Global Brands vs. Offshore Entities: Understanding Your Legal Rights

The Brand Illusion: A Professional Analysis of Broker Risk

The Concept – Global Brand Recognition

In trading, brand is often mistaken for safety. A recognizable logo, glossy website and slick ad campaign signal seriousness. Retail traders see the same name on price comparison sites, football jerseys, and financial news banners and assume that this familiarity translates into protection.

From a risk point of view, that assumption is weak. Marketing is designed to make you feel comfortable, but the real truths are buried in legal documents that few traders actually read and understand before they sign up.

When a broker runs a “global” campaign across multiple regions, the natural conclusion is that “this firm is big, regulated, and therefore safe everywhere”. The imagery reinforces that feeling. High definition shots of headquarters in major cities, sponsorships of well-known sports teams and copy that emphasizes decades in business all encourage you not to ask basic questions about who exactly you would be contracting with. You remember the logo, not the small-print name of the company connected to your specific account.

This cognitive shortcut is understandable. Our brains have a lot of other things to process and most of us are not lawyers. But when it comes to brokers and trading platforms, the details that feel boring on the page are often the ones that decide how you are treated if something goes wrong.

The Reality – A Web of Different Companies

Almost every large broker name you see online is used by more than just one single company. With the brand as an umbrella, a company group will operate in the form of a cluster of different legal entities, spread across countries and regulatory regimes.

One brand may for instance have one Cypriot company authorized by the Cyprus Securities and Exchange Commission (CySEC) for its EU clients, another company authorized by the Financial Conduct Authority in the United Kingdom for its British clients, a third company authorized by the Australian Securities and Investments Commission (ASIC) for its Australian clients, and one or more companies deliberately registered in permissive jurisdictions such as the Seychelles, Vanuatu or Saint Vincent & the Grenadines to catch clients that fall outside these stricter jurisdictions.

In the example above, the company licensed by CySEC must adhere to both Cypriot law and EU-level regulation, including the framework set by the European Securities and Markets Authority (ESMA). For a brokerage company, this means things such as leverage caps for retail trading and mandatory risk warnings on leveraged products. CySEC (and the other financial authorities within the EU) restrict leverage to 30:1 on major forex pairs for retail trading and have even lower caps in place for other assets.

The United Kingdom is no longer a part of the EU, but the UK FCA has very similar rules in place when it comes to retail trader protection, and British brokerage companies must adhere to them.

On the other side of the globe, the Australian company in the example above must follow ASIC rules, including the ASIC product intervention order that capped retail CFD leverage at levels similar to ESMA and the UK FCA, and introduced tougher margin close-out rules and protection against negative balances. ASIC’s review in 2024–2025 showed that these changes sharply reduced extreme losses and margin close-outs among retail traders.

Now, let’s take a look at the companies based in jurisdictions known for their lax approach to trader protection, e.g. the Seychelles, Vanuatu, and Saint Vincent & the Grenadines. In so-called “offshore paradise locations”, both trader protection rules and general company supervision tend to be looser. We can expect to see lighter capital requirements, weaker conduct rules and very little mandatory reporting. In some cases, the offshore vehicle might not even be a licensed broker; it can simply be a standard company holding a basic business license.

To the trader, all of these different companies can show up under the same brand. From a legal perspective, they are separate companies, with stronger or looser connections depending on the exact circumstances.

The Trap

The core trap is this: a brand being well-known and popular is not a legal guarantee that every entity within its group offers the same trader protections and sticks to the same high level of conduct. From a legal perspective, exactly how poorly you can be treated without recourse depends on exactly which entity you sign up with.

If you open an account with “Brand X Global Ltd” in the Seychelles, you are not piggybacking on the regulatory framework of “Brand X UK Ltd” just because they share a logo. You are opting into the law and oversight of the Seychelles jurisdiction, even if all the marketing you have seen references the group’s strong regulatory presence in Britain.

In practice, this means that the comfort you feel when you see a famous name can be badly misaligned with the contract you are actually signing. The illusion comes from assuming that regulation attaches to the brand. In reality, it attaches to the specific entity named in your contract.

