The AI Mega-IPO Wave: Why Ordinary Investors May Lose Out

The U.S. stock market is set for a shake-up as SpaceX and Anthropic are eyeing IPOs in 2026, while OpenAI is likely to happen in 2027. If they come off, substantial amounts of capital from ordinary investors will flow into these stocks whether they like it or not, potentially leading to more over-concentration in AI firms, while making retirement holdings even more subject to the whims of notoriously volatile characters, such as Elon Musk.

Concerned, we crunched the numbers to forecast how exposed the everyday investor could be if these IPOs go as planned.

The Five Things Worth Knowing

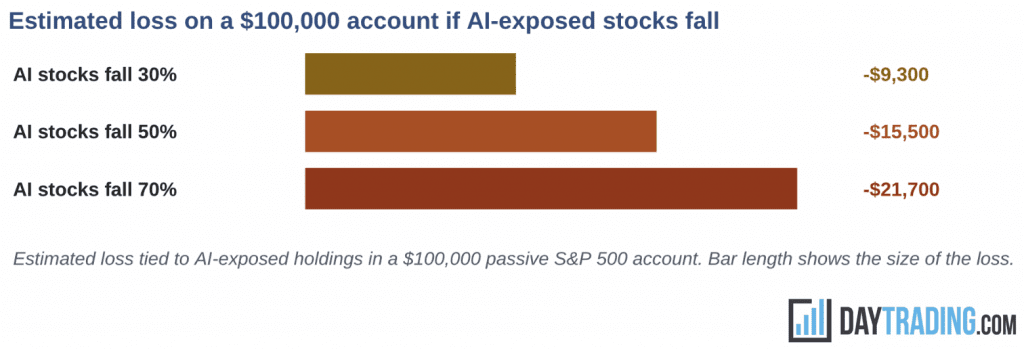

- A 50% fall in AI-linked stocks could cost a retiree with $100k in U.S indices about $15.5k.

- Everyday investors assume their index funds are diversified, protecting against single-stock and single-sector risk. But roughly 31% of the S&P 500 is now tied to the AI trade.

- An AI-led correction (likely at some point) would flow straight through index funds into ordinary retirement accounts. A saver with $500k purely in these stock funds could lose around $77.5k; a $1m account, about $155k.

- For the time being, you’re simply buying a well-marketed growth story, not a stock based on credible earnings.

- We’ve modeled three plausible scenarios for everyday investors and shown how much money they could potentially lose based on different balances.

- SpaceX is targeting a $1.75-$2T valuation despite losing roughly $5B a year before the xAI merger.

- The numbers do not support the price. SpaceX generated about $18.7 billion in revenue in 2025 and lost roughly $4.9 billion. In the first 3 months of 2026, it reported $4.7 billion in revenue and $4.3 billion in losses.

- Since its launch (no pun intended), SpaceX has amassed $37 billion in losses – more than any company going public in history.

- The AI lab is reportedly burning over $1 billion a month, pushing the combined entity even deeper into the red. Private investors can’t continue to finance this indefinitely, which essentially forces an IPO. That’s a valuation near 90x revenue (and over 100x revenue if targeting a $2 trillion IPO valuation), against a typical large-cap multiple of 3-8x.

- Our SpaceX case study explains why the finance matters more than Musk’s repeated pattern of ambitious timelines that have not materialized, from point-to-point Earth travel promised in 2017, a crewed Mars mission that was promised in April 2011 within 10 years, Mars launch schedules he claimed would start in 2018, to new claims about autonomous lunar factories and self-growing and sustaining cities.

- We also list 6 red flags in Musk’s corporate and governance setup of SpaceX that should make any prospective investor think carefully.

- Passive investors could be buying these stocks within 15 trading days of listing.

- A new rule is stripping out the usual waiting period. Nasdaq’s “fast entry” rule, effective May 2026, lets a large new listing join the Nasdaq-100 in about 15 trading days. Normally, a company has to prove itself in public markets first. That safeguard is now absent.

- The primary benefit involves access to new companies sooner; but the major downside is that highly speculative companies get mechanically pushed into passive pools of money. This worsens aggregate earnings and increases the volatility of these indexes.

- SpaceX, OpenAI, and Anthropic are all approaching IPOs despite their poor finances. Discerning public-market investors may not want to buy SpaceX at ~100x revenue with double-digit billions in annual cash burn.

- Passive pools of capital are less discerning, which is why this rule expediting inclusion is so attractive to these companies.

