All In The Charts For US Bonds

A bit of a chart fest today, but I hope it best portrays the issue at hand. That being, the world has had a strong re-think on the prospect of a US and global recession and while this is not a new trade, it has now reached a point where market participants are talking about it in earnest.

Given the interest, therefore, perhaps we can consider fading the move, but, as always let price guide.

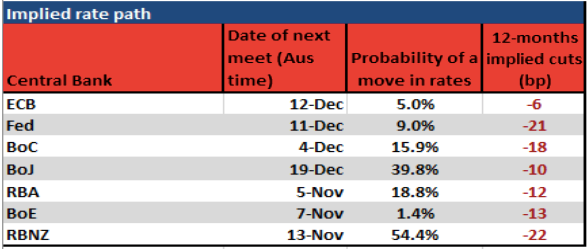

Interest Rate Expectations

Here we see the probability of a cut at the next meeting, as well as what is priced over the coming 12 months.

Honing into US rates markets, we currently see 42bp of cuts (from the Fed) priced by December 2020. This was 133bp of cuts not so long ago. The white line represents zero.

Economic data has its vulnerabilities, and we are not out of the woods, and anyone who saw the recent downgrade to the Atlanta Fed’s Q4 GDP nowcast model to just 1% would attest to the fact that growth is not brilliant.

That said, it’s not terrible, and traders have reduced a number of their recession and trade tension hedges.

If we don’t see a trade agreement signed in mid- to late-November, and the devil is in the detail, and we have not seen an unwind tariffs, then risk aversion will kick in and implied vols will ramp up again.

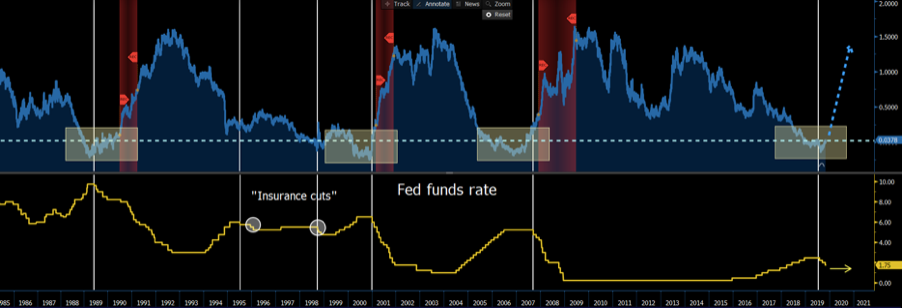

The Bond Market Is Where It’s At:

US Treasury 2s vs 5s curve – One of my favourite charts, as it tackles the debate on whether the Fed has further to go on rate cuts, or whether this is truly the end of the mid-cycle adjustment and insurance cuts.

As we see in the last few decades when the 2s vs 5s curve inverts (that is 5yr yields are lower than 2yr yields) we have seen a strong steepening which has preceded a recession and a strong cutting cycle.

Certainly not an ‘insurance cut’ which is what we saw in 1995/98. The bears will focus on this chart, but is this time different?

UST 10-year real yield (white) – It worries me that ‘real’ (i.e. inflation-adjusted) yields are moving higher. I have overlapped this against gold (which I have inverted), but if real Treasury yields move any higher, and it’s the rate of change that is a key consideration too, then global equities will also face headwinds.

US 3-month vs 10-year Treasury curve – Here I have overlapped the 3m10yr curve (orange) vs high-grade copper (candle chart), which as we know has a PhD in global economics. The curve has moved from -55bp (on 29 August) to +28bp…that is a huge move by any standards.

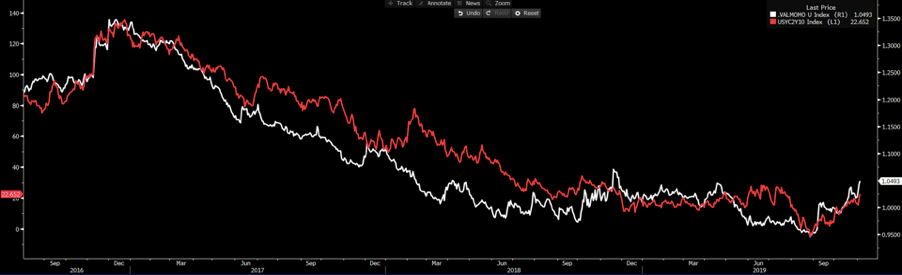

US Treasury 2s vs 10s curve vs the S&P500 value/momentum factor ratio (white) – I have used the IVE and MTUM ETF as input for my ratio, where we see value stocks outperforming momentum in a big way and following the steeper curve.

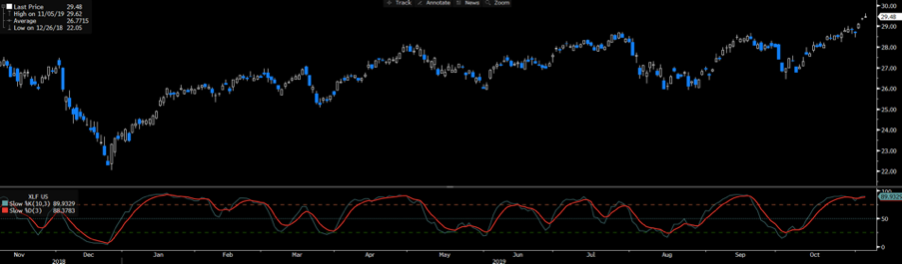

XLF ETF

XLF ETF (US financial sector ETF) – Banks love a steeper curve, as they borrow at the short-end and lend at the long-end, so a steeper curve, therefore, boosts their net interest margins. US banks are flying, although the move is clearly mature. Pepperstone will be offering the XLF, IVE and MTUM ETF’s soon to clients.

S&P 500 futures vs US Treasury futures ratio….The break here shows equities are clearly outperforming fixed income and the pattern suggests the probability is it continues

Basic Fed Policy Model

US5Y5Y forward rate – US 3-Month Treasury (yellow) vs Fed funds rate (blue) – My basic Fed policy model.

Without explaining the mechanics of the US5Y5Y forward rate, at a simplistic level it is considered the market’s interpretation of the LT neutral rate – that being, the correct policy setting considering views on future inflation, growth and employment.

When this is heading lower it suggests ST rates, which align with the fed funds rate, are moving higher than the perceived neutral rate – thus, the market feels Fed policy is too tight.

This model recently got down to -55bp, highlighting that the market felt Fed policy needed at least two cuts just to get a neutral setting. This has since re-priced and sits at +15bp. In layman’s terms, the market now feels, given all we know, that the Fed’s policy-setting is neutral – neither stimulatory or restrictive.

How do we play a steeper curve in FX? USDJPY – we’ve seen two clear fake outs in this run into 109…however, through this session it closed through here…