses of the fund, but do not have any say in the investment decisions.

In a limited liability company (LLC) structure, the hedge fund is owned by its members, who are typically the general partners.

The members of the LLC have managerial control over the fund and are personally liable for the debts and obligations of the fund.

However, their liability is limited to the amount of capital they have invested in the fund.

Both limited partnership and LLC structures offer tax benefits to hedge funds, as the fund itself is not subject to corporate income tax.

Instead, the profits and losses of the fund flow through to the individual investors and are taxed at the individual level.

It’s worth noting that hedge funds are generally only available to accredited investors, which are individuals or institutions that meet certain financial thresholds.

This is because hedge funds are considered to be more risky and complex than traditional investment vehicles and are therefore subject to fewer regulatory protections.

In this article, we discuss the various components that make up a hedge fund structure.

Key Takeaways – Hedge Fund Structure

- Choose a Legal Structure

- Set up as a limited partnership or LLC.

- The fund manager is the general partner and investors are limited partners.

- Establish the Right Domicile

- Select a jurisdiction like the Cayman Islands, BVI, or Delaware for tax efficiency and regulatory flexibility.

- Appoint Key Service Providers

- Engage a prime broker (for trading and financing), administrator (for NAV and records), auditor, and distributor.

- Use a Master-Feeder Structure

- Set up onshore and offshore feeders that pool into a single master fund to serve US and international investors efficiently.

- Handle Tax Flow-Through

- Ensure profits and losses pass through to investors and are taxed individually.

- Avoids corporate tax at the fund level.

- Market to Accredited Investors

- Limit offerings to high-net-worth individuals and institutions to comply with regulations and reduce oversight.

- Manage Illiquid Assets with Side Pockets

- Segregate hard-to-value holdings to maintain fairness in redemptions and NAV calculations.

Prime Broker

A prime broker is a financial services company that acts as a single point of contact for hedge funds and other institutional investors when it comes to executing trades, settling transactions, and providing other financial services.

The main role of a prime broker is to facilitate the trading activities of its clients by providing them with a range of services that allow them to manage their investments more efficiently.

Some of the key services provided by a prime broker to its hedge fund clients include:

- Execution: A prime broker provides access to various exchanges and liquidity pools to help its clients execute trades at the best possible prices.

- Settlement: A PB handles the settlement of trades on behalf of its clients, which includes arranging for the transfer of securities and funds between parties.

- Financing: It may provide financing to its hedge fund clients through margin loans or other types of credit facilities.

- Reporting: A PB provides its clients with detailed trade and account reports to help them track the performance of their investments.

- Risk management: It helps its clients manage the risks associated with their investments by providing them with tools and resources to monitor and mitigate risk.

In addition to these core services, a prime broker may also provide its clients with a range of other services, such as collateral management, tax reporting, and regulatory compliance support.

The exact services offered by a prime broker can vary depending on the needs of its clients and the capabilities of the prime broker.

Administrator

An administrator in a hedge fund is responsible for the day-to-day operations of the fund and ensures that it is run efficiently and in compliance with regulatory requirements.

This may include tasks such as:

- Maintaining records of fund transactions, portfolio holdings, and investor information

- Calculating net asset values (NAVs) and distributing financial statements to investors

- Facilitating the onboarding process for new investors and managing the redemption process for exiting investors

- Coordinating with external service providers, such as custodians, prime brokers, and auditors

- Assisting with the preparation of marketing materials, such as offering documents and presentations

- Providing support to the fund manager and other investment professionals as needed

In addition to these operational duties, the administrator may also be involved in risk management, compliance, and regulatory reporting.

It is important for the administrator to have a strong understanding of the hedge fund industry and the regulatory environment in which the fund operates.

How To Start A Hedge Fund From Scratch

Auditor

An auditor is a professional who is responsible for independently reviewing and verifying the financial statements of a company or organization.

In the context of a hedge fund, the auditor’s role is to ensure that the fund’s financial statements accurately reflect the fund’s financial position and performance.

This includes reviewing the fund’s accounting records and procedures, testing the accuracy of the financial information, and expressing an opinion on whether the financial statements are presented fairly in accordance with relevant financial reporting standards.

The auditor’s role is critical in helping to ensure the integrity and reliability of the hedge fund’s financial information, which is important for investors and other stakeholders who rely on this information to make informed decisions.

Distributor

A distributor is a company that is responsible for marketing and selling securities, such as hedge fund units or shares, to investors.

In the context of a hedge fund, a distributor plays a key role in the fund’s marketing and securities distribution efforts.

The distributor works with the hedge fund’s management team to develop a marketing plan and to identify potential investors for the fund.

This may involve conducting market research to understand the needs and preferences of different types of investors, and developing targeted marketing materials and strategies to reach these investors.

The distributor may also work with financial advisors and other intermediaries to help promote the fund and to facilitate the sale of securities to investors.

In addition to marketing the hedge fund, the distributor is also responsible for facilitating the actual sale of securities to investors.

This may involve processing and tracking investment orders, providing investors with information about the fund and its investment strategies, and answering any questions or concerns that investors may have.

The distributor may also be responsible for maintaining relationships with existing investors and providing ongoing support and services to them.

Overall, the role of the distributor is to help the hedge fund reach and connect with potential investors, and to facilitate the sale of securities to these investors in a way that is compliant with regulatory requirements and best practices.

Legal Entity

The most common legal entity that hedge funds operate under is a limited partnership.

In a limited partnership, there are two types of partners: general partners and limited partners.

As explained earlier, the general partners of a hedge fund are typically the fund’s management team and are responsible for making investment and management decisions on behalf of the fund. They also have personal liability for the fund’s debts and obligations.

The limited partners, on the other hand, are the investors in the hedge fund and do not have any managerial control over the fund. They are only liable for the debts and obligations of the fund to the extent of their capital contributions.

Limited partnerships offer a number of advantages for hedge funds:

- They provide tax benefits, as the fund’s income is passed through to the partners and taxed at the individual level rather than at the corporate level.

- Limited partnerships also offer flexibility in terms of management and decision-making, as the general partners have broad discretion to make investment and management decisions on behalf of the fund.

Another legal entity that hedge funds may operate under is a limited liability company (LLC).

