The Index Fund Trap: Why Your “Safe” Index Fund Is Now A High-Stakes AI Bet

For years, the sales pitch for index funds was simple and mostly fair. Buy the market, keep costs low, avoid stock picking, get a high degree of diversification from day one, and let time do the hard work. That idea still has merit. What has changed is the thing being bought.

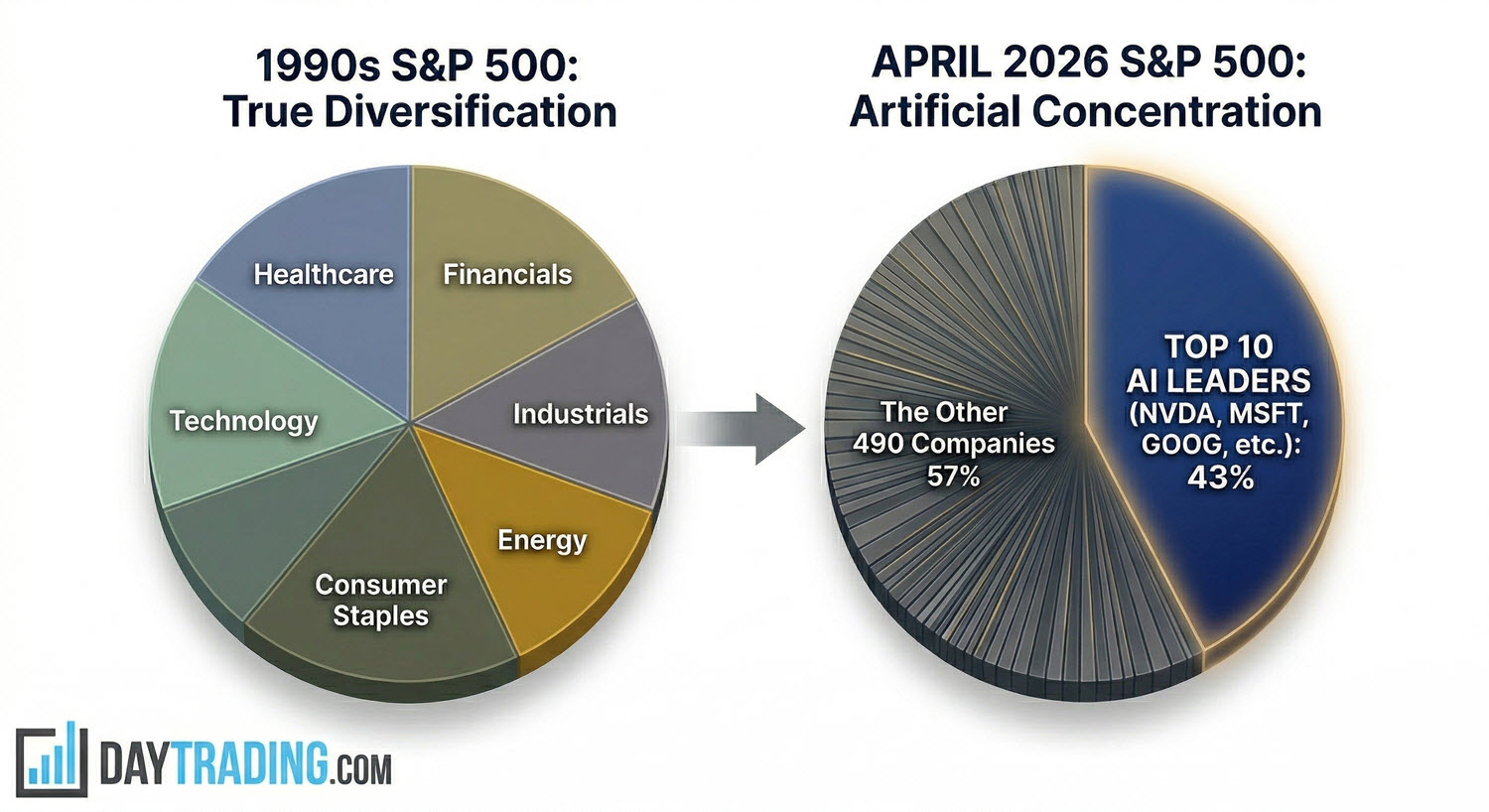

A broad U.S. equity index in the 1990s looked broad in the ordinary meaning of the word. Retail, banks, healthcare, industrials, consumer staples, telecoms, oil, utilities, and technology all had visible weight. A buyer of the index was making a bet on U.S. business activity as a whole, not on a single story about one industry’s next 10 years. But that is not the structure investors face in April 2026. If we look at the S&P 500 index, the top 10 companies now account for more than 43% of the index by market value, according to data sourced directly from S&P Dow Jones Indices. That is above the dotcom-era peak and far above the level that most retail investors picture when they hear the phrase “broad market exposure”.

This high concentration matters more than we might think at first glance, because the dominant names are not just large, they are also linked by the same macro driver: artificial intelligence (AI) spending. The index is not just dominated by a few big corporations; it is dominated by a specific, and highly speculative, sector.

A closer look at the S&P 500 index reveals how Nvidia, with its chips and systems, sits at the center. Microsoft, Alphabet, Amazon, and Meta fund the capex cycle through data centers, cloud platforms and model deployment. Broadcom, Apple, and other mega caps are tied in through infrastructure, devices, networking, or distribution. This is not sector diversification in the old sense. It is one capital cycle showing up under several tickers.

Valuation adds another problem. Depending on the measure used, the S&P 500 is trading around 28 times earnings, well above long-run norms. And that premium is not spread evenly across the index. A large part of it sits in the AI leaders and the companies investors believe will control the next computing stack.

The conclusion is uncomfortable but dangerous to deny. Passive indexing in 2026 is no longer a low drama default. It is a concentrated exposure to the AI trade, sold by funds that still claim to offer a high degree of diversification.

The 2026 IPO Boulder: OpenAI, SpaceX, and Anthropic

