An Overview of the Chinese Yuan (Renminbi)

With the rise of China as a global economic power, many investors and economists consider the Chinese yuan as a potential successor to the US dollar as the world’s top reserve currency. The yuan officially became a “reserve currency” on October 1, 2016 upon its integration into the IMF’s Special Drawing Rights basket of currencies.

The Top Brokers For Renminbi Trading

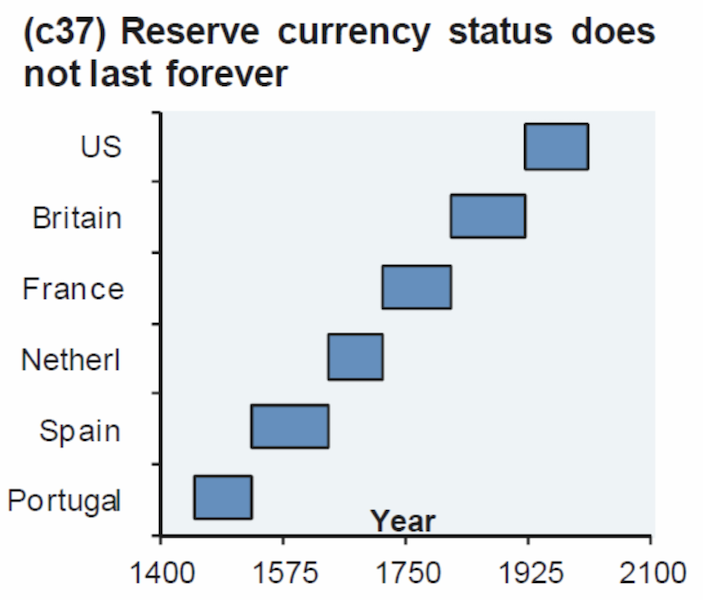

Status as the world’s top reserve currency has tended to be transitory. Going all the way back to the 1400s, six different countries or empires have held reserve currency status and each have lasted for around 100 years on average.

(Source: JPMorgan)

Typically, the country with the highest national income enjoys the status of having the world’s top reserve country.

A reserve currency is defined as a medium of exchange or store-hold of wealth that is held in significant quantities by central banks as part of their accumulation of foreign exchange reserves.

This currency can be used by other countries as an investment or as a medium to conduct international transactions. Because of its relative stability and value, it is normally considered a “safe haven” currency.

Other countries typically hold currency through the sovereign debt market of that country. (A bond is simply a promise to deliver a certain amount of currency in the future.)

The country with the world’s reserve currency derives an income advantage from it. This accounts for a sizable fraction of the gap between the top-earning country on an inflation-adjusted GDP per capita basis and the next highest earning countries.

Since the end of WWII, the real GDP per capita of the UK, Japan, and Germany have stabilized at around 70-80 percent of the US’s. Japan’s approximated 90 percent of the US’s just before its property bubble collapsed in 1989. The dollar’s influence has been a big part of this, and the USD has largely been considered the world’s reserve currency since the mid-20th century with the imposition of the Bretton Woods monetary system (disbanded in 1971 when the USD’s convertibility to gold was abandoned).

Because of the safety and liquidity of the US dollar and the US Treasuries market, this helps the US lower its borrowing costs (estimated at around $100 billion per year) and also allows it to borrow more than it otherwise could because there is more demand for its debt relative to countries determined to be less safe to invest in.

A semi-quick tangent on per capita GDP outliers

To be clear, the US does not have the highest per capita income in the world and per capita incomes are influenced by much more than reserve currency status. But the data is skewed by idiosyncratic outliers – e.g., oil and gas rich nations (Qatar, Norway, Kuwait, Brunei, UAE), tax havens (Ireland, Bermuda, Cayman Islands, Macau, Hong Kong, Singapore, Switzerland), and micro-states (Liechtenstein, Monaco, Luxembourg) – and aren’t appropriate to use when evaluating the wealth effect of relative reserve currency status.