LLCs offer similar tax benefits to limited partnerships, as well as the added advantage of limiting the personal liability of the members (similar to shareholders in a corporation) for the debts and obligations of the LLC.

Why Hedge Funds Use a Master-Feeder Structure

The master-feeder structure is common.

Here’s what it aims at.

1. Tax Optimization for Different Investor Types

- US taxable investors (e.g., high-net-worth individuals, domestic institutions) typically invest through a US feeder (usually a limited partnership or LLC).

- Non-US investors and US tax-exempt entities (like pension funds or endowments) invest through an offshore feeder (usually domiciled in a tax-neutral jurisdiction like the Cayman Islands or British Virgin Islands).

- Both feeders invest into the master fund, which holds the actual investment portfolio.

Why this matters:

- Tax-exempt and foreign investors want to avoid US effectively connected income (ECI) and unrelated business taxable income (UBTI) that could be generated by direct US investments.

- US investors need structures that maintain pass-through tax treatment.

This setup keeps the different investor classes happy while allowing the manager to run one unified portfolio.

2. Operational Efficiency

- Without a master-feeder structure, the manager would have to replicate trades in multiple portfolios for each investor group.

- The master-feeder setup consolidates the portfolio, so the fund manager can execute a single strategy at scale.

- This results in reduced trading costs, simplified administration, and unified performance reporting.

- Since all trading activity happens within the master fund, auditors and compliance teams only need to review one central portfolio rather than reconciling multiple parallel ones.

- This reduces the cost and complexity of financial audits, regulatory filings, and internal controls.

- With all assets centralized, the master fund can calculate a single net asset value (NAV), which is then allocated proportionally to each feeder.

- This avoids discrepancies across multiple portfolios and ensures all investors – regardless of entry point – receive a fair and consistent valuation of their shares.

3. Regulatory Compliance and Flexibility

- US feeders are structured to comply with SEC and IRS rules for domestic investors.

- Offshore feeders are usually not subject to US securities laws, allowing more flexibility in marketing and disclosure requirements abroad.

- The master-feeder structure allows the fund to comply with multiple regulatory regimes simultaneously without needing separate portfolios.

- Eases cross-border fundraising by meeting local legal standards without restructuring the core investment strategy.

4. Marketing and Fundraising

- Many hedge funds want to attract global capital – from both US and international investors.

- Offshore feeder funds allow hedge funds to be marketed to international investors without triggering US tax or regulatory obligations.

- US feeder funds allow domestic investors to access the same strategies.

The structure therefore broadens the investor base without diluting strategy or adding tax complications.

Domicile and Taxation

As mentioned, hedge funds are typically domiciled in offshore financial centers such as the Cayman Islands, Bermuda, and the British Virgin Islands (BVI).

Luxembourg, Ireland, and the US are also common hedge fund domiciles.

This is because these jurisdictions often have favorable tax treatment for hedge funds, as well as a high level of financial privacy.

In terms of taxation, hedge funds are generally taxed as partnerships, rather than as corporations.

This means that the income and losses of the hedge fund are passed through to the individual investors in the fund, who are then responsible for paying taxes on their share of the fund’s income.

One of the main advantages of this structure is that it allows investors to defer paying taxes on their share of the fund’s income until they actually receive a distribution from the fund.

This can be beneficial for investors who are in a higher tax bracket and who might otherwise be subject to a higher tax rate on their share of the fund’s income.

Nonetheless, the specific tax treatment of hedge funds can vary depending on the country in which they are domiciled and the jurisdiction in which the investors are tax residents.

For those considering hedge fund investments, consulting with a tax professional is advised to understand the tax implications of investing in a hedge fund.

Investment Manager Locations

New York City and Connecticut are two of the most common locations for hedge funds and investment management firms.

Many hedge funds are headquartered in New York City due to the city’s financial hub and the availability of a skilled workforce.

Connecticut is also a popular location for hedge funds due to its proximity to New York City and the presence of a number of large financial institutions in the state. Connecticut also had no state income tax until 1985.

The historical association of having lower taxes than NYC and its more rustic location helped make the southwest portion of Connecticut (e.g., Westport, Stamford, Darien) a popular location for hedge funds.

In addition to these two locations, there are also many hedge funds and investment management firms located in other financial centers around the world, such as London, Singapore, and Hong Kong.

The specific location of a hedge fund or investment management firm may depend on a variety of factors, such as the type of investors the firm is targeting, the regulations in the jurisdiction, and the availability of skilled personnel.

Side Pockets

Side pockets are a mechanism used by some hedge funds to classify assets that are relatively illiquid or difficult to value.

These assets are placed in a separate, “side pocket” account within the fund, rather than being included in the fund’s main portfolio.

One reason a hedge fund might use side pockets is to allow the fund to hold onto an asset that may have temporarily decreased in value, but which the fund’s managers believe will eventually appreciate.

By placing the asset in a side pocket, the fund can avoid having to sell the asset at a loss, which would reduce the overall value of the fund.

Another reason a hedge fund might use side pockets is to manage the liquidity of the fund.

If the fund holds a large number of illiquid assets, it may be difficult for investors to withdraw their money from the fund in a timely manner.

By placing these assets in a side pocket, the fund can more easily manage the flow of cash in and out of the fund, and ensure that investors are able to receive their redemption requests in a timely manner.

It is important to note that side pockets are not used by all hedge funds, and their use can be controversial.

Some critics argue that side pockets can be used to artificially inflate the value of a fund, or to hide losses from investors.

As such, investors should carefully consider the use of side pockets when evaluating a hedge fund.

FAQs – Hedge Fund Structure

How are most hedge funds structured?

Hedge funds are investment vehicles that are typically structured as partnerships or limited liability companies (LLCs).

The general partner or manager of the hedge fund has discretion to make investment decisions on behalf of the fund and its investors, who are known as limited partners or members.

A prime broker is a financial services company that acts as a central clearinghouse for the hedge fund’s trades and provides a range of other services, such as securities lending and margin financing.

The prime broker is typically a large investment bank or brokerage firm.

An administrator is a third-party firm that provides back-office support to the hedge fund, including record-keeping, accounting, and regulatory compliance.