Why the Entity Name Matters

The Jurisdiction Gap

From a civil case perspective, your rights as a trader largely depend on what the contract says. Do you have a contract with an entity within your own jurisdiction, or do you have a contract with an entity abroad? And what does the contract say (if anything) about governing law?

In standard broker-client contracts, you will usually find a section that defines the parties, and a section titled “Governing Law” or “Jurisdiction”. The first tells you which legal entity you are contracting with. The second tells you which country’s law applies and where disputes must be resolved.If the agreement says that you are contracting with “ABC Markets (UK) Ltd” and that the governing law is England and Wales, you are inside a framework where the law of England and Wales, and FCA rules, apply. If it says that you are contracting with “ABC Markets International Ltd, registered in Seychelles” and that Seychelles law applies, your contract lives there instead.

That difference is not academic. It determines what conduct rules apply and where you would have to bring a civil legal action if a disagreement escalates.

Accessing Justice

Access to justice is partly about formal law, and partly about practical friction.

If you live in the United Kingdom and your broker is FCA authorized, there is a defined complaints path. You complain to the brokerage firm. If you are not satisfied, you can escalate to the Financial Ombudsman Service. The UK FCA has clear processes for handling reports of misconduct by authorized firms.

Similar clear paths exist in other countries with strong trader protection rules. In Australia, ASIC oversees Australian Financial Services licensees and has powers to take action against them, while the Australian Financial Complaints Authority handles many individual disputes. In the European Union, the respective national regulators operate similar complaint schemes.

In offshore locations known for the relaxed approach to trader protection, things work differently. If your account is with a company based in one of these jurisdictions, you are typically dealing with a regulator that has fewer resources, a smaller supervision team, and sometimes a much narrower mandate. In many cases, trader protection rules are largely absent.

There are also situations where a rule may exist, but the legal system does not really work hard to enforce it. Even when an offshore regulator has real powers, pursuing a case as a foreign retail client usually involves hiring local counsel in that jurisdiction, understanding unfamiliar procedures and dealing with distance and time zones.

Do you even speak the language used by the local legal system? Are you familiar with where they draw the line between a civil case and a criminal case, e.g. when you claim fraud (a crime), and the broker claims it is simply a civil disagreement between two contract partners? Will the local financial authority have your back, or does the full burden of preparing for the case fall on you?

For many traders with accounts in the low five-figure range, the cost of seeking justice in an offshore location outweighs the likely benefit. As a result, they do not pursue formal redress at all. The dispute ends in frustration rather than in any ruling. And the brokerage company groups that open up companies in these lax jurisdictions are very aware of this dynamic.

Investor/Trader Compensation Schemes

Compensation schemes are another area where entity matters more than brand.

Around the world, many countries have investor/trader compensation schemes that can step in and pay compensation, up to a limit, when a brokerage company does not fulfill its obligations. Typically, these programs are designed to step in when a broker becomes bankrupt after having co-mingled company funds and client funds (which is usually in itself a violation of the rules).

Without the co-mingling, the client funds can simply be paid back to each trader when the company files for bankruptcy. When co-mingling has occurred, all the money is in the same pot, and traders will have to compete with all the other claimants. This is why strict financial authorities typically require brokerage companies to keep client money and assets completely segregated from company assets.

Exactly what these investor/trader compensation schemes look like varies.

- In the UK, the Financial Services Compensation Scheme (FSCS) can pay compensation up to a limit per eligible person per firm if an FCA-authorized investment firm fails and cannot meet its obligations. The scheme is funded by levies on authorized firms, and its scope is defined by UK law. It does not cover every product or every client type, but where it applies, it is a real safety net. The FSCS can pay up to £85,000 per eligible person per firm.

- In the EU, member countries operate Investor Compensation Schemes under the Investor Compensation Schemes Directive. These protect retail clients of investment firms up to a minimum of 20,000 euros, funded similarly by contributions from authorized firms.

- In Australia, traders and investors have less protection than in the UK and EU, because there is no general FSCS-style scheme.

