The UK FSCS Double Banking Trap

- Understanding The Basics Of The FSCS

- Aggregation Risk When A Bank Fails

- Which Bank or Banks Are Holding My Segregated Client Money?

- Several Banking Brands Can Operate Under The Same Banking License

- How To Check If More Than One Bank Operates Under The Same Banking License

- Why Should I Care About Bank Aggregation Risk?

- CASS Rules Aimed At Reducing Bank Aggregation Risk

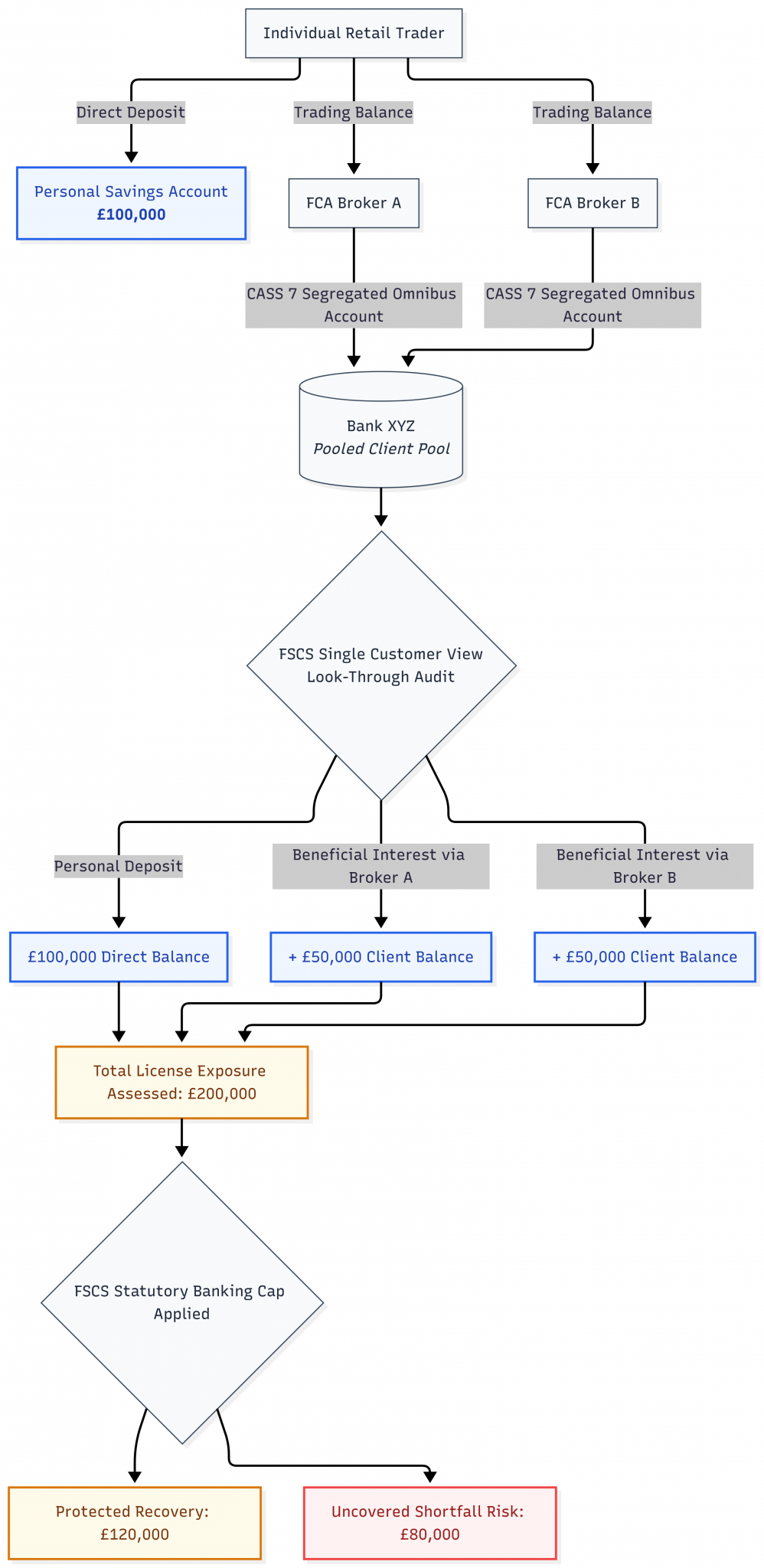

In the UK, many retail investors know that a trading account with an FCA-licensed broker is protected by the Financial Services Compensation Scheme (FSCS) up to £85,000 per eligible account, per firm. Therefore, they feel safe as long as they do not keep more than £85,000 with any individual brokerage company. In reality, and as I explained to some of our UK-based team here at DayTrading.com recently, they also need to know in which bank or banks the broker is using for the segregated client money accounts, because that becomes relevant if the bank itself fails. Bank failure is not common in the UK, but it does happen.