An auditor is a professional accounting firm that reviews the hedge fund’s financial statements to ensure that they are accurate and in compliance with relevant regulations.

The legal entity and domicile of a hedge fund depend on the specific structure that the fund has chosen and the laws of the jurisdiction in which it is established. Some common domiciles for hedge funds include the Cayman Islands, Bermuda, and the British Virgin Islands, due to their favorable tax regimes.

The taxation of hedge funds depends on the tax laws of the jurisdiction in which they are domiciled and the tax status of the investors. In some cases, hedge funds may be eligible for favorable tax treatment, such as the ability to defer or avoid tax on certain types of income.

However, the specific tax treatment of a hedge fund will depend on its individual circumstances.

What is the master-feeder hedge fund structure?

A master-feeder hedge fund structure is a way of organizing a hedge fund in which there are two separate legal entities: a “master fund” and one or more “feeder funds”.

The master fund is the main investment vehicle that holds the bulk of the assets and is where investment decisions are made.

The feeder funds are separate legal entities that are used to hold the assets of individual investors.

The investors in the feeder funds are typically not directly invested in the master fund, but rather they are exposed to the master fund’s investments.

This structure allows the hedge fund to efficiently manage the assets of a large number of investors and to accommodate different legal and regulatory requirements in different countries.

It can also make it easier for investors to invest in the hedge fund, as they can do so through the feeder fund rather than having to directly invest in the master fund.

Are private equity firms structured the same as hedge funds?

Hedge funds and private equity funds are both types of investment vehicles that are used to pool capital from investors and make investments in a variety of assets.

Hedge funds are typically structured as either limited partnerships or limited liability companies. The investors in a hedge fund are known as “limited partners” or “members”, depending on the legal structure of the fund.

The managers of the hedge fund, who make the investment decisions and manage the assets of the fund, are known as “general partners” or “managers”.

Hedge funds are typically subject to less regulation than other types of investment vehicles, and they often have more flexibility in terms of the types of investments they can make and the strategies they can use.

Private equity funds are typically structured as limited partnerships or limited liability companies, as well. Likewise, investors in a private equity fund are known as “limited partners” or “members”, and the managers of the fund are known as “general partners” or “managers” like hedge funds.

Private equity funds typically focus on making long-term investments in private companies, rather than trading securities on a shorter-term basis like hedge funds.

They are subject to more regulation than hedge funds, and they often have stricter requirements for the types of investments they can make.

Private Equity Fund Structure Explained

Conclusion – Hedge Fund Structure

A hedge fund is an investment vehicle that pools together capital from accredited investors or institutional investors and uses that capital to make a variety of investments, often with the goal of generating high returns.

Hedge funds are typically structured as partnerships, and the partners are the investors in the fund.

The general partner is responsible for making investment decisions and managing the fund, while the limited partners are the investors who provide capital to the fund and share in the profits and losses.

There are several key elements to the structure of a hedge fund:

- Prime broker: A prime broker is a financial institution that provides a range of services to hedge funds, including clearing trades, providing financing, and facilitating the settlement of trades.

- Administrator: An administrator is a third-party firm that is responsible for performing a variety of administrative tasks for the hedge fund, such as calculating net asset value (NAV), reconciling trade discrepancies, and preparing financial statements.

- Auditor: An auditor is a professional who is responsible for reviewing the financial records of the hedge fund to ensure that they are accurate and in compliance with relevant laws and regulations.

- Distributor: A distributor is a company that is responsible for marketing and selling the hedge fund’s investment products to potential investors.

- Legal entity: A hedge fund is typically organized as a legal entity, such as a partnership or limited liability company. The legal structure of the fund can have significant implications for the fund’s operations and the liability of its investors.

- Domicile: A hedge fund is usually domiciled in a particular jurisdiction, which can affect the fund’s legal and regulatory environment, as well as its tax treatment.

- Taxation: The tax treatment of a hedge fund and its investors can vary depending on the fund’s domicile and the tax laws of the investors’ home countries. It is important for hedge fund managers and investors to understand the tax implications of their investments.

Hedge Fund Technology (Data, Storage, Trading Systems)

Hedge funds rely on data analytics and advanced storage solutions to manage vast amounts of real-time and historical data, ensuring both performance and security.

Algorithmic trading systems central to many types of hedge funds (i.e., systematic in nature) require continuous refinement for executing trades and integrating with risk management systems for real-time portfolio monitoring.

Robust infrastructure with low-latency connectivity and redundant systems is important to support the trading environment of hedge funds.

Key Takeaways – Hedge Fund Technology

- Data: Hedge funds use real-time and historical data for informed decision-making, supported by analytics.

- Algorithms: Continuous refinement of algorithmic trading and risk management systems is important for trade execution and portfolio oversight.

- Infrastructure integrity: Hedge funds rely on low-latency infrastructure with redundancy to maintain a consistent and reliable trading environment.

Data: The Inputs into Decision-Making

Hedge funds depend heavily on data.

They require high-quality, real-time data to make informed decisions.

This data spans sources including market data, alternative data sets, news feeds, and transactional data.

(What kind of data they need will depend on their business and strategies.)

They also invest in quality data analytics platforms.

These platforms employ algorithms and machine learning techniques to identify trends and generate insights from massive datasets.

Storage Solutions

The enormity of data necessitates robust storage solutions.

Hedge funds use a combination of on-premises and cloud-based storage (e.g., AWS) to ensure both security and accessibility.

Cloud storage offers scalability, allowing funds to adjust storage needs on the fly.

On-premises solutions, often for sensitive data, comply with stringent security protocols to mitigate risks of breaches.

To ensure business continuity, hedge funds also implement disaster recovery plans.

These often involve storing backup data in geographically diverse locations.

Optimizing Trading Systems for Peak Performance

Algorithmic Trading

Algorithmic trading systems are the basis of many hedge fund operations.

These systems execute trades at speeds and volumes impossible for humans to match.

Algorithms are programmed to recognize market patterns, price movements, and execute trades based on pre-set criteria.

To keep these systems at peak performance, hedge funds continually backtest and refine their algorithms against historical data.

They’ll also forward test (i.e., make sure it does what it’s supposed to do in a live environment) and run other types of tests (e.g., Monte Carlo simulations).