So, what will happen next to the broad market index funds? It is possible that the next phase of this trend towards increased concentration won’t come from the existing giants alone, but also from corporations that are still outside the public market, waiting near the door with a very large valuation and a line of passive money behind it.

- As of April 2026, SpaceX is reportedly preparing an IPO at a valuation above $2 trillion after its tie-up with xAI, in what would dwarf every prior listing. Bloomberg reported that the combined company had previously been valued at around $1.25 trillion but that the target for the public listing now exceeds $2 trillion.

- OpenAI has not yet gone public, but it has closed a fresh funding round at an $852 billion post-money valuation and is openly discussed as a 2026 IPO candidate. The company itself announced the new round. Reuters and other outlets have also reported that management is preparing for a possible listing later this year.

- Anthropic is smaller, but not small in any ordinary sense. Reuters reported in February that a new funding round valued the company at $380 billion. It too is discussed as a possible candidate for public markets in the current cycle.

Taken together, these three companies represent a wave of private market value that is large enough to change public benchmarks. Even before formal index inclusion, they affect the market through sentiment, peer multiples, supplier revenues, and capital allocation. Once public, the effect can become mechanical, as index funds must invest in line with their own market cap rules.

That is the passive trap. Index funds do not ask whether a company is attractively priced. They buy because the rules say buy. If a new giant enters a major benchmark and meets the inclusion criteria, trillions of dollars in passive and quasi-passive strategies must own it. The demand is price-insensitive by design. That has always been true, but the scale is different when the incoming company is measured in hundreds of billions or trillions.

The risk is not hard to see. These are not mature cash machines arriving after a decade of clean public reporting. They are high-growth, high-spending companies operating in a capital-intensive race where durable economics are still being argued about. The Wall Street Journal reported that OpenAI and Anthropic are still facing extraordinary compute costs and large projected losses under full cost accounting, even as revenue rises sharply.