Here we can view it in purchasing power parity terms, as compiled by the IMF, World Bank, and CIA:

(Source: Wikipedia)

(Source: Wikipedia)

Ireland, for example, cannot really use GDP or GDP per capita to measure its economy because of its tax haven status, which also affects euro area GDP aggregate measures. (The same is true for Malta, technically Europe’s second-fastest growing economy behind Ireland at the moment, though it is some way’s down the list in PPP terms).

US multinationals are the largest component of the Irish economy, who get a low-single-digit tax rate by consolidating part of their global operations in Ireland. Apple did it, for example, and Microsoft copied them (Singapore IP was sold to their Irish sub).

This tax distortion is so large that when measuring euro area domestic demand (the sum of consumption, government spending, and investment), it’s better to take Ireland and Netherlands IP investment out of the data entirely. Because the double Irish is being phased out in favor of CAIA, Ireland ends up owning a lot more IP, and gets multinational companies twice the tax shield.

However, not all of the GDP from these tax arbitrage strategies is “fake”. For example, some US pharmaceutical companies export their IP to a Caribbean tax shelter then do some type of production in Ireland, so there’s some real FDI in that. But most of the more than $3 trillion in FDI to low-tax jurisdictions is purely due to tax and/or regulatory arbitrage reasons.

A big part of the services deficit between the US and euro area is due to Ireland’s account. And the volatile nature of the dataset is a consequence of the swings in Ireland’s IP investment.

The emergence of the yuan

The yuan is China’s official currency. It is also known as the renminbi and commonly abbreviated as RMB, CNY (onshore traded yuan – i.e., traded in mainland China), and CNH (offshore traded yuan). CNY is the most typically used code for the currency. Based on Google search results, the term yuan to describe China’s currency is 15x more common than renminbi.

Given the general reality that the country with the highest national income is also the country with the world’s reserve currency, it’s believed by many that the CNY will eventually supplant the US dollar as the world’s reserve currency.

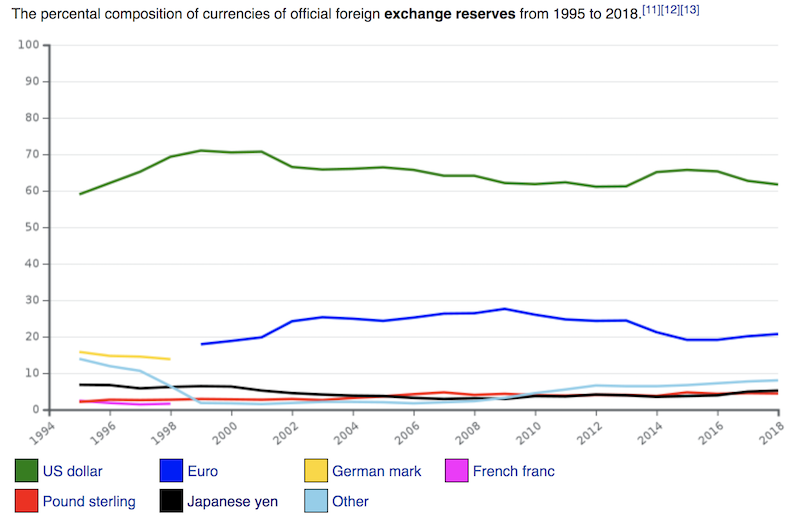

For now, it still has a long way to go to reach this goal. US dollars are 62 percent of global FX reserves, 62 percent of international debt, 57 percent of global import invoicing, 43 percent of FX turnover, and 39 percent of global payments.

(Source: Wikipedia)

The yuan is generally only 0-4 percent in each of these categories at the present moment. Until Chinese banks expand more overseas and if China become a large global hub for insurance, financial, and commodity markets – as well as the world’s most economically powerful country while improving its rule of law, protection of private property rights, oversight of its capital markets – integrating the CNY into the world’s reserves will be a slow process.

To further illustrate the dollar’s current entrenchment globally, according to a 2015 study, 62 percent of countries have a US dollar anchor in the exchange rate arrangements (compared to 28 percent for the euro). Sixty-four percent of all emerging market external debt is denominated in USD (compared to 13 percent for the euro).