Systematic + Discretionary

Sometimes funds will have a discretionary element to their algorithmic systems.

The system will spit out recommendations/guidance and the funds PMs/CIOs will decide what to do.

Risk Management Systems

Effective risk management systems are essential.

These systems monitor and analyze portfolio exposures to various risk factors, such as market volatility or currency fluctuations.

By doing so, hedge funds can adjust their trading strategies to keep tight risk controls.

Risk management technology must integrate seamlessly with trading systems.

This helps ensure real-time monitoring and rapid response capabilities.

Infrastructure

The infrastructure supporting trading systems must be both robust and reliable.

This means investing in high-quality hardware and ensuring low-latency connectivity.

Hedge funds often use dedicated servers and direct market access to reduce the time it takes to execute trades.

Redundant systems and network connections are also common.

This avoids downtime, which can be costly.

If they can’t run their system, they can’t generate revenue.

Quant Research At A Hedge Fund vs. Other Tech Careers

Managing New Data Flows In

When new data flows into a hedge fund’s systems, it initiates a cycle of updates and recalibrations across analytical models.

The data (e.g., market prices, economic indicators, prices of goods and services, transformations of price and volume data, etc.), is first cleaned and normalized to ensure its integrity.

It’s then integrated into existing datasets, where it can impact ongoing analyses and trading algorithms.

This integration process must be seamless to ensure that the fund’s decision-making process incorporates the most current information.

Forward Testing with Adjusted Parameters

Forward testing, often using methods like Monte Carlo simulations, allows a hedge fund to project how changes in strategy parameters might influence future performance.

By running a large number of simulations that incorporate random variations, analysts can assess the probability of various outcomes.

They can stress-test how robust the strategy would be to various shocks.

For example, how would the strategy do if inflation went up to 40% y/y?

How would the strategy do if unemployment went up to 50%?

These examples sound crazy (especially for a developed market economy), but this process is essential for understanding the potential risks and rewards of a strategy before it is deployed live in the market.

Forward testing provides a dynamic framework to evaluate the robustness of a strategy against the non-determinism and volatility of real-world markets.

Exploring What-If Scenarios

What-if scenario analysis is a strategic tool used to predict the outcome of an unusual or extreme event on investment portfolios.

Analysts create hypothetical scenarios – such as a sudden interest rate hike, a geopolitical event, or a market crash – to test how such events could affect asset values and investment/trading strategies.

This helps hedge funds in stress testing their portfolios and in formulating contingency plans.

The flexibility to simulate a variety of outcomes enables funds to anticipate and manage potential risks proactively.

Backtesting with a Changed Model

Backtesting is an important step when a hedge fund considers changing its investment model.

It involves applying the new model to historical data to evaluate how it would have performed in the past.

This retrospective analysis is key for uncovering any potential flaws or for understanding the conditions under which the model performs best or worst.

By doing so, the fund can gauge the potential efficacy and resilience of the new model before it is ever applied to live trading.

This mitigates the risk of untested assumptions and strategies.

Hedge fund CIO gives an easy explanation of quantitative trading

FAQs – Hedge Fund Technology (Data, Storage, Trading Systems)

What types of data are most important for hedge fund operations?

Market data, transactional data, alternative data sets, and real-time news feeds are important for hedge fund operations as they inform trading decisions and risk management strategies.

How do hedge funds store and secure their sensitive data?

Hedge funds use a combination of encrypted storage solutions – both on-premises for control and cloud-based for scalability – alongside strict access controls and regular security audits to secure sensitive data.

What technology infrastructure do hedge funds use for trading?

Hedge funds employ high-performance computing systems, low-latency networks, and direct market access technology to help with rapid and reliable trading.

How do hedge funds ensure data accuracy and integrity?

They implement:

- stringent data validation processes

- employ data governance frameworks, and

- use error-checking algorithms to ensure the accuracy and integrity of their data

What is algorithmic trading and how is it implemented by hedge funds?

Algorithmic trading uses computer algorithms to execute trades based on predefined criteria.

Hedge funds implement it to automate trading processes for efficiency and speed.

How do hedge funds use cloud storage in their data management strategies?

Hedge funds leverage cloud storage for its scalability and flexibility.

They often use hybrid models that combine public cloud resources with private cloud or on-premises data centers.

What are the key features of a hedge fund’s risk management system?

A hedge fund’s risk management system typically includes:

- real-time monitoring

- stress testing

- exposure analysis, and

- compliance checks to identify and mitigate potential risks

How is new market data integrated into a hedge fund’s existing trading systems?

New market data is integrated through automated data ingestion pipelines.

These help cleanse, normalize, and process the data to make it immediately available for trading algorithms and analysis.

In what ways do hedge funds backtest their trading strategies?

Hedge funds use historical data to simulate trades and evaluate a strategy’s performance under various market conditions.

They should also adjust for factors like slippage and transaction costs.

What role does artificial intelligence play in hedge fund technology?

AI in hedge fund technology is used for predictive analytics, pattern recognition, and automated decision-making.

Any way to enhance trading strategies and operational efficiency AI is likely used in some capacity.

How do hedge funds manage the latency in their trading executions?

Hedge funds minimize latency by:

- using co-located servers

- optimizing their trading code, and

- employing high-speed data transmission technologies

For HFT and other “high-speed” trading strategies, it’s more common to use a coding language like C++ (or sometimes Java) rather than Python.

What are Monte Carlo simulations and how do hedge funds use them?

Monte Carlo simulations are used by hedge funds to model the probability of different outcomes in financial markets by running a large number of scenarios to predict the performance of a portfolio (or some type of financial variable).

How do hedge funds perform forward-testing on their investment strategies?

Hedge funds conduct forward-testing by applying their trading models to out-of-sample data to predict future performance without risking actual capital.

What measures do hedge funds take to ensure business continuity in the face of technology failure?

Hedge funds will:

- implement redundancy systems

- have backup servers

- conduct regular disaster recovery drills, and

- maintain business continuity plans to manage technology failures

What considerations do hedge funds have when choosing between on-premises vs. cloud-based solutions?