Money from accounts you have with different brokers, and your own individuals personal savings, can ultimately sit within the same underlying bank. In case of a banking failure, the FSCS protection applies at the banking license level, meaning exposure across personal accounts and pooled broker accounts can be aggregated.

The good news is that the FSCS ceiling is higher when a bank collapses. Instead of the £85,000 that pertains to broker accounts, the bank ceiling is £120,000. The bad news is that this is per banking license, so you might hit that ceiling even if you have made sure not to keep more than £85,000 in any trading or investment account, and not more than £120,000 with your bank.

Example: An individual has £100,000 in their savings account at Bank XYZ, £50,000 in a trading account with Broker A, and £50,000 in a trading account with Broker B. The bank has a UK banking license, and both brokers are licensed by the FCA. The individual feels safe because the bank balance is below the £120k limit, and each trading account balance is kept well below the £85k limit. However, Broker A and Broker B are also using Bank XYZ for the segregated client money accounts. When Bank XYZ fails, and there is a significant shortfall, the individual has a total claim of £200,000. What happens now?

For traders, this creates a less obvious form of concentration risk: diversification across brokers does not necessarily mean diversification across banking licenses. The effectiveness of FSCS protection depends not just on how funds are split between brokers and bank brands, but on where those funds ultimately sit in the banking network when a bank fails.

In other words, understanding FSCS protection is not just about knowing the £85,000 limit and the £120,00 limit, it is also about understanding how trading balances, personal savings, and underlying bank exposures can interact in practice. Diversification across brokers does not necessarily reduce systemic banking exposure.

Understanding The Basics Of The FSCS

Before we look deeper into the FSCS bank aggregation risk, we will take a quick look at what the FSCS is and when this scheme becomes relevant.

In the UK, the Financial Services Compensation Scheme (FSCS) protects eligible customers when authorized financial firms fail. The FSCS plays a vital role in the stability of the UK financial sector by giving people confidence in financial services.

The FSCS is the UK’s statutory compensation scheme for customers of authorized financial services firms, and it provides protection when a regulated firm is unable, or likely to be unable, to meet customer claims against it. The scheme covers a wide range of financial services, including bank and building society deposits, investment and trading accounts, pensions, insurance products, mortgage advice and arranging, debt management services, and funeral plans. Coverage depends on the type of financial product or service involved, and whether the firm is authorized by the Financial Conduct Authority (FCA) or the Prudential Regulation Authority (PRA).

Traders typically think about FSCS coverage in the context of a broker becoming insolvent and failing to honor its obligations. But we will focus on the scenario of a UK-authorized bank becoming insolvent and failing to honor its obligations. When that happens, it is the £120,000 ceiling per customer, per banking license that kicks in, and not the £85,000 per customer, per firm that is applicable in case of broker failure.

Aggregation Risk When A Bank Fails

When a bank fails, the FSCS protects up to £120,000 in total across all accounts you hold, either in your name or where you are listed as the beneficial owner (e.g. money held on your behalf in a client account) within the bank/banking group. It is the banking license that is relevant here, not the brand name of the bank. This means that if you have money in accounts with two different banking brands, they will still count together in the eyes of the FSCS if both brands are operated under the same banking license.

Let’s assume the following scenario:

- Bank XYZ fails.

- You have £100,000 in your own savings account at Bank XYZ.

- Broker A holds £50,000 of your client money at Bank XYZ.

- Broker B holds £50,000 of your client money at Bank XYZ.

- The brokers correctly identify you as the beneficial owner of those client-money balances.

- The client money at the bank is completely lost and therefore needs FSCS protection.

FSCS looks through client accounts to the underlying beneficial owner, and protection is calculated across accounts in your own name and money held on your behalf in client accounts, within the same banking group.

So your exposure is:

£100k in savings account (personal deposit)

£50k beneficial interest via Broker A client account

£50k beneficial interest via Broker B client account

Total exposure at Bank XYZ: £200k

The FSCS protection is limited to £120,000 per client, per banking license. (Assuming no temporary high balance protection).

The result is that only £120,000 of your claim is covered, and £80,000 of your claim is not covered.

In their free deposit takers course, designed for bank, building society, and credit union staff, the FSCS specifically says this when discussing client/pooled accounts: “If any of the beneficiaries have their own account within the same bank/banking group, that may affect the amount they are eligible for, as they are only protected up to £120,000 in total.”