- A larger retail allocation could make these stocks more volatile than normal. If SpaceX, and potentially OpenAI, make as much as 30% of the offering available to retail investors, that puts more of the float in the hands of investors who tend to trade more emotionally, more frequently with more momentum-/trend-chasing styles, and with less access to company information than institutions.

- Hidden exposure to a single Musk-controlled company could climb from about $400 to $3k per $100k invested.

- Day-one exposure is modest, but it can and will ramp up.

- Index weight is set by tradable float and not by headline valuation. Accordingly, SpaceX would enter somewhere near a 0.4% S&P 500 weight, not 3%.

- But as insider lock-ups expire and more stock trades publicly, we expect that weight could climb toward 3%. That would be enough to rank SpaceX among the 10 largest companies in the index.

- The future funding needs of these potentially mega-cap companies aren’t limited to the IPOs either. The IPO is merely the start of fundraising, not the end, so public investors should fully expect their stakes to be diluted in time.

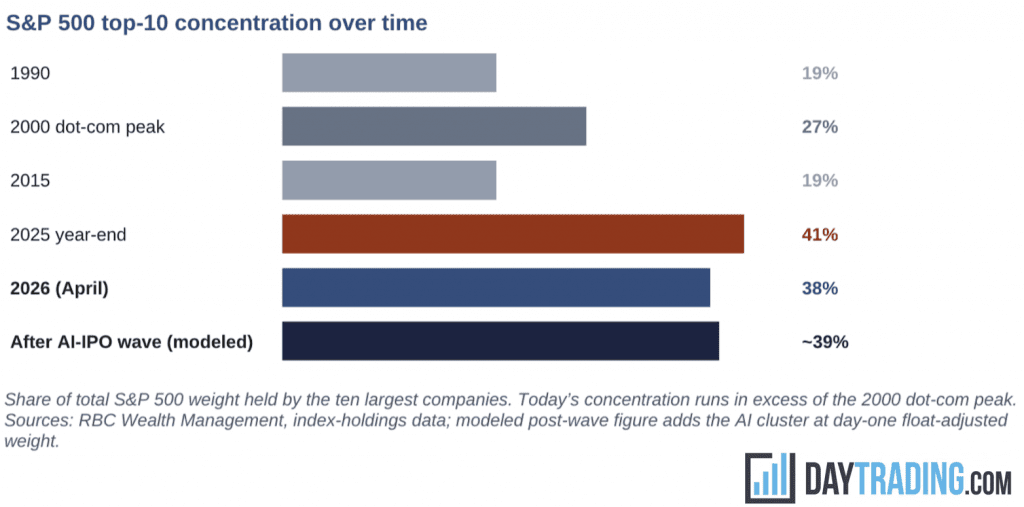

- The S&P 500 is already more concentrated than at the 2000 dot-com peak.

- We are concerned that the AI cluster is being put into an already top-heavy market. The 10 largest S&P 500 companies hold around 38% of the index. The dot-com peak was 27%.

- SpaceX, OpenAI, and Anthropic would deepen a bet that the index is already quite concentrated in. And their operating losses are going to have to be financed for many more years, and there’s no certainty that they will make profits that ever support their extremely high valuations and lead to reasonable returns on investment.

- Tesla, another Musk-controlled company, has shown that futuristic-tech narratives and long-duration promises can sustain and increase valuations, even if they’re untethered from the current and near-future reality of the business. But it’s risky, and the music may stop at some point. History has shown that transformative technologies don’t always reward the companies that build them.

How Much Passive Money Could Get Pushed In

The question for the everyday saver and investor is this: if I own a standard index fund, how much of my money will end up in these companies without my actively choosing them?

Most coverage skips one technical point – that index weight isn’t always the same as headline valuation. Index weight is usually based on some version of float-adjusted market capitalization. This is the value of shares actually available for public trading.

SpaceX, for example, could try to list at a $1.75 trillion valuation while selling only a small percentage of the company to public investors (less than 5%). Accordingly, if the public float is limited at listing, the day-one index weight would be much smaller than the headline valuation implies. Restricting the float also helps the IPO become more successful and supports its performance in the public markets, because it takes less demand to hold the valuation up.

The table below uses a simplified float-adjusted framework to estimate potential index exposure under illustrative IPO scenarios.