There is another detail that makes the issue more immediate. Nasdaq has approved new fast entry rules, effective May 1, 2026, allowing newly listed large companies to join the Nasdaq 100 much faster than before if they rank high enough by market capitalization. Reuters reported that qualifying companies can be assessed on the seventh trading day and admitted by roughly the fifteenth trading day. That shortens the gap between IPO hype and forced passive ownership.

For a beginner, this is where the old language becomes misleading. Buying a broad market index fund used to mean buying the established market and letting new stories prove themselves over time. In 2026, a buyer can end up having a lot of their capital automatically put into freshly listed AI companies almost immediately, and at a valuation set by private rounds, scarcity, and momentum rather than a full public market cycle.

That does not make these broad market index funds bad. It just makes them unsuitable for the way many retail investors still think about passive exposure. When the future arrives in the index at a trillion dollar price tag, the index stops acting like a buffer and starts acting like an amplifier.

The Nvidia Problem: A House Of AI Cards

No company shows the shift more clearly than Nvidia.

Nvidia’s market value crossed $4 trillion in 2025. By early April 2026, it was above $4.3 trillion according to several market trackers, remaining the largest listed company in the world. Reuters documented the $4 trillion milestone last year, and current market data still places Nvidia at the top of the table.

This is not a complaint about the business. Nvidia has one of the best businesses on the planet. It dominates the high-end AI accelerator market, owns critical software layers, and benefits from the simple fact that nearly every serious model builder still needs more compute than it can get. The problem is not quality. The problem is what the market has already priced in.

A company can be excellent and still be dangerous inside an index if the index depends on it too much. In many indices, Nvidia is no longer just a stock in the benchmark, it is one of the benchmark’s load-bearing walls. The same is true, to a lesser extent, for Microsoft, Alphabet, Amazon, and Meta. But Nvidia is different even from these giants, because it sits one layer lower, where the entire AI buildout begins. If model demand slows, if enterprise adoption disappoints, if returns on data center spending look weaker than expected, or if hyperscaler capex gets squeezed by financing costs or energy prices, Nvidia is the first name investors will use to reprice the whole chain.

Notably, that chain is already under pressure. Reuters reported that big tech AI infrastructure spending could reach roughly $635 billion to $650 billion in 2026, but that rising energy costs, construction inflation, higher yields, and geopolitical stress are starting to test the economics. Another Reuters piece noted that hyperscalers are using an unusually large share of operating cash flow for capital expenditures and leaning more heavily on debt markets as the spending race intensifies.

That matters because Nvidia’s valuation rests on the assumption that the spending cycle is not a spike but a long runway. If Microsoft, Meta, Amazon, or Alphabet begin slowing orders, the stock does not need a collapse in earnings to correct hard. It only needs a lower multiple on still excellent earnings. That is what highly concentrated, highly loved market leaders do. They do not wait for disaster. They reprice when the slope of perfection becomes slightly less perfect.

The recent trading action fits that description better than the old “safe anchor” label. Nvidia has already shown sharp swings in 2026, including fast double-digit moves as investors reassessed AI demand, valuations and geopolitical risks. Reuters noted that concern about AI spending and war related market stress pushed Nvidia’s valuation multiple down materially this year, despite still strong growth expectations.

For the Nasdaq 100, this is not a side issue. Nvidia is the largest component there as well, and weight data from Nasdaq and market-based composition trackers show just how much one stock can now matter to a supposedly diversified tech benchmark. This is the structural point many passive investors miss as they put their money into index funds. A broad index can become fragile not because the underlying companies are weak, but because too much of the index is exposed to the same earnings driver, the same funding cycle, the same policy risk, and the same narrative.

That is where the phrase “house of cards” starts to make sense. If one or two major cards begin to wobble, we will soon find out how much the rest is connected.