The same wording also appears on the public-facing page: Deposit protection Q&As – banks & building societies.

Which Bank or Banks Are Holding My Segregated Client Money?

If you’re trying to assess the FSCS risk, you need to find out which bank or banks your broker is using for your segregated client money, and whether your beneficial interest in the client-money account would be identifiable for FSCS deposit protection purposes.

Many FCA-licensed brokers disclose their client-money banks in their client agreement, CASS disclosures, and/or annual reports. Some disclose them publicly, others only provide the information on request. Contact customer support and ask them to provide information about where your funds are held if the broker does not publicly disclose this data. Unfortunately, not all brokers will provide this – we know having contacted many to ask.

Several Banking Brands Can Operate Under The Same Banking License

When you assess your total exposure, it is important to take into account that more than one banking brand can operate under the same banking license.

HSBC UK Bank plc provides a simple example of how FSCS protection works at the banking license level. On their site, the FSCS specifically mentions that HSBC also uses the names First Direct, First Direct Bank, FD, and FD Bank, and that all these brands share a banking license.

If we move on to First Direct’s FSCS information page, it states that eligible deposits with HSBC UK Bank plc are protected up to £120,000 in total and that this limit applies across HSBC UK, HSBC Private Bank, First Direct, M&S Bank, and M&S Savings and Investments. Deposits held across these brands are therefore aggregated for FSCS deposit-protection purposes. That aligns with the information provided at the HSBC FSCS information page and the M&S Bank FSCS information page.

The Prudential Regulation Authority (PRA) requires banks and other deposit-takers to maintain a Single Customer View (SCV) so that, in the event of failure, eligible depositors can be quickly identified and FSCS compensation can be calculated. The aim of the SCV framework is to ensure that deposits held across different accounts and brands within the same authorised institution are correctly attributed to the same individual or entity for compensation purposes. SCV, therefore, enables all eligible deposits held by the same depositor at the same authorised bank to be identified so they can be aggregated for FSCS calculation purposes under the FSCS rules.

For more information, see the PRA Rulebook: Depositor Protection – Single Customer View requirements.

How To Check If More Than One Bank Operates Under The Same Banking License

The FSCS Checker

The FSCS maintains a dedicated banking license checker that shows which brands share the same authorized institution for deposit protection purposes.

You can search for a bank or brand name and see the authorized institution behind it. This is usually the quickest way to determine whether two brands share the same FSCS protection limit.

The FCA Financial Services Register

The FSCS banking license checker is the most practical tool for identifying whether different banking brands share the same banking license and, therefore, whether deposits may be aggregated for FSCS protection purposes. The FCA Financial Services Register can be used as a supplementary source to obtain further information about a firm’s legal name, Firm Reference Number (FRN), trading names, and regulatory permissions, etcetera.

The Financial Services Register

What Is The FSCS Temporary High Balance Protection?

A temporary high balance is a higher-than-usual amount of money in your account caused by a qualifying life event. In most cases, FSCS can protect this balance up to £1.4 million for six months, and protection starts when the money becomes yours legally or is paid into your account.

Note: If the temporary high balance is because of a personal injury, disability, or incapacity award, it is treated differently and may qualify for unlimited protection.

Does The Money Have To Stay In My bank Account To Have Temporary High Balance Protection?

FSCS guidance states that temporary high balance protection can continue after the money is moved, provided the qualifying conditions are still met. The general FSCS rules also recognizes beneficial ownership in certain client and pooled accounts.

However, the FSCS has not published any information specifically covering FCA broker client-money accounts. In other words, they have not specifically confirmed that temporary high balance protection continues when qualifying funds are transferred into an FCA broker’s segregated client-money account.

Moving a temporary high balance (or parts of it) from your bank account and into a broker account, therefore, comes with a degree of uncertainty. Complicating the situation is the fact that the FSCS specifically states that it can not confirm protection until a firm fails and evidence is reviewed.

What Is A Qualifying Life Event?

Your balance may qualify as a temporary high balance if it results from one of the following qualifying life events:

- Sale of your main home

- Property purchase or equity release

- Inheritance

- Insurance payouts

- Retirement benefits

- Redundancy

- Divorce or civil partnership dissolution

- Compensation claims (including unfair dismissal or wrongful conviction)

- Personal injury compensation

- Disability or incapacity benefits

Why Should I Care About Bank Aggregation Risk?

Bank aggregation risk is important to understand because it can expose your money to counterparty risk even if you use one or more reputable brokers that are licensed by the FCA and adhere to all applicable laws and regulations. This is a risk that becomes apparent when a bank fails, not when a broker becomes insolvent.