When choosing between on-premises and cloud-based solutions, hedge funds consider factors such as data security, regulatory compliance, cost, scalability, and the ability to control and customize their IT infrastructure.

How Top Hedge Funds Really Manage Risk (and What You Can Copy)

If hedge funds have one real strength, it isn’t picking the hottest stock or calling the next major macro shift. It’s how they manage risk.

Many beginning traders imagine hedge funds as bold gunslingers.

They think of concentrated bets, calling the next big thing, exotic derivatives, or extreme leverage. And yes, some of that happens to some extent.

But in reality, risk management is the backbone. Even when something is presented in the media as a big bet, there are likely guardrails and offsets around the trade.

The best funds stay alive not because of bold predictions, but because of carefully designed risk frameworks.

Their job isn’t to be right all the time. It’s to never have unacceptable outcomes.

That difference explains why some of the best hedge funds survive decades while most individual traders flame out fairly quickly.

If you can limit your left-tail risk and keep drawdowns manageable, it’s much easier to grow your account and overall wealth.

We explore this more below and how you can copy how the very best traders and hedge funds accomplish this.

Key Takeaways – How Top Hedge Funds Really Manage Risk

- The irony is that the hedge fund model is built on principles most of us already know. Don’t risk everything on one bet. Don’t confuse luck with skill. Don’t put all your eggs in the same basket.

- It’s important to inculcate those rules seriously without exception.

- Survival before profits – Protect your capital first. Avoid positions that could wipe you out, no matter how tempting.

- Risk-adjusted thinking – Judge returns relative to the risk taken. Consistency matters more than big wins. Big losses aren’t compensated by corresponding big gains.

- Real diversification – Spread across strategies, asset classes, countries, currencies, and factors. Remember that most stocks are highly correlated.

- Guardrails and rules – Pre-define limits and follow them.

- Simple hedges – Use stop-losses, cash, or basic puts. Protection matters more than complexity.

Hedge Fund Risk Management Tactics

- Survival/defense first, profits second

- Focus on risk-adjusted returns (Sharpe, Sortino, drawdown metrics)

- Prioritize consistency over raw gains

- Diversify beyond stocks

- Across asset classes (equities, bonds, commodities, currencies, cash)

- Across factors (value, momentum, quality, volatility)

- Across strategies (macro, quant, defensive)

- Position sizing and exposure control

- Value-at-Risk (VaR) models

- Stress tests using past crises

- Strict drawdown limits

- Scale into and out of trades gradually

- Hedging and overlays

- Options, futures, swaps

- Macro hedges vs. position-specific hedges

- Correlation and regime analysis

- Track how assets move together in stress

- Adjust when correlations spike

- Liquidity management

- Maintain cash buffers

- Hold assets that can be sold quickly (or be compensated accordingly)

- Behavioral safeguards

- Hedge funds have strict independent risk teams

- Playbooks for volatility spikes and tail events (e.g., buying cheap OTM hedges well ahead of time)

- Scenario planning

- Culture of humility, constant review of assumptions

- Individual investor adaptations

- Set personal guardrails (max loss or drawdown limits)

- Keep a trading journal for discipline

- Size positions as a % of account, not dollar targets

- Mix strategies (trend, value, defensive, cash)

- Balance short- and long-term bets

- Use simple hedges (stop-losses, index puts, OTM options, uncorrelated assets)

Core Principles of Hedge Fund Risk Management

If you ask most what makes hedge funds successful, they’ll say it’s about spotting winners, timing markets, or pulling clever tricks with leverage.

But their real edge is much less glamorous. It’s risk management.

The best funds aren’t run by adrenaline junkies trying to outguess the market. They’re run by people obsessed with survival, consistency, and balance.

The principles are surprisingly simple; principles you can actually borrow for your own trading.

Survival First, Profits Second

Here’s the hard truth: if you blow up, nothing else matters. Hedge fund managers know this better than anyone. That’s why preserving capital is their north star.

Think about the math. Lose 50%, and you need to double your money just to get back where you started.

That’s a hole you don’t want to be in. So funds play the long game. They’ll gladly pass on a tempting bet if it risks crippling the portfolio.

This is what people mean when they talk about the “don’t blow up” mindset. It’s not about avoiding risk entirely, but about making sure no single mistake can take you out of the game.

Retail traders often chase home runs. Hedge funds are more like marathon runners pacing themselves. 1% gain one month, 0.5% loss one month, 2% gain one month, etc.

Stay in the race long enough, and you’ll have more chances to win.

Risk-Adjusted Returns, Not Absolute Returns

Here’s another big difference: hedge funds don’t care as much about raw returns.

To them, a trader who doubles their money by going all-in on risky bets isn’t a genius. They’re just lucky.

What professionals actually care about is how much return they generate for every unit of risk they take while keeping it within certain risk parameters.

That’s where metrics like the Sharpe ratio come in.

Imagine two portfolios: one makes 20% a year but swings up and down like a rollercoaster with 30% drawdowns common, the other makes 10% steadily with much less drama.

A hedge fund – especially if they want to attract institutional clients and keep them – is going to be in the second one every time. Because it’s more predictable and repeatable.

A sovereign wealth fund (i.e., an example of a hedge fund client) might not care much about the stock market. They might have a mandate of beating their domestic inflation rate by 5% each year, with volatility and drawdown limitations.

Risk-adjusted thinking changes how you see success.

Instead of asking, “How much did I make?” the better question is, “How efficiently did I earn it?”

That mindset is why so many top funds look “boring” compared to the myth of hedge funds as fearless gamblers. Consistency is the real criteria.

Diversification Beyond Basics

Many think diversification means owning a bunch of different stocks. That can help, but only to an extent.

Ask anyone who lived through 2008 or 2020; when people want out, most stocks move together.

Suddenly, a “diverse” portfolio is all sinking in the same boat.

Hedge funds approach diversification differently.

They don’t just spread across names, they spread across asset classes, factors, and strategies.

That means mixing stocks with bonds, commodities, currencies, and sometimes more unique, customized stuff.

It also means blending different styles: momentum, value, macro bets, arbitrage.

The idea isn’t to have more things in the portfolio, it’s to have things that don’t all depend on the same outcome.