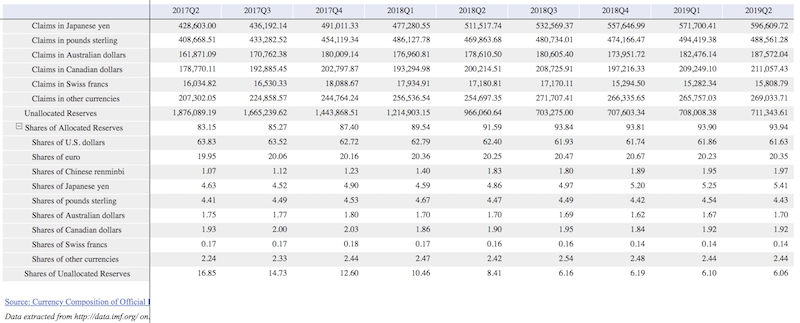

Based on the IMF data, as of Q2 2019, the CNY is 2 percent of foreign currency reserves globally.

It comes after USD (62 percent), EUR (20 percent), JPY (5.4 percent), and GBP (4.4 percent), and is comparable to reserves held in CAD and AUD at just under 2 percent.

The Swiss franc (CHF) is also a safe haven and a G-10 currency. But it yields negatively by a significant margin, making it off-limits to many central banks and sovereign wealth funds. Accordingly, in the global reserve data it barely registers.

How is the CNY exchange rate determined?

The CNY is heavily managed by the PBOC (China’s central bank) and through the country’s state banks. It’s officially called a daily “fix” or a target value by which policymakers choose to set it against a basket of other currencies (called the CFETS basket) and the USD.

The midpoint for CNY trading is announced each weekday at 9:15am Beijing time. The CNY will then trade within a 2 percent band of the midpoint, or a 1 percent allowance above or below the fix. If the CNY gets to the upper or lower bound of the bank, the PBOC will be on hand to buy (if it gets to the lower end) and sell (if it gets to the upper end) as needed.

In 2017, the PBOC introduced a new tool, called the “countercyclical factor” to weigh against strong moves in the currency in either direction. This is designed to weigh down on its volatility, which makes it more stable and attractive to hold by foreigners.

What makes the CNH different from CNY?

The CNH market was established by Chinese policymakers in 2010. CNH is simply yuan that trades offshore and is floated. The idea was for the CNH to help China expand its currency internationally so it could be used for invoicing and foreign transactions.

On many/most forex trading platforms, you can trade USD/CNH but will not be able to trade USD/CNY.

The CNH market is still heavily concentrated in Hong Kong (hence the ‘H’ at the end of it), but is also deliverable in other markets as well, such as London (CNL), Taiwan (CNT), and Singapore (CNS).

The disparity between CNY and CNH is typically taken as an indicator of capital outflows. When there is a higher level of outflows, the CNH will tend to trade at a weaker level than CNY. Nonetheless, the PBOC still manages the offshore yuan.

How can traders gauge the forward expectations of the Chinese yuan?

The CNY has non-deliverable forwards (NDFs) available in cases when restrictions prevent the buyer from taking delivery of the currency. So, parties involved in these transactions will resort to a NDF, which is settled in USD when the contract is due. The reference exchange rate for the NDF is not the prevailing spot market rate but rather the CNY fix.

How does the trade war with the US impact the USD/CNY exchange rate?

When any country is subject to tariffs, that’s a shock to its national income. If the currency is freely floated, it will see its currency decline relative to the currency of the country hitting it with tariffs.

With respect to China’s situation, one option it has is to offset US tariff threats by doing a managed depreciation against the USD.

How tariffs impact exchange rates mathematically

If the threat is another 15 percent in additional tariffs on up to $250 billion worth of goods, that’s $37.5 billion, multiplying the two together (0.15 * $250bn).

The US imports roughly $540 billion annually from China.

$37.5 billion divided by $540 billion is 6.9 percent.

Some part of the USD/CNY exchange rate already reflects forward tariff expectations. But if we ignore that, with the current exchange rate of 7.00, the new rate that’d be guaranteed to offset the effects would be 7.00*1.069 = 7.48.