Table 1. Estimated day-one index weight and passive buying under illustrative listing scenarios

| Company / IPO terms | Float-adj. cap | Est. S&P 500 wt | Est. Nasdaq-100 wt* | Est. S&P-linked buying | Est. NDX-linked buying |

|---|---|---|---|---|---|

| SpaceX: $1.75T val / $75B float | $225B | 0.40% | 0.64% | $52B | $4.2B |

| OpenAI: $1.0T val / $50B float | $150B | 0.27% | 0.43% | $35B | $2.8B |

| Anthropic: $500B val / $30B float | $90B | 0.16% | 0.26% | $21B | $1.7B |

| AI cluster combined (all three listed) | $465B | 0.82% | 1.31% | $107B | $8.5B |

(*S&P 500 figures are simplified exposure estimates, using float-adjusted market capitalization against an assumed aggregate S&P 500 market size. Actual S&P 500 inclusion isn’t automatic and would depend on S&P methodology and committee decisions.

**Nasdaq-100 figures use a simplified application of Nasdaq-style float-adjusted weighting assumptions. Actual treatment would depend on final eligibility, float, liquidity, and index methodology at the time of listing.)

The day-one number is smaller than most framing implies. Under this model, the three companies together would represent less than 1% of the S&P 500 at listing. That’s still material, but not enough by itself to remake the index overnight. The larger risk shows up over time, as they take up greater weight and the public float ramps up.

Why The Exposure Can Grow After Listing

With most IPOs, early investors, employees, venture and private equity funds, or insiders are subject to lock-ups. This helps the IPO’s success by constricting supply and preventing a wave of informed selling right after listing. Despite the role of public disclosures, insiders know far more about the company’s real finances, growth quality, growth prospects, and internal risks than ordinary public investors.

Standard IPO lock-ups typically run 90 to 180 days. After this period, insider and early-investor shares can start entering public circulation. As more shares become tradable, the float-adjusted market cap can rise, even if the company’s total valuation doesn’t change.

That is where passive exposure can quietly increase.

Table 2. Illustrative SpaceX S&P 500 exposure as tradable float grows

| Tradable float | Est. S&P 500 weight | Est. S&P-linked buying | Per $100k S&P 500 account |

|---|---|---|---|

| ~4% at listing | 0.40% | $52B | $402 |

| 10% float | 0.93% | $121B | $929 |

| 20% or more float | 3.03% | $394B | $3,030 |

(Assumptions: $1.75T company valuation, approximately $56T aggregate S&P 500 market capitalization, and simplified float-adjusted index exposure. Per-account figures assume the account is fully invested in an S&P 500 index fund. A typical retirement account that holds bonds or other assets would show proportionally smaller figures. These figures hold valuation and index size constant. Actual index weight would depend on market prices, index methodology, eligibility, float treatment, and admission.)

A move from a 0.4% to a 3% index weight would increase the passive retirement money tied to a single company from a few hundred dollars to roughly $3,000 per $100,000 invested. That gets increasingly to the point where single-stock risk becomes a real concern.

What’s important to know here is that index exposure can grow materially after listing without any ordinary saver placing a trade, or even being aware of where exactly their money is being allocated.

A Top-Heavy Index Gets Increasingly Top-Heavy

The S&P 500’s largest companies already take up a historically high share of the index, and are thematically similar to boot. Several of those names are AI-linked through chips, cloud computing, data centers, software, advertising infrastructure, or direct investments in AI companies.

While SpaceX, OpenAI, and Anthropic would continue to skew the indices in a certain direction, the broader issue is the cumulative, broadening weight of the AI trade inside passive portfolios. This is similar to what the “new economy” stocks represented in the late 1990s and early 2000s, though the dot-com concentration sat on a more profitless base on aggregate than what we have now.

Investors often think of an S&P 500 fund as giving them broad diversification across 500 companies, and protecting them from single-stock and single-sector risk. Technically it does. But economically, a small group of these mega-cap companies, operating overlapping business models (and similar financial exposures), now drives a much larger share of the index’s return.

Table 3. Index drag if the top-10 stocks fall

| Decline in top-10 stocks | Index drag today | Index drag after modeled AI cluster |

|---|---|---|

| Down 20% | -7.6 percentage points | -7.8 percentage points |

| Down 40% | -15.2 percentage points | -15.5 percentage points |

| Down 60% | -22.8 percentage points | -23.4 percentage points |

(This uses a 38% top-10 weight as the midpoint of recent reported concentration estimates. The modeled AI IPO cluster adds less than one percentage point at day-one float-adjusted weights. The concern for retirement accounts and passive investors isn’t the immediate increment alone, but adding to the level of concentration it sits on top of.)