Here’s an example: let’s say equities fall. A hedge fund might have government bonds or a volatility trade that helps to pick up the slack.

In good times, those positions may feel boring. In bad times, they’re the reason the fund keeps its drawdowns to reasonable levels.

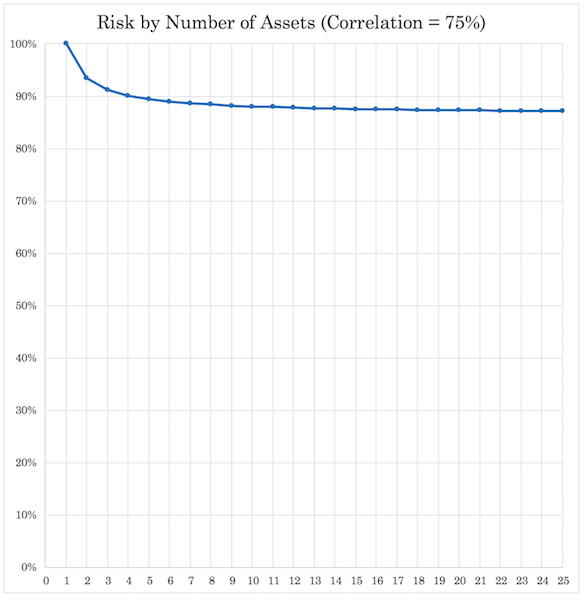

And this is why just owning more stocks have little marginal effect past a point. Adding your 41st stock to a portfolio of 40 doesn’t help much (or at all) if they all mostly move together.

In this article, we explained that if stocks are 75% correlated, on average, then adding more of them starts to flatten the marginal value (as it pertains to risk) quickly:

What matters is finding exposures that zig when others zag.

Tools and Techniques Used by Top Hedge Funds

Hedge funds have various ways to control risk. Some are technical and some are surprisingly common sense.

The goal is always the same: limit downside, stay liquid, and make sure no single event can knock them out.

Let’s break down a few of the most important ones.

Position Sizing and Exposure Control

One of the least glamorous, yet most critical, decisions a hedge fund makes is how big a position should be.

Most blow-ups in financial history didn’t happen because the original idea was wrong. They happened because someone bet too big.

Hedge funds use several tools to prevent that. Value-at-Risk (VaR) is one. In plain English, VaR estimates how much money you could lose in a worst-case scenario over a given period.

It’s not perfect. Critics argue it underestimates risk during crises. But it gives managers a yardstick for exposure.

On top of that, funds run backtests and stress tests.

They’ll feed portfolios through simulations of past disasters (the 2008 crash, the dot-com bust, the COVID panic) to see how much pain they’d suffer if history repeated itself. This helps them avoid blind spots.

They can even use synthetic data and simulate things where there is no historical precedent.

Then there are drawdown limits. Many firms have strict rules about how much loss they’ll tolerate before cutting exposure.

For example, if a portfolio falls 10% from its peak, managers may be forced to shrink positions until risk is back under control.

Finally, funds rarely “go all in.” Instead, they scale into and out of trades.

They’ll start small, see how the thesis plays out, and only build if conditions support it. It’s like dipping your toes in the water before diving in.

Hedging and Overlay Strategies

Another big part of the toolkit is hedging. At its core, hedging is just buying insurance.

Hedge funds know they can’t predict everything, so they pay up to protect against tail events.

They use derivatives like options, futures, and swaps for this purpose. A simple example: a fund holding a lot of equities might buy index put options.

If the market tanks, those puts rise in value and offset losses elsewhere.

There are two broad flavors of hedging:

- Macro hedges, which cover the entire portfolio against a big event like a recession or market crash.

- Position-specific hedges, which are more surgical, protecting a single trade from going sideways.

Hedges aren’t free and they eat into returns when things go well.

But that’s the trade-off: pay a little now so you don’t have unacceptable losses later.

The best funds think about hedges the same way you think about car insurance. You hope you never need it, but you’re glad it’s there if anything happens.

Correlation and Regime Analysis

Diversification only works if your assets don’t all move in the same direction. The trouble is that correlations change depending on the market regime.

In normal times, stocks and bonds may move independently. In crises, though, everything can suddenly crash together as liquidity dries up.

They measure how assets behave in stress scenarios – in the tails – not just in calm markets.

When correlations spike, managers adjust portfolios. That might mean cutting exposure in areas that have become dangerously tied together, or adding strategies that thrive in chaos.

A famous example: during the 2008 crisis, many assets that were historically uncorrelated suddenly became tightly linked.

The lesson is simple but important: diversification isn’t static.

You have to keep asking, “What happens if everything starts moving together?” Hedge funds don’t just assume yesterday’s relationships will hold tomorrow.

Liquidity Management

If there’s one lesson that repeats in financial history, it’s this: it’s not enough to be right, you also have to be able to get in and out when you want (and without extremely high transaction costs).

That’s what liquidity management is all about. Hedge funds keep cash buffers and invest in assets they can sell quickly. They don’t want to be stuck holding something that looks great on paper but can’t be exited when the market panics.

The collapse of Long-Term Capital Management (LTCM) in the 1990s is the classic cautionary tale. Their trades weren’t necessarily bad, but they forgot to take into account their own influence on the market. Liquidity dried up, leverage magnified the problem, and the fund imploded.

Archegos Capital in 2021 blew up for similar reasons. They held huge, leveraged positions in a few stocks. When those stocks dropped, Archegos couldn’t meet margin calls, and the whole thing unraveled almost overnight.

Top hedge funds never forget these lessons. That’s why they always keep a margin of safety.

The Bigger Picture

None of these tools (VaR models, hedges, correlation tracking, liquidity buffers) are perfect on their own.

Markets are too unpredictable for any single method to guarantee safety. But layered together, they form a powerful defense system.

Think of it like flying a plane. Pilots don’t rely on one gauge to stay in the air. They check altitude, speed, fuel, weather, and backup instruments.

Hedge funds do the same with risk. It’s constant monitoring, adjusting, and humility.

Take risk, but understand it and manage it well.

And while the execution can be complex, the underlying lesson is simple enough for anyone:

- size your bets carefully

- protect yourself with insurance

- don’t assume diversification always works, and

- keep enough cash so you’re never trapped

That’s how you stay in the game.