You may think you have two separate exposures:

- Personal savings with Bank Alpha

- Trading cash held by Broker XYZ

But if Broker XYZ holds its client money pool at Bank Alpha, you have both direct and beneficial exposure to the same failed bank.

UK deposit protection applies to the eligible depositor’s total protected balance with the authorized banking firm. If several bank brands share the same banking license, the cap applies across brands. So, you might already have an aggregation risk situation going on, even though you are keeping your cash split over two different bank brands. Now, add the fact that your broker is also putting your trading account money into a bank that operates under the same banking license.

The risk is that your personal bank and your broker’s client money bank are the same authorized institution, and the statutory compensation cap does not care that you mentally separate those balances.

This is especially frustrating because neither the trader, nor the broker, has done anything bad. The trader picked an FCA-licensed broker and a UK bank. The broker segregated the client funds according to all the rules and put them in a UK bank. No one acted recklessly. The problem was concentration.

CASS Rules Aimed At Reducing Bank Aggregation Risk

The Financial Conduct Authority (FCA) recognizes that concentration risk arises when client money is held within a framework that necessarily involves the use of a limited number of eligible credit institutions. Under FCA’s Client Assets Sourcebook (CASS), brokers must segregate client funds from their own money by holding them in designated client bank accounts at eligible credit institutions.

CASS imposes governance, and due diligence obligations on broker firms when selecting and maintaining credit institutions used to hold client money. Firms are required to exercise due skill, care and diligence in the selection, appointment, and ongoing review of these institutions as part of their client money protection arrangements. Within this framework, firms must also have appropriate systems and controls in place to manage the risk of holding client money with credit institutions, which in practice includes consideration of concentration risk and, where appropriate, the distribution of client money across more than one institution.