The IPOs in the pipeline don’t transform concentration by themselves. Rather, they go into an already top-heavy index that overlaps significantly on the same theme. A 40% fall in the ten largest stocks would, by itself, drag the whole index down about 15 percentage points, all else equal. That’s before considering second-order and downstream effects, investor reactions to such an event, related AI suppliers, data-center companies, and broader tech names.

A Larger Retail Allocation Could Increase Volatility

SpaceX, and possibly OpenAI, could also allocate as much as 30% of the IPO to retail investors. If true, that could make these stocks more volatile after listing, as retail investors (taken categorically) trade more heavily around headlines, recent trends or momentum in the share price, social media sentiment, and personality-driven factors.

A larger retail allocation doesn’t necessarily imply that institutional demand will fall short. A company may purposely want a broader shareholder base or the branding and public relations effect of letting smaller rank-and-file investors participate. But it does nonetheless raise the question of why a company would want to place so much of the offering into retail hands if institutions are chomping at the bit to get in at the proposed valuation?

There’s also been hints at woes for OpenAI at least, as when Softbank tried to borrow $6 billion against their OpenAI stake that was supposedly worth $100 billion, the banks denied the loans. Question marks are hovering over its valuation.

Three Scenarios For A $100k Retirement Account

We’ve modeled three outcomes for the AI-exposed part of the S&P 500 and translated each into the dollar effect on a $100,000 passive account that many everyday investors may hold.

“AI-exposed” includes the largest tech and infrastructure companies whose valuations are materially tied to AI expectations. This includes companies in semiconductors, cloud computing, platform software, digital advertising, and the modeled AI IPO cluster.

The estimate uses a roughly 31% AI-exposed share of the S&P 500. A narrower definition, such as excluding AI suppliers, or a broader one, such as including companies materially using AI to streamline operations, would reduce or increase the result, respectively.

Table 4. Modeled outcomes for a $100,000 passive S&P 500 account

| Scenario | What happens | Est. index effect | Est. effect on $100k |

|---|---|---|---|

| Boom | AI-exposed stocks rise 25% | +7.7% | +$7,700 |

| Volatility case | AI-exposed stocks swing sharply, with a 15% peak-to-trough drawdown | -4.6% at drawdown | -$4,600 |

| Correction case | AI-exposed stocks fall 50% | -15.4% | -$15,400 |

(Illustrative only. The volatility-case figure is the estimated drawdown point, not necessarily the year-end result. The correction case is a sensitivity estimate, not a forecast.)

The purpose here is to show how much of an ordinary portfolio is now tied to the AI sector. Through passive funds, savers can become highly exposed to the same theme even if they never buy a single AI stock directly.

A typical $100,000 passive S&P 500 account could carry roughly $800 of AI mega-IPO exposure at listing, rising toward $3,000 or higher as lock-ups expire, without the saver choosing any of it.

What A Fall Could Cost Different Savers

Scenario analysis can be applied to any account balance. In the table below, we show the estimated loss tied to AI-exposed holdings alone if those stocks fall by 30%, 50%, or 70%, across a range of retirement account sizes. It answers a direct question: if the AI trade gets too far in front of its skis and unwinds, what would it potentially cost me?

Table 5. Estimated retirement-account loss if AI-exposed stocks fall

| Account balance | AI stocks fall 30% | AI stocks fall 50% | AI stocks fall 70% |

|---|---|---|---|

| $25,000 | -$2,325 | -$3,875 | -$5,425 |

| $100,000 | -$9,300 | -$15,500 | -$21,700 |

| $250,000 | -$23,250 | -$38,750 | -$54,250 |

| $500,000 | -$46,500 | -$77,500 | -$108,500 |

| $1,000,000 | -$93,000 | -$155,000 | -$217,000 |

(Estimated loss attributable to the AI-exposed share of an S&P 500 index fund (modeled at 31% of the index), assuming the account is fully invested in that fund. A 30%, 50%, or 70% fall in AI-exposed stocks maps to an index decline of roughly 9.3%, 15.5%, and 21.7% respectively. Illustrative sensitivity estimates, not forecasts.)

The figures scale directly with balance. It’s not that any one of these declines will necessarily happen, but that the exposure is already there, sitting inside portfolios that savers were told were broadly diversified.