It is important to remember that these schemes do not follow the logo. They follow the license, and in some cases, you also need to be a resident of that country to be eligible. If your account is with the group’s UK entity, and that entity fails, you fall within FSCS coverage if you also meet the other conditions. If your account is with the same group’s offshore company in the Seychelles, the FSCS has nothing to do with you.

If you decide to contract with a brokerage company outside your own jurisdiction, picking one based in a country with an investor/broker compensation scheme is not enough to guarantee coverage. Let’s for instance look at the United Kingdom. To be eligible for compensation from the UK FSCS, you must use an FCA-licensed broker and, with a few exceptions, be a resident of the UK or one of the entities that are recognized under FSCS rules.

Non-UK residents are typically not eligible for FSCS compensation, even if they use an FCA-regulated broker. So, a Kenyan resident using an FCA-licensed broker can find themselves in a situation where they are ineligible for compensation from the UK scheme (since they are not a UK resident) and ineligible for compensation from the Kenyan scheme (because the broker does not hold a Kenyan license). The UK FSCS is primarily a UK consumer protection measure, not a universal guarantee.

A common misconception is that “Top Tier” protection follows the brand or even the license across borders. In reality, investor compensation schemes often have strict residency requirements.

- The UK Example: To be eligible for the FSCS (£85,000) protection, you generally must be a UK resident. A trader from Kenya or Malaysia using a UK-regulated broker may find themselves legally excluded from the compensation fund, even if the broker holds a valid FCA license.

- The EU Framework: Under the Investor Compensation Schemes Directive, protection (up to €20,000) is typically tied to the specific EU member state’s national scheme where the firm is authorized, but eligibility criteria for “third-country” (non-EU) residents vary significantly.

The Takeaway: Before signing up, don’t just check if the broker is “covered” by a scheme—check if you, as a resident of your specific country, are an “eligible claimant” under that scheme’s specific statutes.

The Self-Selection Funnel

The Nudge

International broker websites are usually not neutral. Instead, many of them are built to route you along specific paths, while carefully avoiding overt rule violations.

One common pattern is IP-based “jurisdiction selection”. When you visit the site, it detects your location and suggests or automatically assigns you to a particular entity. The print may be very small as you are informed that “services are provided by XYZ Markets International Ltd (Vanuatu) for clients in your region”. The default registration form or client agreement then lists that offshore entity as the operator.

The impression is that you are being matched with the “appropriate” branch of a single firm. In reality, you are being nudged into a segment of the group that may be positioned outside stricter regulators’ direct line of sight. You could, in theory, apply to open an account with the group’s UK or EU entity instead, but the site does not push you that way.

This is self-selection because you still click the buttons and confirm each step of the way. The design simply makes one choice feel easier and more natural than the others.