Historical Context: The Nifty Fifty Parallel

There is a useful historical parallel here. In the late 1960s and early 1970s, investors crowded into the so-called Nifty Fifty, a group of large, dominant companies treated as “one decision” stocks. The idea was simple: buy them and never sell. Names such as IBM, Xerox, Kodak, Coca-Cola, and Polaroid were seen as so dependable that valuation stopped mattering, or so people said at the time. When inflation, interest rates, and the broader macro backdrop turned, many of these stocks did not fail as businesses.

What failed was the price investors had been willing to pay for certainty and growth. Their multiples compressed hard, and years of mediocre returns followed, even when the companies themselves remained respectable. The phrase “good company, bad stock” exists for a reason.

That is the cleaner way to think about Nvidia and, to a lesser extent, Microsoft in 2026. The danger is not bankruptcy. The danger is that they remain very good businesses while the market stops paying an AI premium for every dollar of future earnings. When that happens, the stock can fall a long way without any dramatic collapse in the underlying company. That is what beginners often miss. They hear “great company” and assume “safe investment.” History is less polite than that.

Robust Earnings Versus Pure Plays: Alphabet And The AI Startups

Not all AI exposure is equal, and 2026 has made that distinction more important.

There is a real difference between companies that are AI-enhanced and companies that are AI-dependent. Alphabet is a useful example of the first group. In its most recent reported quarter, Alphabet said Google Services revenue rose 14% year over year, with Search and Other up 17%. Google Cloud revenue jumped 48% and the company’s cloud backlog reached roughly $240 billion. Those are not hopes. Those are operating numbers from a business with several mature cash engines.

That does not make Alphabet cheap, and it does not remove competitive pressure. But it does give investors something passive vehicles used to have more of: earnings backstops. If generative AI monetization takes longer than expected, Alphabet still has search, YouTube, enterprise cloud contracts, subscriptions, and a balance sheet that can absorb a bad year without requiring belief as a substitute for cash flow.

Now compare that with the pure plays. OpenAI and Anthropic have revenue growth, real products, and serious demand. They also have no legacy operating base that can carry the valuation if the frontier model business gets repriced. Their value is largely a statement about future dominance, future margins, future platform control, and future pricing power.

The distinction sounds obvious when stated plainly and when each company is analyzed individually. It becomes less obvious once those names enter a benchmark. The wrapper changes the psychology, and retail investors buying an S&P 500 linked product often believe they are buying “the economy” or “large U.S. businesses”. In reality, they may be buying a package where a very large slice of the value depends on whether a small number of AI firms can turn hope and projections into durable profits before capital markets lose patience.

It would be wrong, however, to believe that this is an issue pertaining only to late-stage startups. In reality, it spills back into the incumbents. Microsoft and Amazon are mature companies, but their cloud economics are tied to AI demand. Meta is raising annual capital expenditures up to roughly $115 billion to $135 billion for its super-intelligence push, according to Reuters.

Alphabet, Amazon and Microsoft are all spending on the same arms race. The AI-dependent companies may be pure plays. The mature companies are not pure plays, but they are still funding the same buildout. That is why the old retail distinction between “safe mega cap index” and “risky growth stock” has become fuzzy. Indices such as the S&P 500 now contain both, but more importantly, it blends them into one trade.

Why Index Funds Are No Longer Beginner Friendly

The phrase “beginner friendly” used to mean something like this: low fees, broad diversification, no need to forecast individual businesses, and a smoother ride than stock picking. When we take a look at 2026, the fee advantage still exists, but the smooth ride does not, at least not in the way people remember it.