Meme-Stock Dynamics Meet Index Investing

This IPO wave deserves special attention because the companies leading it carry valuations well in excess of what their current finances would support. The price rests on a steep discounted future growth trajectory and on trust that the business model will work itself out over time. When stocks like that become standard index holdings, the speculative dynamics of a “meme stock” get wired directly into ordinary retirement portfolios.

Start With The Valuations

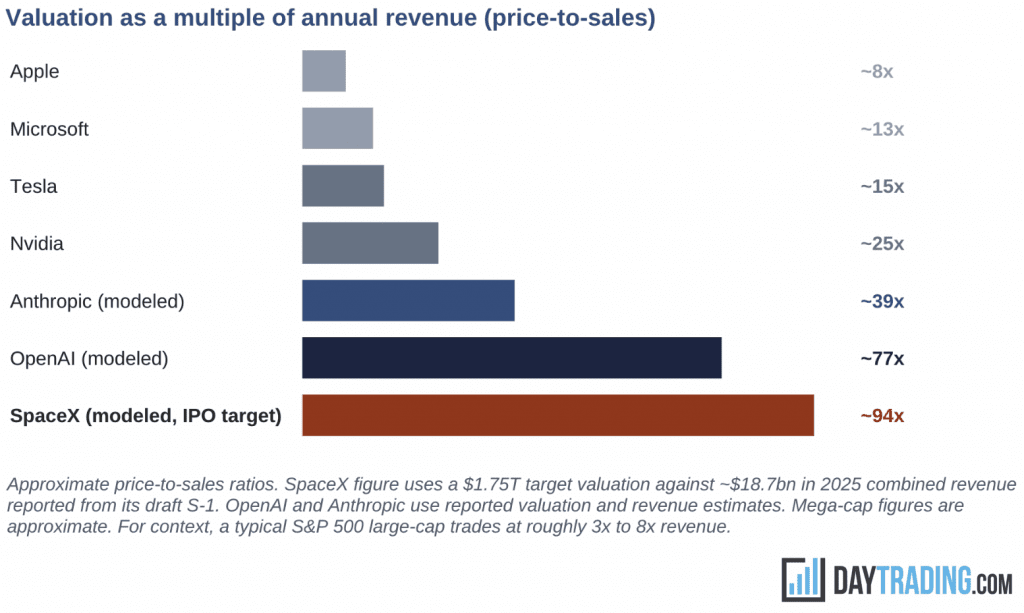

A useful measure for fast-growing companies is the price-to-sales ratio (i.e., price-to-revenue ratio), which compares a company’s market value to its annual revenue. Established large-cap technology companies generally trade at single-digit revenue multiples. As they mature, they trade more on earnings and operating cash flow, because that is what ultimately justifies a valuation.

This matters especially for retirees and those nearing retirement, who rely on investments that produce earnings rather than speculative growth stories where those earnings are far less certain.

The AI mega-IPO candidates need to grow a great deal and also prove that the business model works.

The mismatch is that broad index funds are marketed as conservative, diversified ownership of hundreds of different companies, while these holdings are more in character with late-stage venture capital bets that are unprofitable, require massive cash infusions for some time to plug their operating losses, and are being stacked on top of an already dominant investment theme in the indices.

A Transformative Technology Isn’t Always Economic To Produce

Automobiles and air travel were two of the biggest technological achievements of the last century. Over 90% of automobile manufacturers of the past 100 to 125 years have gone bankrupt, and modern auto manufacturers run on thin margins. Airlines have cumulatively returned close to zero profit to shareholders over their ~100-year history.

Most of the benefits of these technologies accrued to other industries, not to the producers. Whether AI rewards its builders the same way is, at this point, far from settled.

One old rule of thumb on valuation: take a company’s market cap, divide by 10, and ask whether it can conceivably earn that much in profit within five years. A trillion-dollar IPO implies $100 billion in profit, not revenue, within five years. At $2 trillion, it implies $200 billion. SpaceX isn’t currently doing even a tenth of that figure in revenue, and the total addressable market (TAM) of its launch and satellite business is uncertain.

The filing claims a staggering $28.5 trillion TAM (larger than the entire US GDP), with 93% of that market tied directly to AI.

These companies’ cash flows are discounted so far into the future that an investor essentially has to believe in what they might become over decades and that the extreme growth story will make the investment worthwhile.