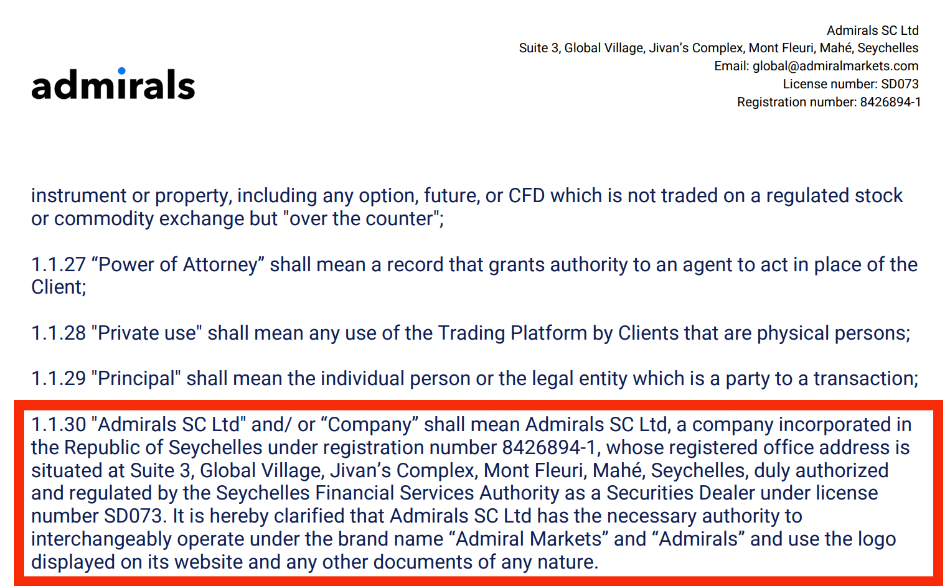

Broker legal documents sometimes spell the process out very clearly. A real example of this can be seen in Admirals’ Seychelles client agreement, which we’ve read through. Under the same Admirals brand, the agreement states that a prospective client applying for an account is first asked to complete an “Account Opening Form”, then to complete and sign the client agreement and provide KYC documents.

The same agreement defines the counterparty as Admirals SC Ltd in Seychelles, and as you can see below, it says that it may operate under the brand names “Admiral Markets” and “Admirals”, and provides that the agreement is governed by Seychelles law with disputes subject to the exclusive jurisdiction of the Seychelles courts. In other words, the familiar global brand is not the legal counterparty; the Seychelles entity is.

The Bait

- Offshore entities in lax jurisdictions often advertise much higher leverage than would be permitted under ESMA, FCA or ASIC rules. Where EU and comparable regimes cap retail forex leverage at 30:1 for major pairs, offshore units may offer 200:1, 500:1 or even 1000:1 on the same pairs. For an inexperienced trader, the choice on the website can look like a simple choice between 1:30 max leverage and 1:500 max leverage, with the different legal entities only being shown in the fine print at the bottom of the glossy pop-up selection boxes.

- Lax jurisdictions typically allow retail welcome bonus offers that would not be permitted by stricter jurisdictions. This can be very appealing, especially to inexperienced traders who are not savvy enough to check the trading requirements before accepting a bonus. Brokerage companies in lax jurisdictions are often seemingly generous with retail bonuses, rebates and competitions, but the devil is in the details, i.e. in the fine print.

- Onboarding can also be quicker and easier in laxer jurisdictions, with fewer requirements and fewer questions. Stricter KYC questions, appropriateness tests and risk warnings required under MiFID II or similar regimes can feel like unnecessary hurdles to a new trader. Offshore entities frequently take advantage of lighter rules to cut down these steps and market that aggressively.

The Hidden Cost

When you, a retail trader, are onboarded under a strict investor protection regime, there are rules about things such as maximum leverage, margin close-out thresholds, clear risk warnings and negative balance protection. These all exist because regulators have watched thousands of retail accounts blow up in predictable ways.

When you accept an offshore route, you gain freedom to use more leverage and to receive richer bonuses, at the price of losing some monitoring of how those features affect real clients. If the firm’s offshore arm fails or behaves badly, you stand outside the dispute and compensation frameworks of your home jurisdiction and of the group’s top-tier entities. In other words, you trade a bit of short-term “flexibility” for less transparency and weaker recourse.

For some sophisticated traders, that is a deliberate decision. For many retail clients, it happens without any conscious choice.

Civil Cases vs. Criminal Cases

When we talk about broker-client conflicts, we often talk about civil cases. But the risk of falling victim to criminal actions (such as fraud) is also something you should consider before you sign up with a broker based outside your jurisdiction, especially if the foreign jurisdiction is a lax offshore paradise. Putting “Seychelles law applies” in a contract does not magically erase the local criminal law of your home jurisdiction.

But when a brokerage company, and the people behind it, are hiding in a lax jurisdiction on the other side of the world, actually bringing them to justice in a criminal case and getting your money back becomes much more complicated. In many cases, it will prove impossible.

Civil Claims

Civil claims typically arise when your broker breaches your contract. For civil claims, jurisdiction is usually determined by contractual choice-of-law clauses in the account agreement. This means that when you enter into that contract, you also agree to initiate civil proceedings, if any, in the contractual choice-of-law jurisdiction. Your home courts will most likely refuse to touch the case, unless there is a strong statutory exception.