The differential between the actual USD/CNY rate and the USD/CNY fix has regularly been the widest since before the 2015 devaluation. Here it was in late August:

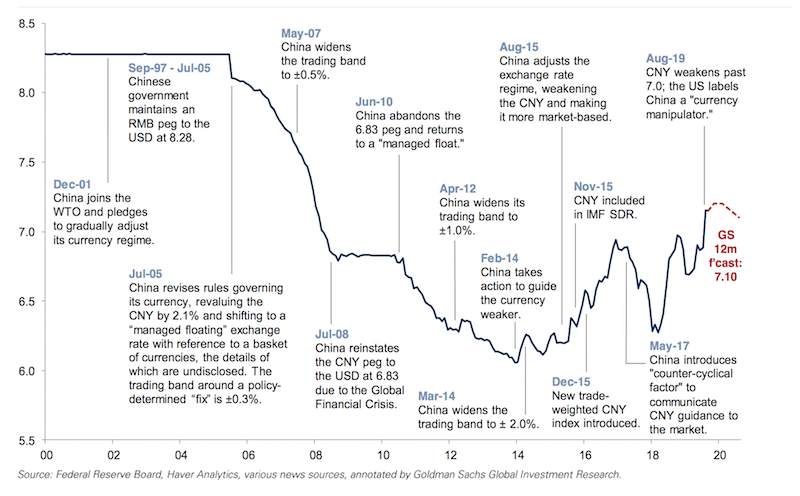

Below is a brief annotated history of the USD/CNY exchange rate since 2000.

Is China a currency manipulator?

The US Treasury labeled China a “currency manipulator” in August 2019, a day after China’s currency went above 7 to the US dollar (i.e., CNY depreciated against USD). It marked the first time the US had used the label on any country since 1994.

Does it have any practical consequences for China? In actuality, it doesn’t mean much. The move was more symbolic than anything.

With that said, the US’s trade policy – wanting smaller bilateral trade deficits – does fit the broader want for a weaker dollar. A weaker currency prices goods more cheaply in the international market. Therefore, it makes them more competitive, which helps reduce trade deficits and/or increase trade surpluses.

In the long-run, trade deficits and surpluses should theoretically close through movements in the currency.

In a shorter-run scenario, a country’s exchange rate is going to be in equilibrium when its balance of payments deficit or surplus is equal to its underlying capital flow. For example, if the US has to fund a balance of payments deficit of a certain amount, so long as enough capital is flowing abroad (debt, equity, deposits, loans) to meet that obligation, the currency will be considered in equilibrium.

‘Manipulation’ determinations are at the Treasury’s discretion

It’s under the US Treasury’s purview to review the foreign exchange practices of its trading partners and report these findings to members of Congress.

The two laws involved in determining currency manipulation were drafted in 1988 and 2015.

The 1988 law was invoked with respect to China, which gives the Treasury complete discretion in determining what country is manipulating its currency “for purposes of preventing effective balance of payments adjustments or gaining unfair competitive advantage in international trade.”

In terms of remediation of the dispute, the Treasury is instructed to take action to initiate negotiations bilaterally or through the IMF. The law isn’t clear what the next steps should be if they don’t bear any progress.

The 2015 law is more specific on exact determinations of what currency manipulation is. It is referred to as the Bennet criteria, which were put into place when the dollar was high and few countries were intervening in their FX markets to keep their currency artificially low.

The criteria are as follows:

- A bilateral trade surplus with the US that exceeds $20 billion.

- A “material” current account surplus that amounts to 3 percent of GDP or more.

- “Persistent,” one-sided intervention in which net purchases of foreign currency total at least 2 percent of a country’s GDP over a 12-month period.

China might meet the first criteria (bilateral trade surplus of a certain amount), but it does not meet the latter two.

In the mid-2000s, the last time there was talk to label China a currency manipulator, the Treasury department did not follow through, citing China’s commitments to improving its domestic growth.

Now, the US perspective toward China and its currency largely reflects US trade policy, with the “trade war” being one sub-plot in a broader geopolitical tangle involving an emerging power coming up to challenge an incumbent power economically, militarily, and technologically.