The SpaceX Case Shows Why The Finances Matter

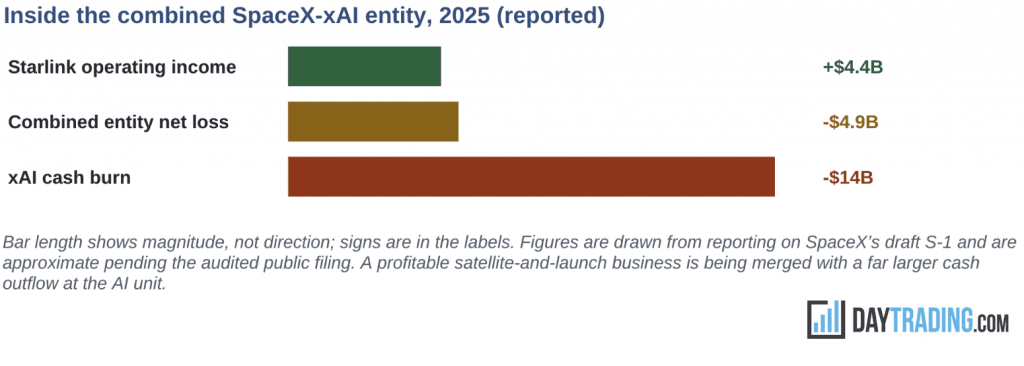

In February 2026, SpaceX completed an all-stock merger with xAI. According to reporting on the company’s draft IPO filing, the entity generated about $18.7 billion in revenue in 2025 and posted a net loss of roughly $4.9 billion. That loss is set to deepen with xAI, which is reported to have burned around $14 billion in cash during the year, more than $1 billion a month, against roughly $3.2 billion in revenue. 2026 Q1 showed a net loss of $4.3 billion.

The health of Starlink’s business is also not represented well by SpaceX’s accounting because they’re capitalizing launch and manufacturing costs, so it ends up as capital expenditures (investment shown on the balance sheet) and not operating expenses on the income statement. Depreciation is also a very real cost, but that’s not accounted for in reported (and promoted) EBITDA metrics.

SpaceX is being used as the wrapper that carries a large, loss-making AI operation into the public markets. Taking xAI public on its own wasn’t feasible, and private fundraising can’t support it forever. In the ongoing AI resource grab, private investors’ pockets are simply not deep enough. Investors who buy the combined company, directly or through an index fund, are buying both parts at once.

Ahead of the IPO, SpaceX took on a $20 billion bridge loan to help refinance some of its debt. This means a large portion of the expected money raised from public investors will go immediately to paying off Wall Street banks. Moreover, footnote analysis shows that while the IPO aims to raise up to $75 billion, SpaceX actually needs $235 billion over the next few years to cover its future commitments.

SpaceX has accumulated $37 billion in losses since its inception, more than any company going public in history.

An already unprofitable rocket-and-satellite business is being used as the wrapper to carry a roughly $14-billion-a-year AI cash burn into the public markets, and a fast-tracked goal of being forced into index funds.

The Tesla Comparison Helps Explain The Dynamic

Tesla’s automotive revenue fell during 2025, yet the stock continued to trade at an extreme multiple of reported profit and a very high multiple of revenue, far above any traditional carmaker. Tesla has been public for more than 15 years and reached a valuation above $1.5 trillion despite never really resolving its finances. The way it earns almost all of its revenue (selling cars) will never get it to that figure.

A large part of that valuation depends not on low-margin car sales today but on long-dated promises about robotaxis, humanoid robots, and artificial intelligence – all speculative, capital-intensive, and carrying material regulatory hurdles. Those promises contribute next to nothing in current revenue, but they sustain a narrative that keeps the valuation elevated. The association with Musk, and a continuous stream of future-facing announcements, has helped the company avoid the fall in valuation its current financials might otherwise invite.

SpaceX is being offered to public investors on a similar basis, and on shakier near-term financials once xAI is included. How much can the launch and satellite businesses grow, when the IPO implies roughly a 100 times revenue multiple and valuations eventually have to be sustained on earnings and operating cash flow? Musk himself has said the AI unit needed rebuilding from the ground up after the merger; it was not generally considered a frontier lab beforehand. The original 11 AI co-founders of xAI have since quit the company.

The combined valuation depends on a future in which orbital data centers (or similar moonshot projects) and frontier AI pay off. That can be a legitimate bet for a venture investor. But a venture capitalist generally expects that most of their investments will be zeroed and they aren’t making these bets at $2 trillion, or close to, valuations. It’s a very different proposition when the same bet becomes a standard holding in retirement accounts through index inclusion, where this kind of speculation is generally discouraged in favor of more stable, cash-generating companies.