Even if your home court would take on the case and rule in your favor, enforcement of a domestic judgment against a foreign broker requires recognition of the judgment in the foreign country. Civil recovery against brokers based in lax jurisdictions is known to be complex, expensive, and uncertain.

Criminal Claims

Criminal law addresses violations such as fraud, embezzlement, or unauthorized financial activity. Criminal jurisdiction is territorial. Generally, only the country where the offense occurred, or the offender is located, can prosecute, although there are exceptions.

If you claim that your broker has committed a crime, such as fraud, you can submit a report to local law enforcement, even if the broker is based in another country and the contract stipulates a foreign jurisdiction for civil cases. Your local authorities can document the offense, and may refer the matter to the applicable foreign authorities under mutual legal assistance treaties (MLATs).

It is important to understand that without the cooperation of the foreign authorities, your local authorities cannot force the foreign broker to appear in court or return funds. For minor retail cases, authorities rarely prioritize investigation unless systemic or large-scale fraud has become a political hot potato.

The Role of the Financial Authority

If you live in a country where brokers are licensed by a strict financial authority, you can avoid a lot of legal complexity by picking a broker licensed by that authority. Typically, only a company based in that jurisdiction can be licensed by the authority. So, a broker that wants to obtain a UK FCA license must also establish a company in the UK, which makes them easier to reach.

Avoiding jurisdictional complexity can serve you well in both civil claim and criminal claim situations, and because the financial authority is there to make sure brokers it licenses actually stick to the trader protection rules. Your first port of call when a complaint can’t be resolved directly with the broker will therefore be the financial authority, and they have an established path for how to proceed. You don’t even have to know if it is a civil case or criminal case; you simply tell them everything and they will know the available routes forward.

Also, brokerage companies that are licensed have agreed to follow a long list of rules that are more detailed and leave less room for interpretation than the more general laws of the country. In countries that take trader protection seriously, licensed brokers are supervised and audited, and the financial authority has far-reaching rights to investigate the company.

How to Verify The Entity Before Signing Up

The Footer

The simplest first step is to go to the bottom of the website. Most compliant financial websites include a paragraph in the footer that reads along the lines of “This website is operated by…” or “XYZ is authorized and regulated by…”. That sentence tells you which company operates the site and which regulator, if any, oversees it.

If you see wording like “XYZ Markets Ltd is authorized and regulated by the FCA” followed by a firm reference number, you can cross-check that number on the FCA’s Financial Services Register. The register is public and allows you to confirm the exact legal name, status and permissions of the firm.

If, instead, the footer names a company in an offshore location, that is the first sign that you are not dealing with the brand’s top-tier entity.

Some groups list several entities in the footer, with different regulators and company names. That is your cue to dig deeper rather than assume all of them apply to you.

The Agreement Check

No matter what you see on the website, it will not be enough to verify the entity, because the decisive document is the Client Agreement.

Before you sign up, you should be able to open a PDF or web page with that agreement. It usually starts by defining the parties: “This agreement is between [legal name] and the client.” That [legal name] is the one that matters. If it is “XYZ Markets (Europe) Ltd, authorized and regulated by CySEC”, you are signing up with a company based in Cyprus, in the European Union. If it is “XYZ Markets Global Ltd, registered in St Vincent and the Grenadines”, you are signing up with a company based in a renowned offshore paradise country.

Later in the agreement, you will find a section on governing law and jurisdiction. It may say that the agreement is governed by the laws of a particular country and that courts in that country have exclusive or non-exclusive jurisdiction over disputes.

If that country is your own, your path in a dispute is much clearer. If it is a foreign country, you introduce jurisdictional complexity; any serious dispute likely requires foreign counsel, translation of documents and navigation of an unfamiliar judicial system. If it is a notorious offshore location with lax trader protection rules, your chances of any restitution drop even lower.

Reading this does not require legal training. You do not need to interpret every clause. You only need to identify two facts: which company name appears as your counterparty, and which law applies.