At the same time, the 1988 and 2015 laws may not be flexible enough to include other countries that might fit the bill as currency manipulators.

In October 2018, the Treasury’s monitoring list included China, India, Germany, Japan, Switzerland, and South Korea.

This year, newcomers to the “potential manipulators” watch-list include Vietnam, Malaysia, Singapore, Ireland, and Italy.

(Ireland and Italy share the euro, so the claim is not so much the euro itself is being broadly manipulated necessarily, but rather the purported contributions of these two countries.)

India and Switzerland were recently dropped from monitoring and no countries were labeled manipulators directly (i.e., they did not fit all three Bennet criteria).

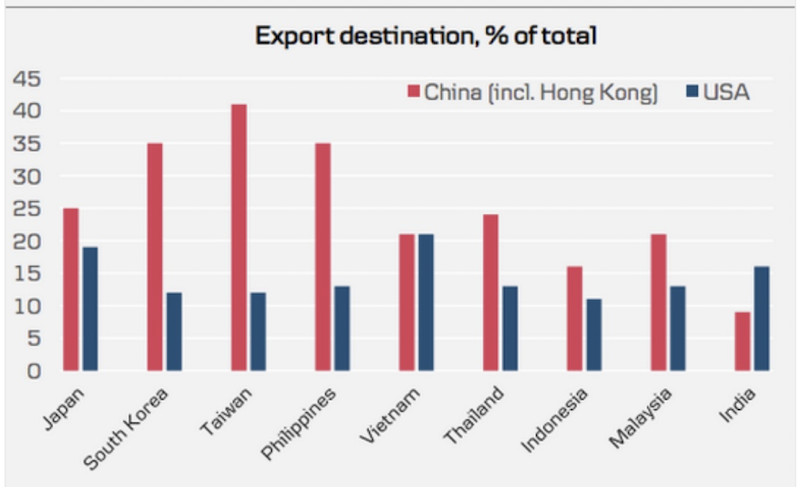

Vietnam is arguably the closest to being labeled a manipulator. For now, it escaped the label as the Trump administration’s trade action against China pushed down the currencies of most of China’s trade partners. These smaller export-oriented Asian economies generally rely more on China to buy their goods than the US. India depends more on the US than China for its exports and Vietnam’s dependence is roughly equitable between the two.

(Source: Macrobond Financial, Danske Bank)

This pushed all “managed float” Asian currencies down and reduced appreciation pressures on developing Asia’s most prominently managed currencies, which include Vietnam (VND), Thailand (THB), Singapore (SGD), and perhaps Taiwan (TWD).

Moreover, part of Vietnam’s trade surplus with the US is due to US policy directly. Tariffs on Chinese imports has incentivized supply chains to move toward Vietnam, particularly as an assembly point for electronics.

However, in practice, it will take a while for supply chain retrenchment away from China on any large scale. Supply chains aren’t anywhere near as developed in Vietnam (or Malaysia, Taiwan, Indonesia, and other competing markets) as they are in China. The machinery for capital-intensive work and safety standards aren’t as up to par. Vietnam has only about 7 percent of the population and there are current labor shortages.

With that said, the Treasury Department is likely to be more strict than it has been in the past. First, the Treasury will evaluate a higher number of its trading partners. Before, it had evaluated twelve countries, and has expanded this list to more than 20 based on more than $40 billion in goods exchanged per year.

Moreover, the threshold for a “material” current account surplus has been reduced from 3 percent to 2 percent. And any country engaging in “persistent, one-sided” FX intervention for six months (a lower amount of time) is enough for the Treasury to slap on the “manipulator” label.

In May 2019, the Trump administration announced it would place tariffs on countries that systematically undervalue their currencies. In other words, any country that uses currency subsidies that undermine or harm US industries are likely to see countermeasures by the Department of Commerce.

Can China sell US Treasuries to counteract the trade conflict?

China selling off US Treasuries can only happen on a limited scale. There is no other sovereign debt market that provides this sort of scale that reserve managers can target for safety, liquidity, and yield. Japanese government bonds and German bunds are much less abundant and don’t provide anywhere near the same yield.