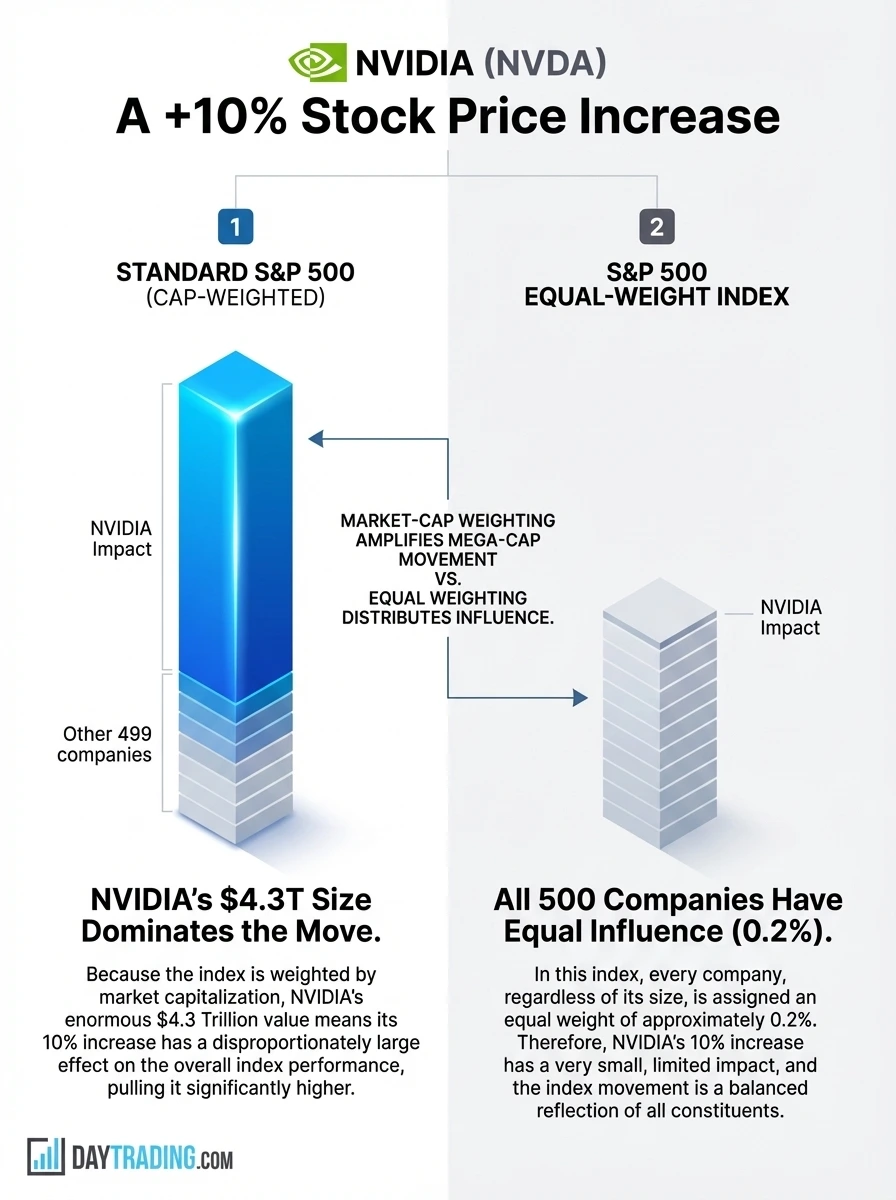

When the top of the index is this concentrated, daily moves in a few names start to control the tone of the entire product. A sharp drop in Nvidia, Microsoft, Alphabet, Amazon, Meta, or Apple can now pull the broad market lower, even if much of the remaining index is flat or positive. That is what market cap weighting does under extreme conditions.

The diversification problem is worse than the simple sector labels suggest. On paper, investors can still say they own technology, communication services, consumer discretionary, industrials, and more. In practice, much of the top weight is exposed to the same AI capex and compute cycle. Nvidia sells chips and systems. Microsoft rents cloud and deploys models. Alphabet does the same while defending search. Amazon supplies cloud and infrastructure. Meta is a buyer of compute and a seller of AI-driven ad inventory. Broadcom supplies connectivity and custom silicon. Different categories, same weather.