Behavioral and Organizational Risk Management

At the end of the day, risk management is as much about psychology and culture as it is about math.

The smartest hedge funds know this, which is why they don’t just rely on formulas.

They build organizational guardrails that keep egos, blind spots, and emotions from sinking the ship.

Let’s look at three key parts of this behavioral layer of risk management.

Independent Risk Teams

One of the most important safeguards inside a top hedge fund is the separation between traders and risk officers. The people making bets aren’t the same people policing risk.

Why? Because traders are wired to see opportunity.

They believe in their ideas, sometimes fiercely. That conviction is valuable; it’s what makes them pull the trigger on out-of-consensus trades.

But conviction can also morph into overconfidence. If you let the same person monitor risk, human nature kicks in. They’ll justify keeping a position longer than they should. They’ll bend rules to give themselves “one more day.”

Independent risk teams prevent that. They sit in a separate group, often reporting directly to the CIO or even the board.

They have the authority to say, “This position is too big” or “You’ve hit your drawdown limit, cut exposure now.”

In other words, they act as internal checks and balances. Traders push for returns, risk teams push for survival. That tension is healthy.

It’s the financial equivalent of having both an accelerator and a brake in the same car. Without it, you either don’t move, or you crash.

Playbooks and Guardrails

Another way hedge funds protect themselves is by not waiting until a crisis to figure out what to do. They create playbooks and guardrails ahead of time.

Think of it like a fire drill. You don’t want to be figuring out where the exits are when the building is already full of smoke.

Hedge funds run through “what if” scenarios in advance.

What if volatility suddenly doubles? What if the market gaps down 15% overnight? What if liquidity dries up and we can’t sell a major position?

These scenarios aren’t just academic exercises. They result in pre-defined rules.

For example:

- If volatility spikes past a certain level, cut position sizes across the board.

- If a portfolio suffers a 10% drawdown, reduce risk by 50% until stability returns.

- If a tail event occurs (say, a sovereign default), trigger a pre-set hedge or rebalance.

By having these responses codified, funds take emotion out of the equation.

In the heat of a crisis, it’s easy for fear or denial to take over. Playbooks are there so action happens automatically, without second-guessing.

Some funds even run crisis drills where they simulate market shocks and practice executing their rules.

It may sound over the top, but when the real thing hits, those rehearsals make the difference between panic and calm execution.

Culture of Humility and Adaptability

Finally, and maybe most importantly, the best hedge funds cultivate a culture of humility. They know markets have a way of humbling anyone who is highly certain of everything.

Overconfidence is one of the biggest risks in investing. The moment a fund believes “we’ve cracked the code,” it’s usually a bad path to be on.

Markets change. Regimes shift. What worked in the past and today may not work in the future.

To guard against this, top firms embed humility into their culture.

That doesn’t mean they lack conviction; it means they combine conviction with constant self-checks.

They regularly hold post-mortems on trades, asking: Were we right for the right reasons, or just lucky? Did we miss warning signs? Are our assumptions still valid?

This continuous review of assumptions keeps them adaptable.

Bridgewater, for example, is famous for its culture of debate. AQR is equally known for relentlessly questioning whether its factor models still hold up in the current market.

Humility also shows up in position sizing.

Even when a fund has a “high-conviction” idea, it rarely bets a significant portion of the portfolio. They always leave room for being wrong. That mindset (confidence tempered with caution) is what allows them to survive over decades.

The Human Side of Risk

When you step back, all these organizational safeguards (independent risk teams, playbooks, humility) are about protecting against human nature.

Markets tempt us to overreach when things are going well and to freeze when things turn bad. Hedge funds know this, so they design systems that keep them from becoming their own worst enemy.

It’s not about eliminating risk entirely. That’s impossible. It’s about making sure risk is managed in a way that removes ego from the equation, which is often the biggest hidden liability.

What Retail Traders and Investors Can Copy

Hedge funds may operate with billions, armies of analysts, and cutting-edge systems, but the principles they use to manage risk are surprisingly transferable.

You don’t need complex derivatives or a formal background in quantitative finance to apply these ideas.

What you need is discipline, structure, and the willingness to think more like a professional than a gambler.

Here are four areas where everyday investors can borrow directly from the playbook of top hedge funds.

Set Guardrails for Yourself

The most important lesson is to decide how much pain you can take before you start.

Hedge funds use strict rules around drawdowns and exposure, and retail investors should too.

Define your maximum drawdown or the largest loss you are willing to accept before you cut back risk.

For example, you might decide that if your account falls 15% from its high, you will either buy OTM put options to provide a strict boundary or reduce position sizes until you stabilize.

The key is not just to set the rule but to stick to it. That is harder than it sounds. When losses start piling up, the natural instinct is to hope things will turn around.

This is why they write their rules down in advance and treat them as non-negotiable.

Keeping a trading journal can help. Document your rules, your reasons for each trade, and how you will respond to different outcomes.

That way, when emotions run high, you have a written guide reminding you what the rational version of yourself already decided.

Think in Risk Units, Not Dollar Signs

One of the simplest yet most powerful mental shifts you can make is to stop thinking about trades in terms of absolute dollars.

This is called position sizing relative to account size, and it changes everything. If you risk one or two percent per trade, even a string of losses will not wipe you out.

You may feel frustrated, but you will still be in the game. If you size trades emotionally, based on how much you want to make, it is only a matter of time before one bad streak does permanent damage.

Consistency matters more than home runs. A fund that makes steady gains with controlled losses can compound for decades.

An individual who swings for the fences may get lucky once or twice, but eventually, the odds catch up.

If you focus on building reliable, repeatable processes and keeping risks small, the profits will take care of themselves over time.

Diversify Across Strategies, Not Just Stocks

Most retail investors think diversification means owning more stocks, but that is only a small piece of the puzzle.

Hedge funds diversify across independent strategies, not just names. You can borrow that idea, even with a modest portfolio.

Instead of putting everything into one style, combine a few approaches.

For instance, you could hold some trend-following positions that benefit when markets run strongly in one direction. Add some value investments that try to capture long-term fundamentals.