The Alleged License

Any fraudster can make up a name and claim to run a company licensed in your jurisdiction. Always go directly to the applicable financial authority website and verify the information. Make sure the exact name of the company, not just the brand, matches a licensed entity. It is also a good idea to visit the broker website listed with the financial authority, and sign up through that exact website, instead of using any links provided by ad campaigns, referrals, or similar. The goal is to avoid fraudulent clone sites.

The Leverage Litmus Test

Leverage levels can act as a quick way to spot if you are being nudged towards an offshore entity. Most of the regulators that are considered top-tier when it comes to retail trader protection have set clear caps on retail leverage. CySEC and other EU regulators limit major FX pairs to 30:1, gold and major indices to 20:1, and individual equities to 5:1 for retail clients. The FCA, after the UK’s exit from the EU, chose to adopt similar limits. ASIC’s product intervention order set the same caps for Australian retail accounts.

If you live in a jurisdiction where such caps apply but you see an offer of 1:200, 1:500 or even 1:1000 leverage for a retail account, two explanations are likely. Either you are being onboarded as a professional client under a different rule set, or your account is not under that jurisdiction at all. Both explanations are strong reasons to pause and investigate, because both paths will reduce your legal protections.

For most new traders clicking “open account” on a website, professional classification is unlikely. The more common pattern is that they are being routed to an offshore entity where those caps do not apply. Using leverage as a litmus test is not precise, but it is fast. If the leverage figures on the promotional banner or in the contract are far above what you have seen published by your home regulator, that is a strong signal that something is wrong. However, seeing the right leverage caps is no guarantee that the jurisdiction and classification are correct.

Red Flag Checklist

| Feature | Safe (Green-Tier Regulated) | Real Example | High Risk (Offshore/Lax) | Real Example |

|---|---|---|---|---|

| Legal Name | Matches the regulated entity exactly. | eToro (UK) Ltd / eToro (Europe) Ltd. | Generic or brand-led naming that hides the legal counterparty. | FXGlory user agreement states: “This Agreement is between FXGlory and the Client.” (No legal company suffix like Ltd or Corp). |

| License Number | Shows a specific license from a top-tier regulator (FCA, ASIC, CySEC). | FCA FRN 583263 (eToro UK) or CySEC licence 109/10 (eToro Europe). | Often lists a “Registration Number” which is a business ID, not a financial license. | FXGlory lists Saint Lucia registration 2023-00207, which is a company ID, not a trading license. |

| Physical Address | Lists a real office in a major financial center (London, Sydney, etc.). | 24th floor, One Canada Square, Canary Wharf, London (eToro UK). | Uses a shared “Corporate Centre” or P.O. Box in an offshore tax haven. | FXGlory: PKF Corporate Services Building, 1st floor, Meridian Place, Choc Estate, St. Lucia. |

| Verification Link | Direct link to the regulator’s official, searchable database. | FCA Register entry for ETORO (UK) LIMITED / CySEC register entry for Etoro (Europe) Ltd. | No link provided, or links only to a “Certificate of Incorporation” (which is meaningless). | FXGlory pages typically do not provide a direct link to a searchable regulatory register. |

| Leverage Warning | States strict retail leverage caps (usually 30:1). | XM’s EU site: “Up to 30:1 leverage available dependent on instrument.” | Promotes “unlimited” or extreme leverage to attract retail gamblers. | FXGlory prominently advertises leverage up to 1:3000. |

| Redirection | Clearly warns you if you are being moved to a different regional entity. | eToro shows a pop-up: “It looks like you’re in the United States. View our US site.” | Quietly switches the URL or footer based on IP to an offshore domain (e.g., .com to .sc). | HFM (formerly HotForex) often defaults to their Seychelles (.sc) or Mauritius entity for global traffic unless the user specifically seeks the UK/EU site. |

Jurisdictional Arbitrage: What It Is & Why It Happens

Jurisdictional arbitrage describes the practice of choosing where to base operations or entities based on differences in law and regulation across countries. In finance, it appears when firms structure their groups so that high-friction activity, such as dealing with strict conduct rules and product restrictions, sits in one jurisdiction, while more aggressive marketing or higher-risk products sit in another with looser requirements.