That reduces the usefulness of the index as a risk control tool. An old-style diversified benchmark could absorb stress in one sector because another sector worked differently. Energy could fall while banks rallied. Retail could weaken while healthcare held up. In 2026, the dominant slice of the benchmark often responds to the same rates, the same power constraints, the same chip politics, the same AI spending assumptions and the same investor mood.

Macro conditions sharpen that risk. In March 2026, Reuters reported that energy cost inflation and the Middle East conflict are testing the economics of data center expansion. The same reporting flagged the possibility that strained returns on AI infrastructure could spill into a broader equity correction. At the same time, semiconductor supply chains remain exposed to geopolitics and industrial bottlenecks. That is not the backdrop most beginners imagine when they are told to buy the market and go to sleep.

There is also a behavioural issue. Indexing was beginner-friendly partly because it reduced the urge to react. But concentrated indexes can produce single stock style volatility while still wearing the calm language of passive investing. That mismatch is a problem. People who think they own something defensive are more likely to panic when it behaves like an aggressive growth portfolio.

The Ballast Is No Longer Reliable

In earlier cycles, the broad market had a kind of internal ballast. When growth stocks cracked, bonds often held up better. When technology sold off, utilities, consumer staples, and other defensive sectors could at least slow the damage. That relationship mattered because the sectors were driven by different forces.

In 2026, that separation has weakened. AI is no longer just a software theme or a chip theme. It is also a power, grid, construction, and physical infrastructure theme. U.S. power demand is projected to reach fresh highs in 2026 and 2027, with a large share of the increase tied to data centers and large-scale computing loads. Utilities are raising capital spending to serve that demand, while energy producers and infrastructure operators are being pulled into direct partnerships with data center developers and hyperscalers. Reuters has reported on AI driven electricity demand pushing utilities to expand spending, and on data center growth lifting the strategic importance of power supply across the market.

All this changes what “sector diversification” actually means. Owning utilities, energy, industrials, cloud, and semiconductors may look diversified on a fact sheet, but in practice, those exposures are increasingly tied to the same capex cycle. If AI spending slows, the damage does not stay inside software and chips. It can hit the utilities that were counting on data center load growth, the energy names tied to incremental power demand, and the industrial suppliers building out the physical system underneath it all.

The old defensive ballast is weaker because more of the market now feeds the same AI buildout. Beginners may think they own separate sectors, while actually just being exposed to several different limbs of the same AI body.

The Global Fund Is Often The Same Bet In A Different Wrapper

A lot of beginners try to solve the concentration problem by moving one step up the shelf and buying a “world” fund instead of a U.S. fund. On paper, that sounds sensible. In practice, the fix is weaker than most people think. In March 2026, the MSCI World Index was still about 71.3% U.S. stocks, according to MSCI’s own factsheet. That means a fund marketed as world exposure is still mostly a bet on the U.S. market, and the U.S. market is still dominated by the same mega cap names driving the AI trade.

The concentration inside the wrapper does not disappear just because the label says world. One current MSCI World ETF composition page shows the top 10 holdings making up about 25% of the fund, led by Nvidia, Apple, Microsoft, Amazon, Alphabet, Broadcom and Meta. Those are not random global exposures. They are the same companies already carrying the U.S. benchmarks discussed in this article. The international portion is real, but for many beginners, it functions more like a 25% seasoning on top of the same core trade rather than a genuine break from it.

“Global diversification” sounds like protection from the U.S. tech cycle, but a market-cap-weighted world index still sends most of the money into the country with the biggest stocks, and that country’s biggest stocks are the AI leaders. Beginners may think they have stepped away from the concentration risk by clicking on a world fund instead of an S&P 500 fund. In reality, they may just be buying the same AI exposure with a thinner international accent. In 2026, true diversification takes more than buying the most popular index product with the broadest-sounding name. It takes active selection of what kind of index you actually want to own.