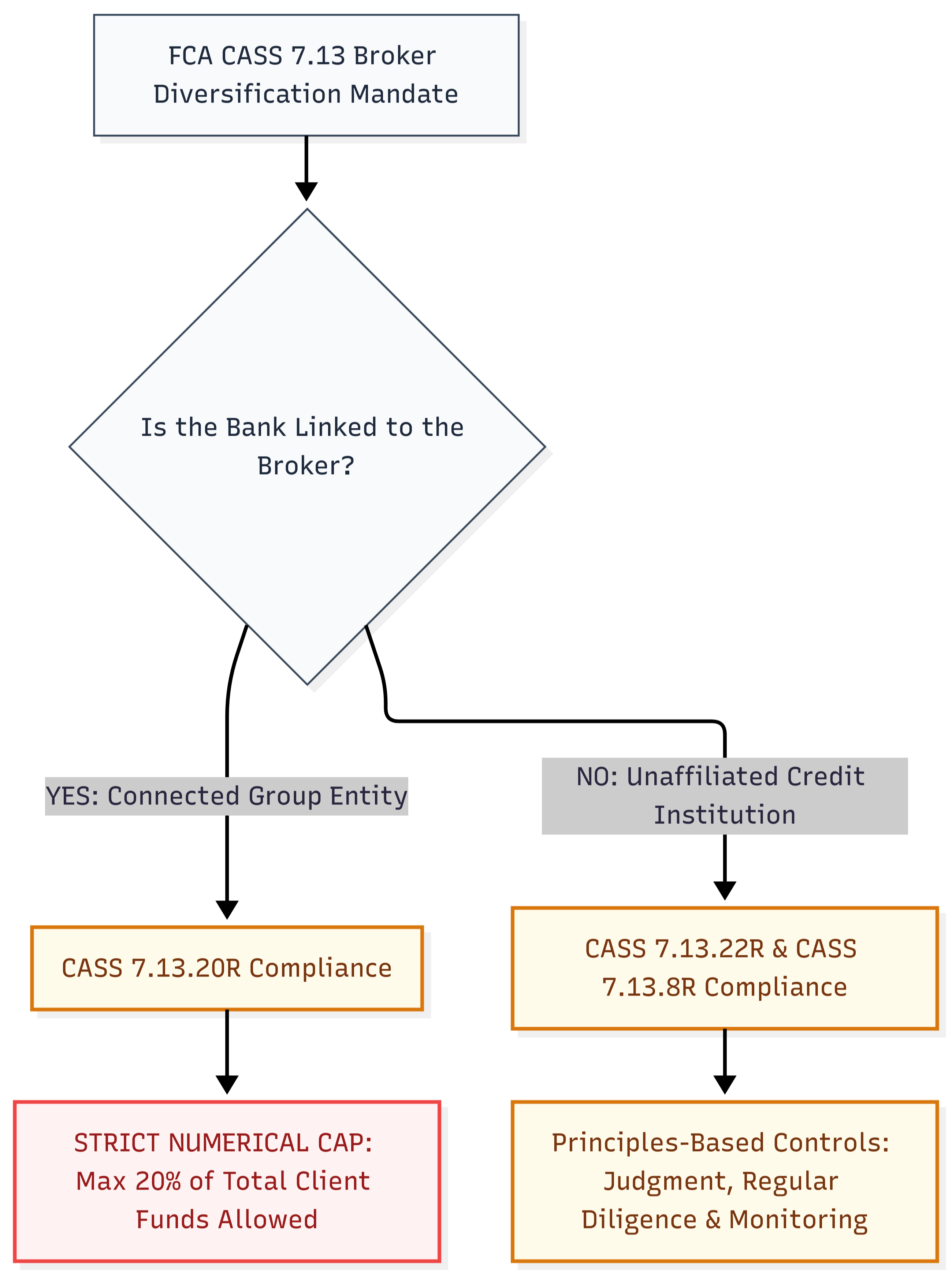

More specifically, it is CASS 7.13.22R that requires firms to periodically review their arrangements for holding client money, including whether it is appropriate to diversify placements across credit institutions. CASS 7.13.23G provides guidance on factors relevant to this assessment, including the potential use of multiple third parties and the need to consider exposure to entities within the same group when assessing concentration risk.

In addition, CASS 7.13.8R requires firms, when selecting and appointing credit institutions to hold client money, to exercise due skill, care and diligence and to have regard to the need for diversification of those institutions.

The rules also impose a specific concentration limit in relation to relevant group entities. Under CASS 7.13.20R, a firm must ensure that client money placed with a relevant group entity, or group of such entities, does not exceed 20% of total client money held. However, the CASS framework does not impose an equivalent numerical limit for exposures to unaffiliated credit institutions, instead relying on principles-based governance, due diligence, and ongoing risk management.

CASS 7.13.22 R

The key rule is CASS 7.13.22 R, which stipulates that a firm must periodically review whether it is appropriate to diversify (or further diversify) the third parties with which it deposits some or all of the client money that the firm holds; and whenever it concludes that it is appropriate to do so, it must make adjustments accordingly to the third parties it uses and to the amounts of client money deposited with them.

CASS 7.13.23 G

CASS 7.13.22R establishes that concentration risk is something that the firm must both review and take action against. Explanatory guidance for complying with the requirements in CASS 7.13.22 R is found in CASS 7.13.23G. Among other things, it says that the firm should have regard to whether it would be appropriate to deposit client money with a number of different third parties, and whether to limit exposure to entities within the same group.

In the FCA Handbook, the letter at the end of a provision shows its legal status. “R” stands for Rule, meaning it is a binding requirement that authorized firms must comply with, and failure to do so can lead to regulatory action by the FCA. “G” stands for Guidance, which is not legally binding but is intended to explain how the FCA interprets or expects firms to comply with the related rules in practice.

CASS 7.13.8 R

CASS 7.13.8 R is also relevant. Section (1) is broad and establishes that the firm must exercise due skill, care, and diligence when a bank, credit institution, or money market fund is selected for client money safekeeping. Section (2) is more specific because it stipulates that the firm must consider the need for diversification as part of its due diligence under (1).

CASS 7.13.20R

Furthermore, CASS imposes a specific concentration limit in respect of relevant group entities. Under CASS 7.13.20R, a firm must limit the amount of client money placed with a relevant group entity, or a combination of such entities, so that it does not exceed 20% of total client money held. However, the rules do not impose an equivalent numerical concentration limit for unaffiliated credit institutions, instead relying on broader requirements for due skill, care, and diligence, and ongoing risk management under the client money regime.

As you can see, CASS is creating a two-layered system. There is a hard rule in the form of a fixed 20% cap, but only for connected risk (group entities). For everything else, there are softer principles-based controls found throughout CASS 7.13, with requirements for judgment, diversification reviews, and ongoing monitoring. Group exposure means that there is a correlated collapse risk, which is why the hard limit has been put in place. The strict 20% cap is only for group-linked entities, and there is no such cap for unrelated entities. The 20% cap targets the risk caused by the concentration of client money within the same corporate group as the firm itself and limits how much client money that can be placed with the broker’s parent bank group or sister banks within the same financial group. If the entire group were subjected to a harsh event, there would be a risk of both broker failure and bank failure at the same time, and CASS is trying to prevent systemic contagion. CASS 7.13.20R and CASS 7.13.21R are thus not general banking diversification rules.