From a business view, this is rational. Complying with strict regimes raises costs. ESMA’s product intervention rules on CFDs, negative balance protection requirements and leverage caps all reduce the revenue a broker can generate per client compared to a high-leverage, lightly monitored offshore environment. ASIC’s product intervention in 2021–2026 had a similar effect in Australia.

By maintaining entities in different countries, groups can still serve clients who want features banned or restricted in top-tier jurisdictions, while keeping their flagship licenses clean. Marketing then leans heavily on the safety reputation of the flagship, and the big promotions of the offshore companies, even though getting both are not possible for retail clients.

This is not hidden. Group structure charts in annual reports, where they exist, often show dozens of subsidiaries. But retail traders rarely read those documents.

Not all use of entities in several jurisdictions is abusive. Operating several companies will, in fact, often be necessary for a multinational brand that wishes to obtain the required licenses to be active on multiple markets around the world. The UK FCA requires a company based in the UK, and so on. Each jurisdiction and financial authority has its own rules, and establishing several companies is an approved method to ensure traders in each jurisdiction are treated correctly.

From a trader’s perspective, there are also situations where signing up with a foreign brokerage company makes sense. Some experienced traders consciously choose to work with less regulated entities because they want higher leverage, looser margin rules or access to products that local regimes restrict. They are aware of the risks and are willing to assume them. After all, trading is about accepting risks and managing them carefully. The trader knows that if the entity fails or behaves unfairly, their practical options are limited. They factor that into position sizing, cash management and counterparty diversification. Typically, they sign up with several brokers, and never keep a large part of their total capital or assets with any individual broker.

The problem arises when ordinary retail clients are drawn into the same structures without understanding that they have stepped outside their home protections. For them, the risk side of the trade-off is invisible. They only see the attractive features. Jurisdictional arbitrage shifts regulatory risk from the firm to the client. The firm benefits from operating at lower compliance costs through its offshore arm, while the client accepts weaker protection without a direct price tag attached. The brand serves as a bridge, making the offshore offer feel as safe as the onshore one. Seeing that clearly does not require a PhD in finance. Once you see it, you will stop asking “is this brand well-known” and start asking “which exact company will I be dealing with, and under which rule book”?

Last but not least, it is also worth mentioning that there are traders who live in jurisdictions where trader protection rules are absent or not enforced, or where the financial authority does not license, supervise and investigate online retail brokers. For such traders, picking a broker based in a foreign country with stricter rules can be the “least-bad” choice if they want to trade online. A trader in Farawayistan might not enjoy the same full protection as a British resident when they sign up with a British FCA-licensed broker, but they do so hoping an FCA-licensed entity will behave well across the board and treat Farawayistan clients well too.

Summary: The 3-Step Verification

The entity trap works by exploiting inattention. You are nudged to care about visual identity, features and pricing, and to ignore which legal entity sits behind your account. A simple three-step habit can reduce that risk.

- First, stop and think before you sign up. Treat the moment before you sign up as a pause point. Do you know which company you are about to sign up with, where it is based, and which jurisdiction will apply? Verify the entity. Read the footer. Open the Client Agreement. Note the legal name and governing law.

- Secondly, cross-check that name on your local regulator’s website. Do not trust information published anywhere else, e.g. on the broker’s site or in advertising material. If the brand claims to be FCA authorized, you should find the exact entity in the FCA Register. If you cannot find the entity at all, or if the one you find is different from the one in your agreement, you have your answer. Brand Ltd UK is not the same as Brand Global Ltd Seychelles.

- Third, ask the uncomfortable questions. Contact support and ask them directly which specific company will hold your account and which law governs your Client Agreement. Note how clear and specific the answer is. A credible operation should be able to respond quickly and clearly. If you receive vague replies about “global operations” or are pointed back to marketing pages instead of being given a legal name, you know exactly how much weight to give the brand halo.

The global broker you see on billboards is not a single thing. It is a set of entities, governed by very different rules. Your risk lives in the one you sign with, not in the name on the shirt of a sports team.