The Case For Active Passive Investing In 2026 And Onward

The solution is not to abandon indexing. It is to stop pretending all index exposure sold as “broad market index fund” is the same. The default passive products still work as low-cost market access tools, but they do not work as the old beginner story promised. They are no longer a neutral middle. They are frequently a strong view on AI, mega cap duration, hyperscaler spending, and the market’s willingness to keep paying a premium for all of it.

In 2026, buying the index is still passive in method, but it is no longer passive in economic exposure. The S&P 500 is now historically concentrated, richly valued by long run standards, and dominated by companies tied directly or indirectly to the same AI buildout. The next wave of giant IPOs could intensify that structure rather than soften it. Also, we need to be aware of the faster rules for index admission in the Nasdaq 100.

The sensible response is not stock picking bravado, but more deliberate index selection. That is the real shift. The old beginner move was to buy the cap-weighted index and assume you had stepped away from the need to make active judgments. In 2026, even that decision is an active judgment. If you simply pour everything into the S&P 500 and step back, you have decided to own a market where more than two-fifths of the benchmark sits in 10 names, where one chipmaker can shake the whole tape, and where future IPOs may push even more unproven AI valuation into the passive core.

- Equal-weighted products are one answer and they deserve more attention than they usually get. The S&P 500 Equal Weight Index holds the same companies as the cap-weighted S&P 500, but each name is reset to about 0.2% at quarterly rebalance. This dramatically reduces dependence on the very largest stocks.

- Total market funds can also help a bit, but less than many investors assume. Vanguard’s VTI spreads money beyond the S&P 500 into mid and small caps, which is useful. Still, the largest names remain the largest names there too. Recent holdings data show that VTI’s top positions are still led by Nvidia, Apple, Microsoft, Amazon, Alphabet, and other mega caps. A total market fund dilutes concentration modestly, but it may not be enough for investors looking for lower risk and high diversification. The top 10 still command roughly 30%+ in the VTI diluted concentration.

- Global equity exposure can also be a part of the strategy, as a mix of U.S. and non-U.S. equity can help bring diversification up, if done correctly to avoid the pitfalls.

In conclusion, the safe index fund still exists as a product label. But as a risk profile, that label looks old. If you are not prepared for a hard tech-led correction, you are not prepared for what a standard cap-weighted index fund now is.

Appendix 1

Understanding What Weighting Is And Why It Matters So Much In This Context

For beginner investors who are familiar with the concept of a weighted index, the arguments above are probably fairly straightforward. For beginners who have not paid much attention to weighting until now, seeing the situation clearly will be more difficult. I will therefore now take some time to explain the weighting concept. If you are already well-versed, you can simply skip forward to the next part of this article.

What Is A Weighted Stock Index?

A weighted index is a stock market index in which each constituent’s impact on the index level depends on a certain factor, e.g. market capitalization, price, or some other metric. Weighting determines how much influence each stock has on the overall index performance. The idea is to create a meaningful aggregate measure of market performance.

There are several different types of weighting methods and they are suitable for different investment goals.

Examples:

- Price-weighted: Favors high-priced stocks.

- Market-cap weighted: Reflects company size, and large caps will dominate the index.

- Equal-weighted: Large-cap and high-priced stocks are not given more than their due mathematical influence.

- Fundamental-weighted: Highlights companies with strong underlying metrics, e.g., earnings.

In the 1800s, the early stock indices used price-weighting for simplicity. One example is the Dow Jones Industrial Average (DIJA), which was introduced in 1896. This method would continue to dominate during the first half of the 1900s, and the first widely recognized market-cap weighted index was not introduced until 1957, with the launch of the Standard & Poor’s 500 (S&P 500).