Keep a portion in defensive assets like bonds or gold that may hold up in downturns. And don’t forget cash, which gives you flexibility and the ability to add (or at least do things) when opportunities come up.

The goal is balance. Some strategies will do best in booming markets, others in choppy or even declining ones.

But by blending them, you reduce the risk that all your bets fail at once. This doesn’t require dozens of accounts or complex products.

Even a handful of well-thought-out allocations can mimic the same principle that protects multi-billion-dollar portfolios.

Another part of this is balancing short-term and long-term bets. Hedge funds know that timing is tricky, so they mix positions that may pay off quickly with those designed to compound slowly over years.

Retail investors often go all-in on one timeframe, which makes them vulnerable if that specific environment changes.

Use Simple Hedging

You don’t need exotic instruments to protect yourself.

A few simple things can go a long way. Buying index puts can act like portfolio insurance during a market crash. Setting stop-loss orders on individual positions prevents small losses from snowballing into catastrophic ones.

Holding some uncorrelated assets such as gold, Treasury bonds, or even just cash can buffer the portfolio when equities stumble.

The key is to remember that hedging is about principles, not products.

Hedge funds use swaps, structured notes, and other complex overlays because they operate at a scale that requires it. You don’t need that complexity.

You can achieve the same effect with straightforward products that are easy to understand and execute.

And keep in mind that hedges are not meant to make you money all the time. Just like insurance, you pay a cost for protection.

It might feel frustrating when a hedge drags on returns during calm markets, but when volatility spikes, you will be grateful you had it.

Case Studies / Anecdotes

It is one thing to talk about risk management in theory. It’s another to see how the biggest names in the hedge fund world actually do it.

Each of the top firms has its own style, shaped by the personalities of their founders, the lessons of past crises, and the culture they build around risk.

Let’s look at three well-known examples and what makes them stand out.

Bridgewater’s “All-Weather” Approach

Bridgewater is famous for one of the simplest yet most powerful ideas in investing: build a portfolio that can survive any environment.

Dalio realized decades ago that the future is unknowable.

Instead of trying to predict what will happen, why not prepare for every possibility and spread your risk across it so the portfolio is less biased?

This became the foundation of the All-Weather portfolio.

Bridgewater balances exposures so the fund can handle growth booms, recessions, inflation spikes, or deflationary slowdowns.

Stocks do well when growth is stronger than expectation and inflation is modest. Bonds often shine when growth slows. Commodities and inflation-linked assets protect against rising prices.

The fund is never fully exposed to one outcome when blending the mix together.

Here’s an example allocation:

- 35% stocks (equity index funds)

- 10% inflation-protected securities (e.g., TIPS)

- 10% cash/short-term bonds

- 25% nominal bonds (government and corporate bonds)

- 20% commodities (gold, silver, and other precious metals, along with standard commodities)

It’s the humility behind this approach that’s key.

Many traders and investors believe they can predict the future. Bridgewater designs beta portfolios assuming they can’t.

That mindset (preparing instead of predicting) is a subtle but powerful form of risk management.

Citadel’s Strict Drawdown Rules

Citadel is about discipline and control. Founded by Ken Griffin, Citadel runs like a machine. After barely surviving 2008, it has a relentless focus on preventing losses from spiraling.

One of Citadel’s defining features is its strict drawdown rules. Traders are given clear limits: if their strategy loses beyond a set percentage, they are forced to cut back or stop trading altogether.

There is no negotiation. There are no exceptions. Even if a trader believes passionately that the market will turn, the rule still applies.

This can feel harsh, but it is precisely what keeps the fund alive. Every trader, no matter how talented, will go through bad streaks.

Without guardrails, emotions take over, and people double down to try to win back losses. That is how blow-ups happen. Citadel’s system removes that temptation.

What makes Citadel unique is its culture of accountability. The rules apply equally to everyone, from junior traders to senior portfolio managers. It’s about process. That uniform discipline is one of the reasons Citadel has survived multiple market crashes and come out stronger each time.

AQR’s Factor Diversification

While Bridgewater focuses on macro balance and Citadel on strict discipline, AQR (founded by Cliff Asness and his colleagues) is known for a more scientific and academic-like approach.

AQR believes that returns come from exposure to certain factors, which are persistent patterns in markets.

Examples include value (cheap stocks tend to outperform expensive ones over time), momentum (assets that are going up often keep going up), and quality (companies with strong fundamentals often deliver steadier returns).

AQR’s strategy is to spread across many of these factors, in equities, bonds, commodities, and currencies, to create a broad base of uncorrelated returns.

We recently did an article covering macro momentum, which is an example strategy.

What makes AQR unique is its belief in breadth over boldness. They don’t rely on a single brilliant prediction.

Instead, they diversify across dozens of small edges. Each factor may not work all the time, but the combination smooths out the ride.

It’s the investing version of “don’t put all your eggs in one basket”; not just across assets, but across ideas.

This approach also reflects humility, but in a different way than Bridgewater’s.

Bridgewater admits it can’t know the future, and AQR admits that any single strategy will go through painful stretches.

So, AQR’s approach is to reduce the odds that everything fails at once by diversifying across factors.

The Common Thread

Bridgewater, Citadel, and AQR are very different in style.

One spreads across macro environments, another enforces iron discipline on traders, and the third diversifies across factors.

Yet they all share the same DNA: an obsession with survival and limiting losses.

Each firm has designed a system to protect against the biggest danger in investing: overconfidence.

Whether it is Bridgewater saying “we don’t know,” Citadel saying “rules first,” or AQR saying “no single idea is enough,” the theme is the same.

For individual traders/investors, the lesson isn’t to copy their exact strategies. You don’t need your own All-Weather model, Citadel-style risk committee, or AQR’s factor database.

The takeaway is that the best firms succeed not because they’re always right, but because they design systems that protect them when they’re wrong.

Conclusion

With hedge funds, their real advantage isn’t necessarily secret information and it’s definitely not perfect predictions.

It’s rigorous control of risk.

That is good news, because you can apply the same principles without billions under management.

Define your limits, size positions by risk, diversify intelligently, and protect yourself with simple hedges.

Survival comes first, profits second.

Do that consistently and you’ll discover the edge that keeps hedge funds alive can work for you too.