6 Red Flags – Governance, Disclosures, and Related-Party Transactions

#1 – Super-Voting Power

Using a dual-class share structure, regular investors get Class A shares (1 vote), while Musk gets Class B shares (10 votes). This grants Musk 85% voting control despite owning only 41% of the equity, making it effectively impossible for shareholders to fire him.

Having tight control and compromised boards has been Musk’s governance approach with every project since being let go by the original X.com in September 2000. On top of that, the terms explicitly force investors to waive their rights to class-action lawsuits or public courts. This mandates private, individual arbitration for any future disputes or fraud allegations.

#2 – The Texas Guardrail

Following legal battles in Delaware over his executive pay, Musk reincorporated SpaceX in Texas, where corporate law is uniquely favorable to management. In Texas, a shareholder must own a staggering $52 billion in stock (3%) just to file a derivative lawsuit, and text messages/emails are explicitly shielded from shareholder discovery requests.

#3 – “Consciousness” as a Metric

The prospectus formally lists management’s primary objective as “extending the light of consciousness to the stars.” This phrase appears 10 times in the official filing.

#4 – Bailing Out Tesla and Insiders

The filing shows that SpaceX single-handedly propped up Tesla’s struggling vehicle sales by purchasing $131 million worth of Cybertrucks at full retail price, accounting for 18% of all US Cybertruck registrations at one point in late 2025. Also, SpaceX carries over $20 billion in AI leasing obligations structured with entities tied to sitting board member Antonio Gracias.

#5 – Improbable Executive Compensation

Musk’s new pay package includes 1 billion restricted shares that vest if SpaceX reaches a $7.5 trillion market cap and establishes a permanent Mars colony. SpaceX explicitly tells the SEC these goals are “improbable” – an accounting loophole to avoid recording hundreds of billions in expenses today. Still, Musk receives the legal rights to vote those shares, collect dividends, and borrow tax-free cash against them immediately.

#6 – Starship is SpaceX’s Critical Dependency

Starship underlies every future revenue stream – e.g., orbital data centers, Mars colonies, Starling V3 deployments. Starship would need to achieve a flight rate of hundreds of launches per year.

Yet Starship has yet to reach orbit or land without combusting. As such, the IPO valuation depends on a piece of hardware that’s yet to be proven.

A History of Overpromising and Underdelivering

Musk has made many unfulfilled promises across his companies, claiming many soon-to-be tech breakthroughs that never come, and show very little to no progress.

For example, point-to-point Earth travel was promised starting in 2017. The claim was that flying passengers from New York to Shanghai via rocket would happen “within a decade” for a few thousand dollars per passenger.

In 2016, Musk promised steady, train-like cadences of rockets leaving for Mars every couple of years (starting in 2018). Over the last decade, none of those scheduled Mars missions have launched.

And because the Mars timeline has stalled, the rhetoric has shifted to building an autonomous, self-growing city and an electromagnetic mass-driver satellite factory on the Moon using Tesla “Optimus” robots.

What Ties This IPO Wave Together?

A central reason these companies are heading public now is that the AI arms race has outgrown what private investors and government funds can capably finance. Building and running large AI models requires enormous and continuous capital infusions for compute, chips, and power.

Private funding rounds have been large, but are reaching a ceiling and need new sources of funding. Public markets, and the passive capital that flows in automatically through index funds, are the next and largest pool of money available.

The IPO wave isn’t simply a milestone for these companies. It is, in part, existential – a response to an acute funding need that private markets can no longer meet alone.

Secondary offerings and dilution for IPO investors should also be fully expected.

Bottom Line

This AI IPO wave goes beyond a few private companies going public. It’s fundamentally a story about how quickly speculative, founder-driven, high-valuation companies can become unavoidable holdings inside ordinary retirement accounts.

The day-one index exposure may be modest. A trillion-dollar or two-trillion-dollar IPO doesn’t automatically mean a commensurate index weight off the bat.

But the longer-term issue is that if and when the AI mega-IPO wave arrives, and if these companies enter major indices, passive savers and investors could gain exposure automatically. As floats expand, that exposure could grow. And because the market is already concentrated in AI-linked mega-caps, the new listings would deepen an existing structural bet, while mixing in new companies with much shakier finances.