A problem with price-weighted indices is that high-priced stocks will dominate regardless of company size. The S&P 500 offered a way to remedy this by focusing on market cap. Market-cap weighting was introduced to better reflect the actual economic significance of companies in the market, as larger companies tend to have more influence on the overall economy and investment performance. Equal-weighted and fundamental-weighted indices did not begin to appear until late in the 1900s, when they were launched to address biases in market-cap weighting, such as overexposure to overvalued or particularly large companies.

Understanding Different Methods

The Price-Weighted Index

Definition: Each stock is weighted based on its stock price.

The index is the sum of all current stock prices divided by the divisor. The divisor is a number adjusted for stock splits, dividends, or changes in the index composition so that the index remains consistent over time. Initially, the divisor could be thought of as the number of stocks, but over time, the divisor is adjusted to account for events like stock splits, spin-offs, replacements, and other corporate actions that could distort the index. The purpose of the divisor is to keep the index continuous and comparable over time, despite changes in stock count or prices due to corporate actions.

The downside of a price-weighted index is that high-priced stocks dominate regardless of company size, and if a share becomes really high-priced, that stock can have a huge impact on the overall index.

One example of a well-known price-weighted index is the Dow Jones Industrial Average (DJIA).

The Market Capitalization-Weighted Index

Definition: Stocks are weighted by their total market value (share price × number of shares outstanding).

You calculate the index by first finding each stock’s market cap. Then, add all market caps to get the total. Divide each stock’s market cap by the total to get its weight. Multiply weight by stock price (or use a scaling factor) and sum to get the index level.

A market capitalization-weighted index automatically adjusts with market movements, since the market capitalization is the same even after a stock-split or similar corporate action.

A downside is how large-cap companies will dominate the index. And overexposure to overvalued stocks is a major risk factor for market capitalization-weighted indices.

Examples of well-known price-weighted indices are the S&P500 and the NASDAQ-100.

The Equal-Weighted Index

Definition: All constituents have the same weight, regardless of price or market cap.

Calculation example: Let’s assume the index is comprised of the five stocks A, B, C, D, and E. Equal weight means 20% each. Let´s also assume that the stock prices are now 50, 100, 200, 25, 10, respectively.

- A → 50 * 0.2 = 10

- B → 100 * 0.2 = 20

- C → 200 * 0.2 = 40

- D → 25 * 0.2 = 5

- E → 10 * 0.2 = 2

Because stock prices change daily, the weights can gradually drift away from being equal. To maintain equal weighting, the index must be rebalanced periodically. It is typically not done every day. Before you invest, make sure you know how frequently the index is rebalanced, e.g. quarterly.

The equal-weighted index seeks to avoid the concentration in large-cap companies that we see in market-cap weighted indices such as the S&P 500. One of the downsides is the need for re-balancing.

Examples of well-known equal-weighted indices are the S&P 500 Equal Weight Index (an equal-weighted version of the S&P 500, giving each of the 500 companies the same influence), the Russell 1000 Equal Weight Index (equal weights across the largest 1000 U.S. stocks in the Russell 1000), and the NASDAQ-100 Equal Weight Index (equal weighting applied to the 100 largest non-financial NASDAQ companies).

The Fundamentally-Weighted Index

Definition: Weights based on fundamental measures like revenue, earnings, dividends, or book value.

The aim is to focus on underlying economic factors. But calculations can become complex and it can be difficult for investors to understand exactly how the index is calculated. Access to reliable accounting data is necessary.

Examples of fundamentally-weighted indices:

| Index | Weighting basis | Objective |

|---|---|---|

| FTSE RAFI 1000 | Sales, cash flow, dividends, book value | Focus on economic size rather than market price |

| RAFI US 1000 | Sales, cash flow, dividends, book value | Reduce overweighting of overvalued companies |

| WisdomTree Dividend Index | Dividends paid | Reward high dividend-paying companies |

| STOXX Fundamental Indices | Earnings, book value, dividends | Focus on solid fundamentals in European stocks |