The Fed has the tools to react to a “capital war” anyway, such as signaling a rate cut and/or absorbing the excess supply not wanted by the private markets by buying it directly.

What the US should be worried about is China orchestrating a depreciation.

The yuan’s valuation over the long-run

Over the long-run, I am bullish on the CNY and Chinese assets. China’s per capita incomes are only about 15 percent of those in the US. Prices between the US and China eventually will need to get closer in line.

This won’t happen by US incomes being cut down closer to current Chinese incomes and Chinese incomes won’t come fully in line with US incomes. But they will eventually need to come closer. The yuan and yuan-denominated assets are too cheap in US dollar terms. So, eventually a devaluation of the dollar relative to the yuan is likely.

Due to trade frictions, the USD recently made an 11-year high against the CNY. If the US escalates the trade conflict against China, it could get even worse. In such a scenario, the USD/CNY in the 7.50-8.00 range isn’t out of the question if it were to get to that point (basically the US placing tariffs on everything and at reasonably high rates.)

But it doesn’t make a ton sense for the USD to remain that high against the CNY over the long-run. The Chinese economy is simply a lot bigger and more productive than it was eleven years ago.

Even if you (wisely) don’t take the Chinese government’s GDP and other economic data at face value, it is still growing faster than the US economy. It still has more catch-up to do technologically and building out an urbanized middle class of consumers, which will work to close the per capita income gap.

Only 3.0-3.5 percent output growth is sustainable for China based on current productivity and labor growth trends compared to 1.5-2.0 percent for the US. (GDP is a mechanical function of the sum of the growth in productivity and the growth in the labor market.)

So, a dollar devaluation against the yuan not only seems likely but would also be healthy for the US – i.e., it would help to close trade deficits, reduce US external debt as a percentage of GDP – and also for the rest of the world.

What all this means for traders

The US wants – and needs – a weaker dollar. However, all developed countries are not keen on having a stronger currency either. Japan and Switzerland have come out and denounced having a stronger currency. Europe is stuck at zero and negative interest rates on cash and many longer-term bonds and other financial assets; it is stuck with perpetual QE, and still has little growth or inflation. So, they don’t want a stronger currency either.

G-10 FX as a whole has become an asset class that isn’t the most interesting to trade.

It’s not just the low / zero / negative rates that make the returns low (i.e., for carry trade purposes). But rather, since no country cares much for a higher exchange rate, they are broadly working to match each other’s policy moves to prevent relative currency swings.

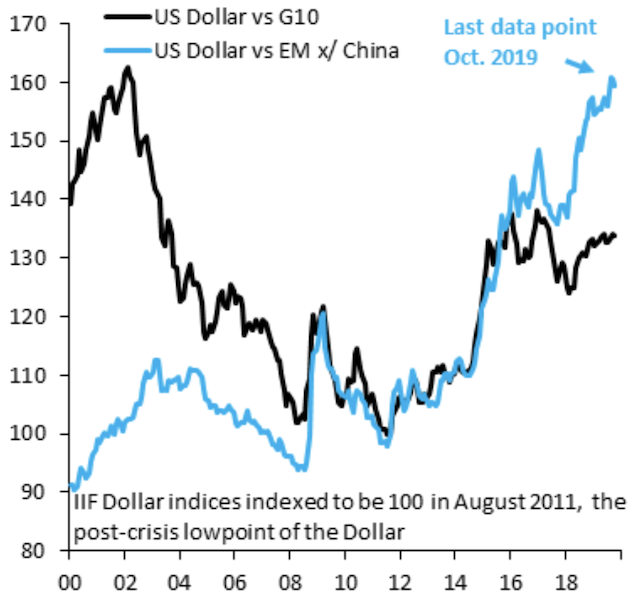

The dollar’s action versus other G-10 FX hasn’t done much over the past four years (black line), though the USD has increased in value in relation to emerging markets (blue line).

Policymakers’ desire to keep a lid on their currencies also tends to benefit alternative store-holds of wealth like gold, whose value is proportional to the amount of reserves and currency in circulation globally relative to the size of the gold stock (which only expands by 1-3 percent per year).