The result is that millions of everyday investors may believe they’re holding broad, passive, diversified portfolios while in reality becoming increasingly exposed to one investment theme, one technology cycle, and a small number of speculative companies that lack the current finances to back up their valuations.

Methodology Notes

- Market-size assumptions – S&P 500 aggregate market capitalization is modeled at approximately $56T and the Nasdaq-100 at approximately $35T. These are rounded estimates for scenario modeling purposes.

- Index inclusion – Nasdaq-100 fast-entry rules may allow qualifying large new listings to enter faster than under the prior annual-only reconstitution process. S&P 500 inclusion isn’t automatic and depends on separate eligibility criteria and committee discretion. This note models potential exposure if the companies qualify.

- Index weight – Exposure is modeled using simplified float-adjusted market capitalization. The Nasdaq-100 and S&P 500 use different methodologies. The tables show approximate exposure mechanics and not exact index-provider calculations.

- Float assumptions – The modeled scenarios assume SpaceX sells $75B of public float at a $1.75T valuation, OpenAI $50B at $1T, and Anthropic $30B at $500B. These are not confirmed listing terms. All 3 are expected to list at these approximate amounts or higher, with Anthropic potentially even seeking an OpenAI type of valuation with its enterprise adoption. Per-account figures assume an account fully invested in an S&P 500 index fund. Portfolios containing bonds, cash, and other investment allocations would need to appropriately downweight the effect proportionally.

- Concentration assumptions – Top-10 index concentration is modeled at 38%. This is the midpoint of recently reported estimates in the mid-to-high 30s% and low 40s%. The stress table isolates the top-10 impact only. It doesn’t model second-order impacts, like wider market contagion.

- AI-exposed basket – The scenario analysis and the loss table use an estimated 31% AI-exposed share of the S&P 500, covering mega-cap technology and infrastructure companies whose valuations are materially linked to AI expectations, plus the modeled AI IPO cluster. The definition is subjective. The output is meant to be treated as a sensitivity analysis.

- Valuation multiples – Price-to-sales figures in Chart C use reported or estimated valuations using 2025 revenue. The SpaceX figure uses a $1.75T target against ~$18.7B in revenue reported from the draft S-1. Mega-cap figures are approximate.

- Company financials – SpaceX, xAI, and Starlink figures are drawn from media reporting on the draft S-1 and pre-IPO disclosures. They are approximate pending the audited public filing. Tesla figures reflect 2025 reported results.

- Important caveat – All figures are illustrative estimates built to be transparent and reproducible. They’re not forecasts, investment advice/recommendations, or intended to be claims about what index providers will do. A change in market-size, passive-asset, or valuation inputs would move estimated weights and dollar effects proportionally.

Article Sources

- Nasdaq Indexes, “Nasdaq-100 Index Methodology Changes FAQ,” May 2026.

- Nasdaq Indexes, “Nasdaq-100 Index Methodology,” May 2026.

- Reuters, “New Nasdaq rules to include ‘fast entry’ for new listings on benchmark index,” March 30, 2026.

- S&P Dow Jones Indices, “S&P Dow Jones Indices Announces Update to S&P Composite 1500 Market Cap Guidelines,” July 1, 2025.

- Morningstar, “The SpaceX IPO: How Index Funds Will Adapt,” April 8, 2026.

- The Wall Street Journal, “S&P Eyes Plan to Ease Index Rules With SpaceX IPO Looming,” May 1, 2026.

- Barron’s, “EchoStar Rallies as Play on SpaceX IPO. There Could Be More Upside,” May 18, 2026.

- Reuters, “OpenAI lays groundwork for juggernaut IPO at up to $1 trillion valuation,” October 30, 2025.

- Reuters, “OpenAI defeats Elon Musk’s lawsuit, removes obstacle to IPO,” May 18, 2026.

- Anthropic / Reuters, “Anthropic clinches $380 billion valuation after $30 billion funding round,” February 12, 2026.

- RBC Wealth Management, “The ‘Great Narrowing’: S&P 500 concentration,” January 22, 2026.

- TIAA, “Q2 2026 CIO Chartbook,” April 2026.

- Vanderbilt Policy Accelerator, Asad Ramzanali, “After the AI Crash,” March 2026.

The writing and editorial team at DayTrading.com use credible sources to support their work. These include government agencies, white papers, research institutes, and engagement with industry professionals. Content is written free from bias and is fact-checked where appropriate. Learn more about why you can trust DayTrading.com